Rental Property ROI in Canada 2026: How New Construction Returns Compare to Every Alternative

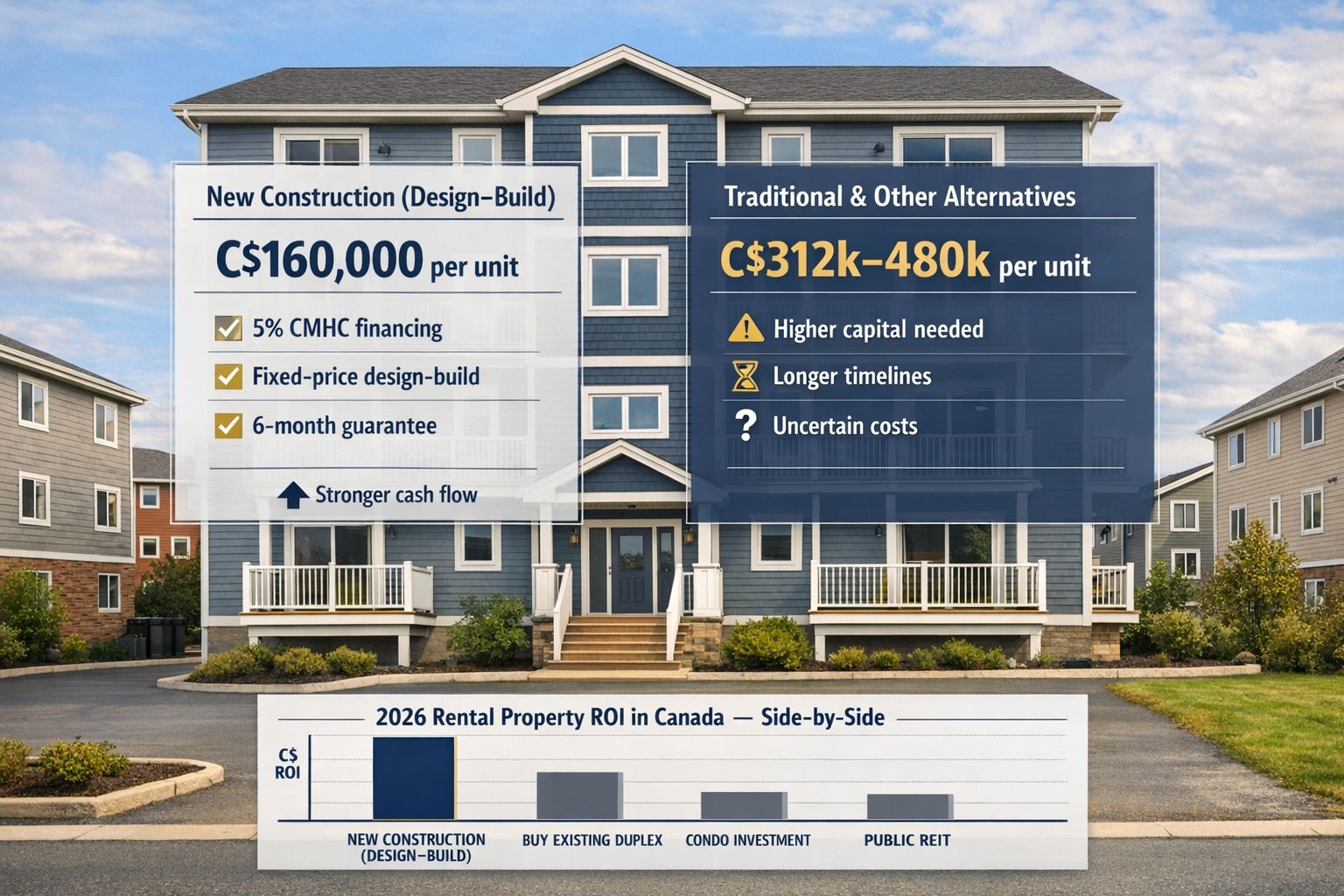

If you're investing in Nova Scotia's rental market in 2026, you're likely asking: What delivers the highest return on investment - buying existing properties, building new units, or going with alternatives like REITs or short-term rentals? Here's the quick answer: constructing new multi-unit rentals costs approximately $160,000 per unit, compared to $250,000–$480,000 per unit for existing buildings. That’s an immediate $90,000 per unit in equity, or $540,000 for a sixplex. Add CMHC MLI Select financing, which allows 5% down payments and 50-year amortizations, and new construction becomes an attractive option for cash flow and scalability.

