What Your Financial Advisor Won't Tell You About Building Rental Property

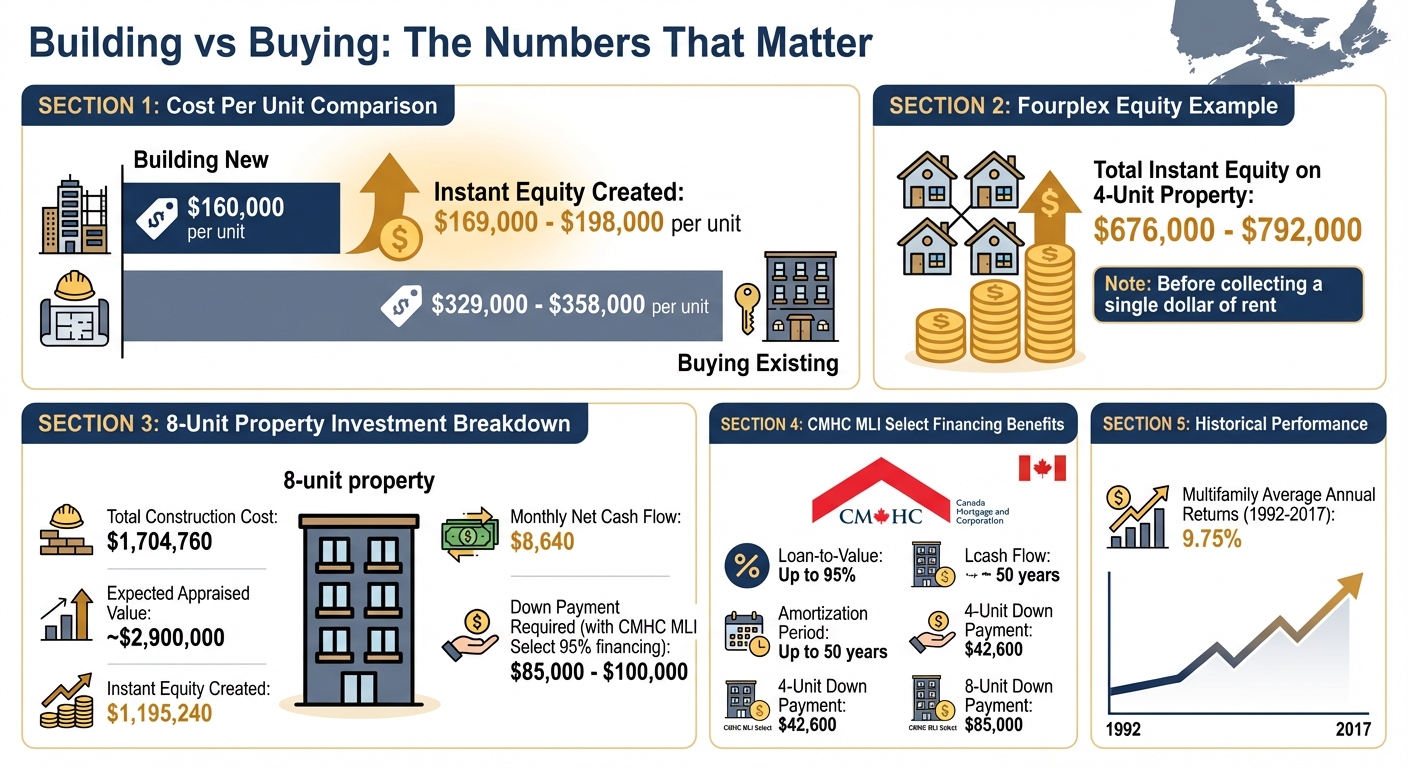

When most people think about investing in real estate, they picture buying an existing property or putting money into REITs. But what if I told you that building a new rental property, especially in Nova Scotia, could cost as little as $160,000 per unit? That’s less than half the price of buying a comparable unit, which often sells for $329,000 to $358,000. The gap creates instant equity - up to $792,000 on a fourplex - before you even collect a single dollar of rent. Add to that CMHC’s MLI Select program, which offers up to 95% financing with amortization periods as long as 50 years, and you’re looking at a much lower upfront investment than you’d need for an existing property.

This article dives into the numbers, financing options, and key steps to help you decide if building rental units aligns with your goals. If you’re tired of hearing the same advice about passive investments, this is the insider knowledge your financial advisor probably isn’t sharing.

