Real Estate for Retirement: How Building Rental Property Creates Pension-Like Income in Canada

If you’re nearing retirement and worried about income falling short, you’re not alone. In Canada, CPP and OAS combined rarely exceed $2,000 per month, leaving a gap when you need $3,000–$4,000 to retire comfortably. Fewer Canadians have employer pensions, and RRSPs come with risks like market fluctuations and tax complications. For many, rental properties are filling that gap. In Nova Scotia, a fourplex costs about $640,000 to build and can generate $7,600–$9,000 in monthly rent. After expenses, this translates to $4,000–$5,000 in net income - steady cash flow that doesn’t run out, unlike savings. This article breaks down how rental property works as a retirement strategy, focusing on costs, financing, and returns in Nova Scotia.

How Does Rental Real Estate Impact Your Retirement Strategy?

sbb-itb-16b8a48

How Rental Properties Compare to Standard Retirement Strategies

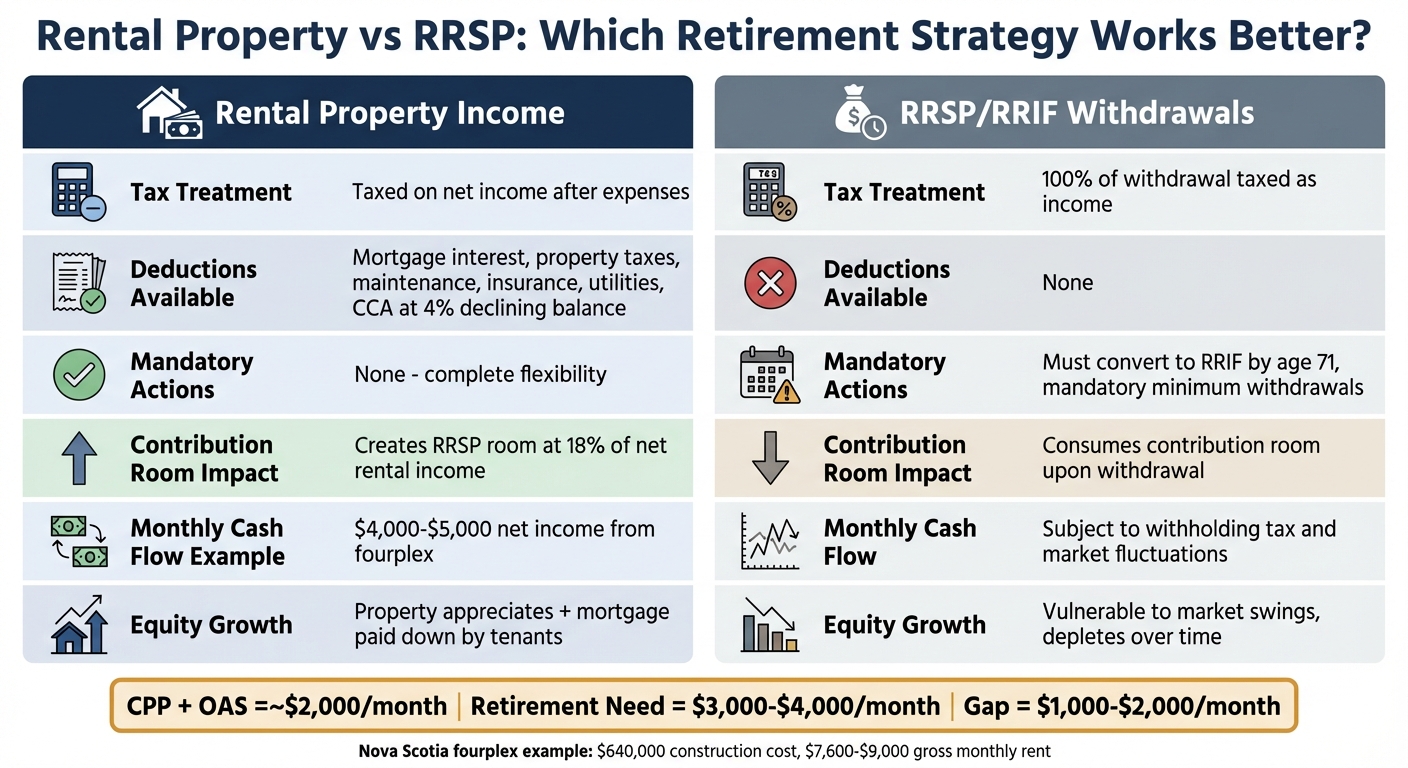

Rental Property vs RRSP Retirement Income Comparison

Rental properties and traditional retirement savings, like RRSPs and pensions, function very differently. RRSPs and pensions provide predictable income but come with rigid rules that can limit financial flexibility. On the other hand, rental properties not only generate consistent income but also build equity over time. This dual benefit addresses many of the shortcomings associated with conventional retirement planning, offering a more adaptable and potentially rewarding approach.