This article breaks down how new builds stack up against buying single-family homes, existing multi-units, REITs, and short-term rentals. Whether you're navigating Halifax's 5.50%–6.25% cap rates or weighing the risks of regulatory hurdles, this guide will help you decide which strategy fits your goals.

ROI vs Cash-on-Cash: The Real Return Most Beginners Miss | Investor Ian In Canada

sbb-itb-16b8a48

1. Buying Existing Single-Family Homes

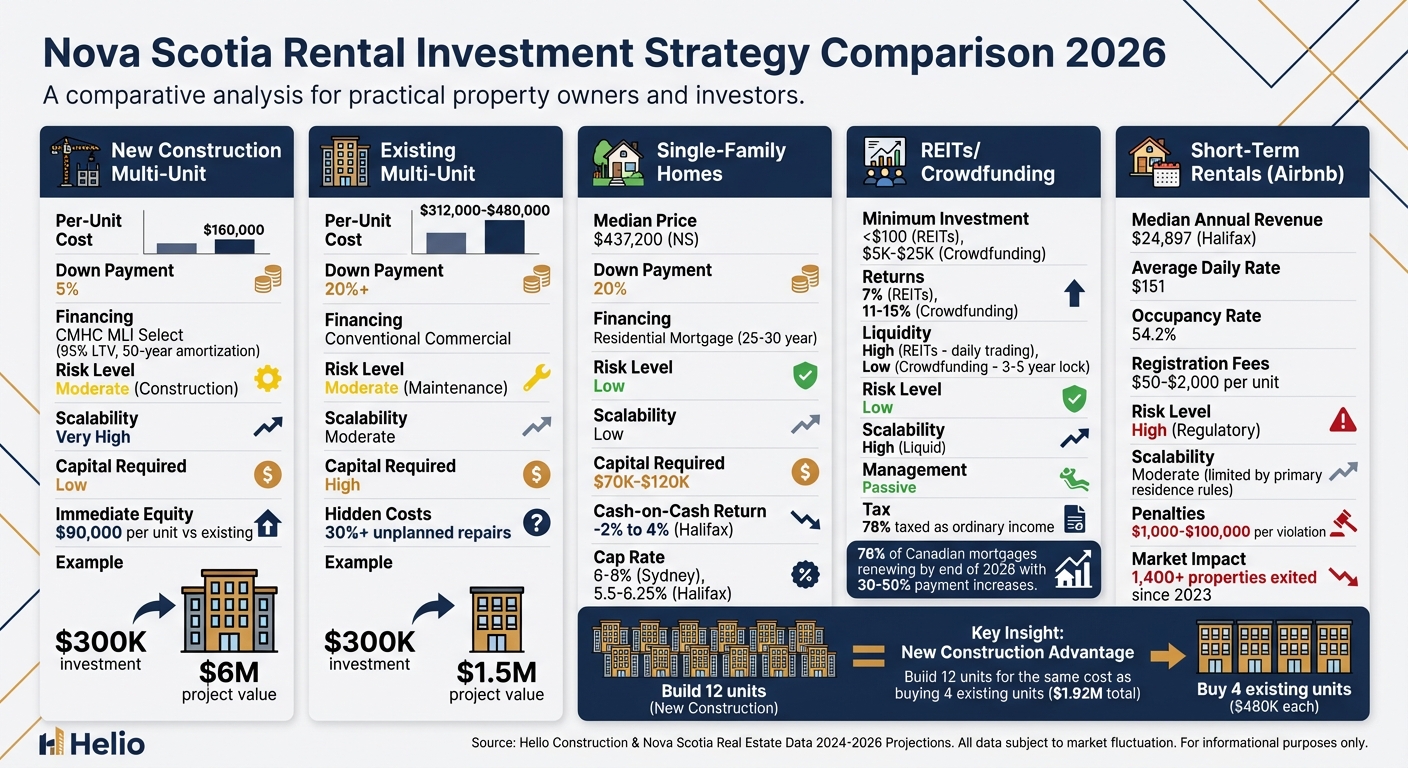

For many Canadian investors, single-family homes are often the first step into rental property investment. However, 2026 data paints a less-than-rosy picture, especially in Nova Scotia. In Halifax, cash-on-cash returns currently range from -2% to 4%, meaning investors are either barely breaking even or facing outright losses after covering expenses [3]. With the province's median home price at $437,200, entering the market typically requires $70,000 to $120,000 in liquid capital [3].

The financial hurdles don’t stop there. Investors face a 10% non-resident deed transfer tax and a 2% annual property tax, which further erode potential profits [3]. Take a $500,000 property in Halifax, for example. While $2,200 in monthly rent might seem promising, heating costs alone - especially in older homes without heat pumps - can eat up 10-20% of operating expenses [3].

Michael Crawford of the Atlantic Canada Investment Group explains: "The most successful Nova Scotia investors recognize that the province's real estate market has fundamentally changed since 2020. The influx of remote workers, technology professionals, and lifestyle migrants has created new demand patterns that aren't fully reflected in historical data" [3].

For those focused on long-term appreciation, single-family homes can still make sense, particularly in areas like Sydney. There, average home prices of $275,000 offer 6-8% cap rates, a far cry from Halifax’s slim margins [3]. However, maintenance risks - think roof replacements, HVAC failures, or foundation repairs - can quickly wipe out gains. Financing also presents challenges, as conventional mortgages (20% down, 25-30 year amortization) tie up significant capital.