Build to Rent: How to Evaluate and Fund Any Deal (Real Estate Development Training)

Why Financial Advisors Don't Recommend Building Rental Properties

Financial advisors often stick to the investment options they know well - typically passive vehicles like mutual funds or REITs. Building multi-unit rental properties falls outside their usual comfort zone, not because the returns are poor, but because construction requires a level of expertise they may lack. As Kenny Loh, Senior Consultant at Financial Alliance Pte Ltd, explains:

"Retirees should enjoy their retirement instead of getting worried about their investment and dealing with property-management hassles" [2].

This mindset leads many advisors to view the construction of rental properties as overly complex and time-intensive.

Most Advisors Don't Understand Construction Economics

A big part of this hesitation comes from a lack of understanding about the financial side of construction. Many advisors are unfamiliar with tools like CMHC MLI Select, which provides attractive financing options with limited-recourse terms. They often assume that financing a multi-unit build is more challenging than purchasing an existing property. However, lenders generally see multifamily buildings as lower risk compared to single-family homes [1][5].

This knowledge gap extends to the per-unit economics of building. For instance, a 10-unit property with a total cost of $1,600,000 works out to $160,000 per unit - often cheaper than buying standalone homes in Nova Scotia [1][4]. Advisors also tend to misjudge vacancy risks. They may focus on the potential hassle of managing multiple tenants and overlook the income stability provided by multiple units. If one unit in a four-plex is vacant, the remaining three still generate 75% of the total rental income. In contrast, a vacancy in a single-family rental drops income to zero [1][4].

Historically, multifamily properties have delivered strong returns. Between 1992 and 2017, they averaged annual returns of 9.75%, outperforming many other real estate types [4]. These factors - lower per-unit costs, income stability, and competitive returns - are often overlooked by advisors who aren't familiar with the nuances of construction investments.

They Stick to Familiar Investment Products

Another reason advisors shy away from recommending rental property construction is their preference for liquid, low-maintenance investments. Products like REITs fit this mould perfectly - they're professionally managed, easy to buy or sell, and require minimal involvement from the investor. As Victor Haghani, Founder and CIO of Elm Wealth, points out:

"discerning private investors should be able to identify individual properties with higher returns than the average REIT‑owned property, they need to generate returns about 4% higher just to catch up with the efficiencies of REITs" [3].

REITs have certain built-in advantages. They often secure borrowing rates around 1% lower than what individual investors can access, and they benefit from economies of scale in property management [3]. These efficiencies make them an attractive option for advisors who prioritize simplicity and liquidity.

For property owners, the key takeaway is that advisors recommend what they know best - not because they're against construction, but because it's outside their expertise. While REITs can offer dividend yields of 5% to 9% [2], building rental properties provides opportunities for instant equity and stronger cash-on-cash returns. However, these benefits do require a more hands-on approach during the construction phase. The numbers behind new builds speak for themselves, even if advisors tend to avoid the complexity.

The Numbers Behind Building Multi-Unit Rental Properties

Building vs Buying Rental Property in Nova Scotia: Cost Comparison and ROI Analysis

Traditional advice often skips over the raw economics of construction in Nova Scotia today. Let’s dig into the specifics to see how building multi-unit rentals stacks up as an investment.

Construction Costs: $160,000 Per Unit Breakdown

In Nova Scotia, constructing a multi-unit rental property costs about $160,000 per unit when using an integrated design-build approach. This price includes everything: planning, construction, and premium finishes such as triple-pane windows, ductless heat pumps, and quartz countertops. It also covers five inspections by a Professional Engineer (P.Eng), ensuring quality at every stage.

Now compare that to the cost of buying recently completed buildings in areas like Eastern Passage or Dartmouth. Those typically sell for $329,000 to $358,000 per unit[6]. The difference - anywhere from $169,000 to $198,000 per unit - translates to instant equity once your project is complete. For a fourplex, that’s $676,000 to $792,000 in equity, even before you start collecting rent. This equity boost happens because integrated construction avoids the multiple contractor markups that inflate costs when you hire six or seven separate trades.

By keeping costs lower, you not only build equity but also position yourself for stronger cash flow.

Cash-on-Cash Returns and Instant Equity

Let’s take an eight-unit property as an example. The total cost to build would be around $1,704,760, but once completed, it’s expected to generate approximately $8,640 in monthly net cash flow and create about $1,195,240 in equity.

With CMHC MLI Select financing covering up to 95% of project costs, the upfront investment needed is surprisingly low - typically between $85,000 and $100,000 for an eight-unit building.