Monthly Cash Flow vs. RRSP Withdrawal Limits

RRSPs come with strict withdrawal rules, especially after age 71. At that point, RRSPs must be converted into a RRIF or an annuity, and withdrawals are taxed at your marginal rate. On top of that, withholding taxes apply to withdrawals, creating additional hurdles. Every dollar you take out is fully taxable.

Rental properties, however, don’t have these restrictions. A well-managed fourplex, for example, generates steady monthly cash flow, much like a pension cheque, but without mandatory withdrawal schedules or conversion deadlines. Plus, you’re only taxed on the net income - after deducting expenses like mortgage interest, property taxes, insurance, and maintenance costs [3]. This flexibility makes rental income a more manageable and tax-efficient option for retirement.

Growing Equity vs. Fixed Pension Payments

Most pensions offer fixed payments, with only modest adjustments for inflation, if any. RRSPs, while more flexible, are vulnerable to market swings that can erode their value. Rental properties, particularly multi-unit buildings in sought-after locations, provide a hedge against these risks. They not only appreciate in value over time but also build equity as tenants pay down the mortgage.

Multi-family buildings also distribute income across multiple tenants, reducing the financial impact of a vacancy compared to single-family homes [9]. Unlike pensions, rental properties allow you to adjust rents in response to market conditions, creating the opportunity to grow your income over time. This ability to adapt can help close retirement income gaps and build wealth, ensuring a more stable financial future.

Tax Benefits of Rental Income in Canada

In addition to providing consistent cash flow and equity growth, rental properties offer tax advantages that RRSPs and pensions simply don’t. Rental property owners can deduct a wide range of operating expenses - mortgage interest, property taxes, maintenance, insurance, utilities, and professional fees - all of which reduce your taxable rental income [3]. You can also claim Capital Cost Allowance (CCA) at a 4% declining balance rate, which could even bring your taxable rental income down to zero [6].

Another advantage is that the CRA treats net rental income as "earned income", which increases your RRSP contribution room by 18% of your net rental income [6][7][8]. With the 2026 maximum RRSP contribution limit set at $33,810 [5], rental properties not only provide retirement income but also expand your ability to defer taxes on other earnings.

Jason Heath, Certified Financial Planner at Objective Financial Partners, notes: "Retirees are often better off taking RRSP withdrawals as opposed to contributing to RRSPs, to minimize their lifetime tax payable" [6].

| Feature | Rental Property Income | RRSP/RRIF Withdrawals |

|---|---|---|

| Tax Treatment | Taxed on net income after expenses | 100% of the withdrawal is taxed as income [4] |

| Deductions | Interest, property taxes, maintenance, CCA [3] | None |

| Mandatory Actions | None | Must convert to RRIF by age 71 [4] |

| Contribution Room | Creates RRSP room (18% of net income) [6] | Consumes room upon withdrawal [5] |

For property owners, these tax benefits mean rental income is taxed more efficiently than RRSP withdrawals. The ability to deduct expenses and generate additional RRSP room creates compounding advantages that can significantly enhance your retirement cash flow over time. Rental properties combine flexibility, equity growth, and tax efficiency in a way that traditional retirement strategies can’t match.

Financial Returns and Financing Options

When assessing rental properties as part of your retirement strategy, focus on two main sources of returns: monthly cash flow and long-term equity growth. Unlike RRSPs or pensions, rental properties generate income through these dual mechanisms. To evaluate immediate returns, use the cash-on-cash (CoC) return metric, which measures how much annual income you earn relative to your upfront investment.

Calculating Cash-on-Cash Returns

Cash-on-cash return is a straightforward calculation that shows the percentage of pre-tax annual cash flow earned on your invested cash [10]. The formula is:

Cash-on-Cash Return (%) = (Annual Pre-Tax Cash Flow / Total Cash Invested) × 100 [10][11].

- Annual Pre-Tax Cash Flow = Net Operating Income (NOI) – annual mortgage payments [10].

- Total Cash Invested = Down payment + Closing costs (typically 1.5–3% in Canada) + Any upfront site development costs [10].