This is where new multi-unit builds shine. They qualify for CMHC MLI Select financing, allowing 5% down and 50-year amortizations, compared to the 20% down required for existing homes. With per-unit costs averaging $250,000 for existing rentals versus $160,000 for new builds, the $90,000 cost difference makes a strong case for construction [2].

For investors banking on interprovincial migration and willing to accept slim cash flow in exchange for 7-10% annual appreciation, single-family homes in central Halifax remain an option [3]. However, those seeking better cash flow or scalability will need deeper pockets - or may need to look beyond Halifax to higher-yield markets.

2. Purchasing Existing Multi-Unit Properties

Investing in multi-unit properties - like duplexes, triplexes, or small apartment buildings - can provide a steady stream of income and lower risk compared to single-family homes. These properties spread rental income across multiple units, which helps cushion losses from vacancies. In Canada, cash-on-cash (CoC) returns for multi-unit properties typically range from 8–12%, but urban markets often see lower yields between 5–7% [5].

In Nova Scotia, buying an existing multi-unit property in 2026 could cost anywhere from $312,000 to $480,000 per unit [2]. However, older "B" and "C" class buildings often come with hidden costs. Common issues like roof repairs, electrical updates, or HVAC replacements can eat up over 30% of your budget on unplanned repairs [2]. While these properties generally have lower tenant turnover, their age makes them less appealing to renters who increasingly prefer newer buildings with modern amenities. This can lead to higher vacancy rates and greater maintenance costs, which widen the expense gap compared to newly built properties.

Jeff Caddell, Director at Property Valuation Services Corporation, highlights: "We're seeing more of a focused demand for homes, those smaller-type homes, semi-detached townhouses, duplexes, multi-unit. Relatively speaking, more affordable homes, more moderately priced, is where we're seeing the highest demand and the market growth" [4].

The financial contrast between buying older units and building new ones is stark. For example, a fourplex priced at $480,000 per unit totals $1.92 million. By comparison, constructing new units at $160,000 each would allow you to build 12 units for the same amount. That’s an additional eight units, which significantly boosts cash flow and long-term equity.

The Canada Mortgage and Housing Corporation (CMHC) offers its MLI Select financing program to support existing properties. It provides up to 95% loan-to-value (LTV) financing with 50-year amortizations and lower insurance premiums (2.60% compared to 3.25% for new construction) [8][9]. However, these loans come with strict conditions: you’ll need at least five years of experience managing multi-unit properties and a net worth equal to 25% of the loan amount, with a minimum of $100,000 [7]. For first-time investors, these requirements often make building new properties a more accessible and cost-effective option.

3. Investing in REITs or Crowdfunding Platforms

REITs and crowdfunding platforms offer ways to invest in real estate without the hassle of managing properties. Canadian REITs, for example, posted an 11.8% total return in 2025, with an average sector yield of around 7% as of early 2026 [15]. Public REITs are highly liquid, with shares often priced under $100 and traded daily, making it easy to buy or sell [10][12].

Crowdfunding platforms, on the other hand, usually require a higher upfront commitment. Minimum investments often start at $5,000, though some platforms allow entry for as little as $1, while others catering to institutional-grade investments may demand $25,000 or more [12][14]. Expected returns fall between 11% and 15% [12], but there’s a catch: your capital is tied up for 3–5 years, limiting liquidity. The 2023 PeerStreet bankruptcy also underscores the risks tied to these platforms [14].

| Feature | Public REITs | Crowdfunding | NS New Construction |

|---|---|---|---|

| Liquidity | High (daily trading) [10] | Low (3–5-year lock-in) [12] | Low (sales can take months) [13] |

| Min. Investment | < $100 [12] | $5,000–$25,000 [12][14] | High (typically 5–20% down payment) |

| Management | Passive [10][12] | Passive [12] | Active (owner-managed or via a manager) [13] |

What this means for property owners: REITs provide monthly distributions and liquidity but at the cost of control and certain tax benefits. For instance, in 2024, 78% of REIT dividends were taxed as ordinary income rather than as capital gains [13]. By investing in REITs, you also miss out on leveraging CMHC-backed financing (up to 95% LTV) that can significantly boost returns on new construction projects.

Ultimately, the choice comes down to control and leverage. REITs make you a passive shareholder in a professionally managed portfolio, while building new construction allows you to own a tangible asset, build equity, and take advantage of government-backed financing. Next, we’ll dive into how new construction uses financing to amplify returns.

4. Short-Term Rentals (Airbnb) in Nova Scotia Markets

Short-term rentals in Halifax can deliver solid gross revenues. In 2026, the median property brought in $24,897 annually, with an average daily rate of $151 and an occupancy rate of 54.2% [16]. Some properties, like the Seacliff luxury waterfront rental, performed exceptionally well, earning $179,853 over 12 months with a nightly rate of $740.48 and a 55.4% occupancy rate [16]. However, these numbers come with significant regulatory and operational hurdles.

Since mandatory registration began in April 2023, fees have ranged from $50 for primary residences to $2,000 per commercial unit in Halifax, alongside a 3% marketing levy [20][22][23]. Non-compliance carries steep penalties, with fines ranging from $1,000 to $100,000 per violation [18][23]. These changes have already had a tangible impact - over 1,400 properties have left Nova Scotia's short-term rental market since the registration rules took effect [19].

One of the biggest challenges is the primary residence restriction, which limits short-term rentals to an owner's principal dwelling in many municipalities, including Halifax [20][21]. This rule aims to protect long-term housing availability but effectively caps investors at one property, making it difficult to scale operations. Even compliant hosts face a shifting market: 31.7% of Halifax listings have moved to a minimum stay of 30 nights to reduce regulatory exposure [16][17]. These constraints make it clear why some investors are rethinking their strategy.

While short-term rentals can generate strong cash flow, their scalability is hampered by high registration costs, strict municipal rules, and the risk of enforcement penalties. For investors looking to grow their portfolios and achieve more predictable returns, new multi-unit construction - especially when paired with CMHC-backed financing - offers a more practical and scalable alternative.

Next, we’ll dive into how new construction multi-unit projects stack up against short-term rentals, focusing on per-unit costs, financing options, and long-term profitability.