For example, consider a $500,000 duplex financed through CMHC MLI Select. With 5% down ($25,000) and $15,000 in fees, your total upfront investment is $40,000. If this property generates $8,000 in annual net cash flow, the CoC return is:

(8,000 / 40,000) × 100 = 20%.

Compare this to conventional financing, where a 25% down payment plus fees would total $140,000 upfront. The same $8,000 in cash flow yields a much lower CoC return of 5.7%. Most Canadian investors aim for CoC returns between 5–10% on stabilized commercial properties [10], so the CMHC program can significantly outperform these benchmarks.

It’s important to note that higher leverage doesn’t increase your total returns; it simply spreads the same dollar return over a smaller upfront investment, boosting your percentage yield. This is where financing tools like CMHC MLI Select come into play.

CMHC MLI Select Financing: 95% Loan-to-Value

The CMHC MLI Select program allows you to reduce upfront costs while improving cash flow. It offers up to 95% loan-to-value (LTV) financing and amortization periods of up to 50 years [12]. These features lower both your initial investment and your monthly debt service. For example, a 50-year amortization can reduce monthly payments by 30–40% compared to a standard 25-year term [12]. This reduction directly boosts your monthly cash flow and improves your CoC return.

| Feature | CMHC MLI Select | Conventional Financing |

|---|---|---|

| Down Payment | As low as 5% | Typically 20%–25% |

| Amortization | Up to 50 years | Typically 25–30 years |

| LTV Ratio | Up to 95% | Typically 75%–80% |

| DSCR | As low as 1.1x | Typically 1.25x or higher |

For example, consider a fourplex built at Helio's $160,000 per unit pricing, totalling $640,000. With a 5% down payment, your upfront cost is $32,000, plus $18,000–$28,000 in closing and site development costs, resulting in a total investment of $50,000–$60,000. Under conventional financing (25% down), the same project would require $160,000 upfront, plus additional costs, bringing your total to $180,000–$200,000. The difference - $120,000–$140,000 - can be redirected toward building more units or saved as retirement capital.

Helio simplifies this process by ensuring all its designs are pre-qualified for CMHC MLI Select, removing the uncertainty of whether your project will meet eligibility requirements. This financing option not only reduces barriers to entry but also maximizes your potential returns.

Nova Scotia Rental Market Conditions

Nova Scotia’s rental market presents promising opportunities for investors focused on retirement income. The province’s overall vacancy rate has climbed to 2.7% in 2025, up from just 1.0% in 2023, but the affordable housing segment remains critically undersupplied [14][15][17]. Trish McCourt, Executive Director of the Nova Scotia Non-Profit Housing Association, remarked, "My guess would be close to zero" when discussing affordable unit vacancies [15]. Data backs this up, showing that affordable unit vacancy in Halifax edged up only slightly from 0.4% to 0.7%, as most new construction targets mid-to-upper price points [17]. For property owners building fourplexes or eightplexes at Helio’s fixed price of $160,000 per unit, these conditions suggest consistently high occupancy rates. This tight supply in key urban areas underpins strong rental demand, especially for reasonably priced units.

Rental Demand and Vacancy Rates in Halifax and Beyond

Halifax continues to drive Nova Scotia’s economy, contributing 93% of the province’s net real GDP growth in 2025. The city’s rental market reflects this economic momentum, with average monthly rents increasing by 8.0% to $1,745 across all apartment types. For two-bedroom units, the average rent rose 6.7% to $1,826 [14][17]. Turnover leases in Halifax are particularly lucrative, with rents jumping by an average of 23% (around $2,058 for a two-bedroom unit), while rents for sitting tenants grow at a more modest 4% annually [13][16][17]. As CMHC noted, "the significant rent gap between turnover and non-turnover units created a strong financial incentive for tenants to stay in their units" [17].

Secondary markets like Truro also offer compelling investment opportunities. Construction costs in Truro are approximately 15% lower than in Halifax, and municipal fees are significantly reduced - for example, a fourplex permit costs just $240 in Truro compared to over $1,200 in Halifax. These cost savings improve cash-on-cash returns while maintaining steady rental demand, making secondary markets an attractive option for property owners aiming to minimize upfront expenses.

Provincial Incentives and Rent Control Policies

Nova Scotia’s rent control policy caps annual rent increases at 5% for existing tenants, but turnover units are exempt, allowing landlords to reset rents to market levels when tenants move out [16][17]. For retirement-focused investors, this means cash flow projections should account for the 5% cap while factoring in the turnover premium to maximize income. To ensure financial viability, it’s prudent to stress-test pro formas using conservative assumptions, such as an 85% occupancy rate and a 2% annual rent cap.