5. New Construction Multi-Unit Builds in Nova Scotia

New construction for multi-unit rentals in Nova Scotia stands out as a cost-effective alternative, reducing per-unit costs significantly. At roughly C$160,000 per unit, this approach is 36%–67% cheaper than acquiring existing buildings, which range from C$312,000 to C$480,000 per unit. This cost reduction is largely due to integrated design-build models, which eliminate the need to juggle six or seven separate contractors, a common feature of traditional construction. Adding to the financial appeal, the provincial HST rebate for purpose-built rentals - available for projects started after September 14, 2023, and completed by December 31, 2035 - further enhances affordability. The 2026–27 Nova Scotia budget has earmarked C$54.1 million for this rebate [11].

Why this matters to property owners: New construction not only lowers upfront costs but also reduces the risk of long-term maintenance headaches.

The financing landscape also favours new builds. CMHC MLI Select financing offers attractive terms, including up to 95% loan-to-value ratios (5% down payment), 50-year amortization periods, and debt service coverage ratios as low as 1.1x [26][27][28]. Projects scoring 70–100 on CMHC's scale can also qualify for 20%–30% discounts on insurance premiums [28].

Rob Lough, Broker/Owner at Century 21 Optimum Realty, explains: "The provincial HST rebate continues for new purpose-built rental projects... this significantly improves the financial viability of new multi-unit rental development" [11].

New construction offers advantages that existing property purchases or REITs cannot match. It provides full control over the asset, immediate equity creation, and avoids inheriting issues like deferred maintenance, outdated systems, or tenant conflicts. Additionally, new builds come with warranty coverage and compliance with modern building codes.

Integrated design-build projects also deliver speed, with units typically generating revenue within six months from permit approval to move-in. Halifax cap rates of 5.50%–6.25% and average two-bedroom rents of C$2,058 per month further enhance cash-on-cash returns [1][24]. Unlike REITs, which offer passive yields around 2.73% [1], new construction demands active involvement but compensates with higher returns and appreciation potential.

While construction risks like delays and cost overruns exist, integrated design-build models mitigate these through fixed-price contracts and guaranteed completion dates. The shift from condominium developments to purpose-built rentals highlights developer confidence in this model, supported by favourable government financing and the lack of presale requirements [25]. These factors position new construction as a strategic option for property owners seeking higher returns and long-term asset control.

Pros and Cons of Each Strategy

Nova Scotia Rental Investment Strategy Comparison 2026: ROI and Capital Requirements

Every rental investment strategy comes with its own set of trade-offs, particularly in terms of upfront capital, risk levels, and growth opportunities. The table below provides a snapshot of how five common strategies stack up under 2026 market conditions in Canada, with a focus on financing accessibility and potential for scaling.

| Strategy | Risk Level | Capital Requirement | Scalability | Financing Options |

|---|---|---|---|---|

| New Construction Multi-Unit | Moderate (Construction) | Low (5% down) | Very High | CMHC MLI Select (95% LTV) |

| Existing Multi-Unit | Moderate (Maintenance) | High (20%+ down) | Moderate | Conventional Commercial |

| Single-Family Homes | Low | Moderate | Low | Residential Mortgage |

| REITs / Crowdfunding | Low | Very Low | High (Liquid) | N/A (Cash Investment) |

| Short-Term Rentals | High (Regulatory) | Moderate | Moderate | Residential/Commercial |

This breakdown highlights the compromises investors face. Below, we'll unpack what these differences mean in practice.

One standout feature of the New Construction Multi-Unit strategy is its leverage potential. With CMHC MLI Select, a mere 5% down payment can secure assets worth 20 times the initial investment. This allows investors to refinance and grow their portfolios quickly - turning a single fourplex into multiple properties by tapping into immediate equity gains [2].