The province also offers financial incentives to reduce development costs. Provincial HST rebates help lower construction expenses, and when combined with CMHC MLI Select financing - pre-qualified for Helio’s designs - investors may only need $30,000–$40,000 upfront for a fourplex. In Halifax, ER-3 zoning regulations allow up to eight residential units on a single lot, with 50%–60% lot coverage and no minimum parking requirements. These zoning benefits enable higher rental income per square metre and streamline the permitting process through as-of-right approvals. Together, these policies and financing options enhance the efficiency of Helio’s model, making it a strong choice for those planning retirement income through rental property investment.

How to Build Your First Fourplex: A Step-by-Step Process

Building your first fourplex becomes much more manageable when using Helio Urban Development's integrated design-build model. This method simplifies construction into a predictable six-month process with fixed costs, broken down into three straightforward phases: site assessment and design selection, fixed-price contracting with guaranteed timelines, and efficient construction delivery. For property owners aiming to create a retirement income stream, this approach locks in costs at $160,000 per unit - totalling approximately $640,000 for a fourplex. By combining site evaluation, contractual clarity, and streamlined execution, this process ensures your project aligns with your long-term financial goals.

Site Assessment and Design Selection

Helio begins by evaluating potential sites against essential criteria, including zoning compliance for multi-unit residential properties, soil stability for foundations, proximity to transit and schools in Halifax, utility access, and risks like flooding or drainage issues [1][2]. This detailed review ensures your site meets requirements for CMHC financing. Within a few weeks, you'll know if your property is suitable, avoiding expensive redesigns that can derail traditional builds.

Fixed-Price Contracts and 6-Month Construction Timeline

Once the site is approved, Helio's fixed-price contract locks in all costs at $160,000 per unit, or roughly $640,000 for a fourplex. This includes design, permits, materials, and labour, protecting you from the budget overruns often seen in traditional builds. CMHC pre-approved designs simplify the permitting process, cutting approval times by up to 30 days, and qualify for MLI Select insurance, which offers reduced premiums and extended amortization periods [1][18].

The construction timeline is tightly managed, with pre-fabricated components and on-site coordination ensuring efficiency:

- Weeks 1–4: Foundation and framing

- Weeks 5–12: Building envelope and mechanical systems

- Weeks 13–20: Interiors and finishes

- Weeks 21–24: Final inspections and handover

This process is reinforced by expedited financing draws and a $1,000-per-day late penalty, ensuring deadlines are met. In one Halifax project, Helio evaluated the site, selected a pre-approved design, signed a fixed-price $640,000 contract, and delivered a fully operational fourplex within six months. The property was immediately ready for rental, generating positive cash flow [1][2].

How to Avoid Common Construction Problems

Traditional construction often involves juggling multiple contractors, which can lead to coordination issues, delays, and budget overruns. Helio’s model eliminates these challenges by providing single-point accountability and fixed-price terms, avoiding the 20–30% cost increases typical in fragmented projects [1][2]. CMHC pre-approvals further streamline the process, preventing months of delays caused by redesigns. Additionally, MLI Select financing supports up to 95% loan-to-value, ensuring projects stay on schedule and within budget.

For investors focused on retirement income, this approach removes the stress of managing complex construction projects. Instead of spending years dealing with setbacks, you’ll receive the keys in six months and start earning rental income almost immediately. This efficiency makes rental property a reliable addition to your retirement strategy.

Growing Your Rental Portfolio: From Fourplex to Full Retirement Income

Once you've established steady cash flow from your first fourplex, you can use that success as a springboard to grow your portfolio. By tapping into the equity and rental income from your initial property, you can finance additional buildings through CMHC programs. Scaling up from a single fourplex to an eightplex - or even multiple properties - can significantly increase your monthly income while maintaining the same fixed-price, six-month construction timeline.

Income Projections: Fourplex vs. Eightplex

Let’s break down the numbers. A fourplex built for $640,000 typically generates between $7,600 and $9,000 in gross monthly rent in Nova Scotia, translating to $91,200–$108,000 annually. After deducting operating costs like property taxes, insurance, maintenance, and utilities, the average net operating income (NOI) comes to around $65,000 per year. This leaves an annual cash flow of about $43,000.

Now, compare that to an eightplex. At a construction cost of $1,280,000, an eightplex brings in $15,200–$18,000 in monthly rent, or $182,400–$216,000 annually. After expenses, you're looking at a cash flow of roughly $86,000 per year - double that of a fourplex. This jump in cash flow can make a significant difference in funding your retirement, potentially outperforming traditional pension plans.