On the other hand, REITs and Crowdfunding offer high liquidity but come at the cost of control. These investments are also more vulnerable to market fluctuations. Existing Multi-Unit properties require significant upfront capital - typically 20% or more - and stricter lending conditions under OSFI rules. Many of these properties fall under the Income-Producing Residential Real Estate (IPRRE) category, which often comes with higher interest rates [30][6]. Meanwhile, Short-Term Rentals face increasing regulatory challenges as municipalities impose tighter restrictions on their operation [6].

The 2026 market conditions also put additional pressure on investors. With approximately 76% of Canadian mortgages set to renew by the end of 2026, many borrowers will encounter payment increases of 30%–50% due to rising interest rates [29]. In this environment, the longer amortizations - up to 50 years - offered through CMHC MLI Select become a critical tool for maintaining positive cash flow.

Allwyn Dsouza, Senior Analyst at REIC, explains: "CMHC's Apartment Construction Loan Program and its MLI Select insurance made financing cheaper and de-risked, pulling thousands of rental projects off the drawing board" [29].

These distinctions in financing and scalability highlight why new construction stands out as the most effective strategy for investors navigating the 2026 landscape.

Conclusion

When it comes to investment strategies, new construction multi-unit builds in Nova Scotia stand out as a practical choice for 2026, offering a solid mix of return on investment, scalability, and financing flexibility. Building new units costs about $160,000 per unit using integrated design-build models, which is 36–67% lower than the $312,000–$480,000 per unit required to buy existing properties [2]. The CMHC MLI Select program further amplifies this advantage, requiring only a 5% down payment for new construction projects compared to the 20%+ typically needed for existing multi-unit purchases.

The financial benefits extend beyond lower upfront costs. CMHC's multi-unit insurance products have shown strong performance, with 197,573 units insured in the first three quarters of 2025 and an arrears rate of just 0.32% as of September 2025 [31]. In response to this stability, the Canada Mortgage Bonds annual limit increased from $60 billion to $80 billion, further supporting multi-unit financing [31]. Additionally, projects that meet energy efficiency and affordability benchmarks can receive premium discounts of 10%, 20%, or 30%, reducing the overall cost of capital [8][9].

Consider this: with $300,000 to invest, you could either buy an existing multi-unit property worth about $1,500,000 (requiring a 20% down payment) or build a new project valued at up to $6,000,000 (requiring only a 5% down payment) [2]. This difference in leverage creates a significant opportunity for portfolio growth. For example, refinancing under CMHC MLI Select could turn a modest fourplex into a portfolio of up to 24 units, enabling rapid expansion.

Market conditions in 2026 further support this approach. In Halifax, 81% of all housing starts are targeted at the rental market [32], and a projected shortage of 15,000 construction workers by 2034 [33] will likely constrain future supply. Starting a project now positions property owners to benefit from rising demand and increasing construction costs down the line.

In a landscape marked by rising capital requirements and shifting regulations, new construction provides a clear path to achieving positive cash flow and long-term equity growth. With lower per-unit costs, better financing terms, and the potential for scalability, it remains one of the most effective strategies for building wealth through rental properties in 2026.

FAQs

How do I qualify for CMHC MLI Select financing?

To qualify for CMHC MLI Select financing, you’ll need to meet a few key requirements. First, your project must align with affordability benchmarks, typically tied to the median renter income in your area. Second, you should have at least five years of experience managing rental properties, which shows you understand the operational side of the business. Lastly, you’ll need to demonstrate that you have expertise in handling multi-unit projects - this could mean anything from previous developments to managing similar properties. Make sure your application clearly addresses these points to strengthen your case for approval.

What are the biggest risks when building a new multi-unit rental?

Delays, unexpected costs, and dealing with regulatory requirements are some of the most significant risks in development projects. Smaller projects, in particular, can be deceptively complicated - what looks straightforward on paper often turns out to involve more layers of complexity. To tackle these challenges effectively, thorough planning and a solid grasp of local regulations are absolutely crucial.

How do interest rates affect cash flow and ROI in 2026?

In 2026, interest rates are expected to hold steady, which bodes well for rental property investments. With borrowing costs staying predictable, financing expenses are less likely to fluctuate. This stability helps property owners maintain consistent cash flow and dependable returns on their investments.