The financing side adds another layer of benefits. CMHC-insured rental properties often secure interest rates 1% to 1.5% lower than conventional financing for five-year terms, with 10- to 15-year fixed rates available at even lower levels. For example, on a $1,280,000 eightplex, a 1.25% rate reduction saves about $16,000 annually in interest - directly increasing your NOI. These savings compound over time, making CMHC financing a powerful tool for scaling your portfolio.

Using CMHC Financing to Build Additional Properties

CMHC's financing framework is specifically designed to help property owners expand their portfolios. Through the Income Property program, owners can use up to 50% of the gross rental income from existing properties to qualify for new projects. This means every completed building strengthens your ability to fund the next one. As of September 2024, CMHC had committed $20.65 billion through the Apartment Construction Loan Program (ACLP), financing over 53,000 purpose-built rental units with loans ranging from $1,000,000 to 100% of residential construction costs [1].

Refinancing is another key strategy. Once your fourplex is stabilized with steady rental income, you can refinance to unlock equity for your next project. For example, a $640,000 fourplex refinanced at 70% loan-to-value (LTV) can provide $448,000 in capital - more than enough to cover the down payment on an eightplex while keeping the original property cash-flow positive.

This approach allows you to turn one property into a diversified portfolio, with each project creating new opportunities for income growth. By scaling up strategically, you not only increase your monthly revenue but also lay the groundwork for a secure and resilient retirement plan.

Conclusion: Is Building Rental Property Right for Your Retirement?

Building rental properties appeals to those with a long-term outlook who want control over their investments and a steady income stream compared to traditional retirement plans. Rental income can complement CPP and OAS, while also building wealth through equity and delivering consistent monthly cash flow.

That said, no investment is without risks. Interest rate changes, tenant turnover, and regulatory shifts can affect returns. To reduce these risks, consider fixed-price construction contracts, maintain reserve funds for unexpected expenses, and use conservative estimates - such as 85% occupancy rates and 2% annual rent increases - for your financial planning.

Owning rental property isn’t passive; it’s an active business. Even if you hire professional property managers, you’ll need to stay involved in key decisions and maintain financial discipline. This approach is essential to achieving stable, pension-like income over the long term.

As Jim Rohn said, "Discipline is the bridge between goals and accomplishment" [19].

If you already own land or can acquire it, building new rental properties offers predictable costs, efficient timelines, and inflation-adjusted income potential. With a clear plan and sufficient capital, the design-build model ensures a six-month construction timeline, and with CMHC MLI Select financing, you may need as little as 5% down. In Nova Scotia’s strong rental market - where demand remains high and financing options support growth - building rental properties can provide inflation-protected income and long-term financial stability for your retirement.

FAQs

What are the biggest risks of relying on rental income in retirement?

Counting on rental income to fund your retirement isn’t without its challenges. One major risk is the possibility of cash flow problems. If your expenses - like mortgage payments, property taxes, and maintenance - end up being higher than your rental income, you could face financial strain. On top of that, rental income is taxable, which might reduce your eligibility for certain benefits, such as Old Age Security (OAS) in Canada.

Property values and equity can also fluctuate with the market. A downturn could erode your equity or make it harder to sell if you need to free up cash. Managing properties adds another layer of complexity. As you age, dealing with tenant issues, vacancies, or unexpected repairs can become more difficult, making this income feel far less “passive” than it might initially seem.

How much cash do I need upfront to build a fourplex in Nova Scotia?

Building a fourplex in Nova Scotia will set you back about $160,000 per unit in construction costs. On top of that, you’ll need to account for soft costs such as permits, design fees, and other pre-construction expenses. Altogether, the total upfront cash requirement typically lands around $640,000, though the final amount can vary based on site-specific conditions and your financing structure.

What happens to my retirement cash flow if rates rise or a unit sits vacant?

Rising interest rates can push up borrowing costs or monthly mortgage payments, particularly for variable-rate loans. This can cut into your net income. On top of that, vacancies reduce rental income, putting additional pressure on cash flow. That said, in high-demand rental markets like Halifax, vacancy rates tend to stay low, offering some protection against prolonged income gaps.

To navigate these risks, many property owners factor in potential vacancies when budgeting and often adjust rents gradually to keep up with rising expenses. This approach helps maintain a steadier cash flow, which is crucial for anyone relying on rental properties as part of their retirement income.