This combination of instant equity and steady cash flow highlights why building from scratch can outperform traditional real estate purchases in today’s market.

Using CMHC MLI Select Financing to Maximize Leverage

When it comes to new rental construction, CMHC MLI Select financing can make a major difference in how far your investment dollars go. This program is tailored for multi-unit rental developments and offers some of the most attractive financing terms available.

What CMHC MLI Select Offers

CMHC MLI Select is a mortgage insurance program specifically designed for rental properties with five or more units. It allows property owners to borrow up to 95% of the project cost, meaning you only need a 5% down payment. For example, if you're planning to build an eight-unit rental property with a total cost of $1,280,000, your down payment would be just $64,000 - far less than what conventional financing would require[7][9].

The program operates on a points system, awarding credits for affordability, energy efficiency, and accessibility. The more points you earn, the better the terms. For instance:

- 50 points: 95% financing with a 40-year amortization

- 70 points: 95% financing with a 45-year amortization

- 100 points: 95% financing with a 50-year amortization

Longer amortization periods reduce monthly payments, which boosts cash-on-cash returns. Another advantage is the debt service coverage ratio (DSCR) requirement - MLI Select allows a DSCR as low as 1.10, compared to the 1.20–1.30 range typically required by conventional lenders[7][9].

In 2023 alone, over 127,000 rental units across Canada were insured through MLI Select[8]. Despite its growing popularity, many property owners are still unaware of how this program can reshape their project financing.

However, securing these favourable terms isn’t automatic - your building must meet CMHC’s design criteria.

Meeting CMHC Pre-Approved Design Requirements

To qualify for MLI Select financing, your project needs to align with CMHC’s specific design standards. One straightforward way to earn the required 50 points is by dedicating 10% of your units to affordable rents. CMHC defines affordable rent as no more than 30% of the median renter income in your municipality[9]. For example, if the median renter income is $39,600, affordable rent would be capped at $990 per month. This commitment must be maintained for at least 10 years.

Additional points can be earned by incorporating energy efficiency measures - achieving 20% to 40% greater efficiency than the standard building code - or by including accessibility features, such as ensuring 15% of units meet CSA B651:23 accessibility standards[7]. Energy efficiency improvements need validation from accredited professionals like Professional Engineers, Architects, or Certified Energy Managers[7].

When working with pre-qualified CMHC designs, such as those provided by Helio Urban Development, these requirements are integrated into the planning phase. This approach eliminates guesswork and reduces the risk of delays in securing financing.

What this means for property owners: By using CMHC-certified designs and an integrated design-build approach, you can secure 95% financing before construction even begins. This drastically lowers your initial capital outlay compared to traditional financing methods. For property owners in Nova Scotia, this streamlined process makes build-to-rent projects a far more accessible and appealing option.

sbb-itb-16b8a48

Building Multiple Properties to Scale Your Portfolio

After completing your first rental property, you don’t have to wait years or save another massive down payment to build the next one. By tapping into the equity created through new construction and using CMHC MLI Select financing, you can grow your portfolio much faster than many expect.

How Leverage Drives Portfolio Growth

The key is using the equity from your first project to fund the next. For example, if you’re building at $160,000 per unit and the completed property appraises at a much higher market value, you’re creating equity right from the start. Let’s say you develop an eight-unit building with total costs around $1,704,760. If the property appraises at approximately $2,900,000, you’ve generated about $1,195,240 in equity. That equity can then help secure financing for your next project - no need to save up another full down payment.

CMHC MLI Select’s 95% loan-to-value (LTV) financing is another game changer. For an eight-unit project, you’d typically need just $85,000 down; for a four-unit project, it’s around $42,600. Once the building is complete, the monthly net cash flow - approximately $8,640 for an eight-unit property or $4,320 for a four-unit - can further strengthen your financial position. Within 12 to 18 months of finishing your first project, you could refinance the equity to cover the down payment for your next build.

This method stands in stark contrast to purchasing existing properties, where you’re paying market value without building equity upfront. As Tim Allenby, Chair of ACORN Dartmouth, states, “landlords benefit from primarily relying on fixed-term leases, so of course that's going to end up being an investment benefit” [10]. Additionally, new builds allow you to set market rents immediately, sidestepping Nova Scotia’s 5% rent cap for existing tenants [10][11]. Plus, with the 100% GST rebate available for new rental projects of 10 or more units (for construction starting after September 13, 2023) [12], the financial case for building multiple properties becomes even stronger.

By reinvesting this built equity, you can identify and secure your next project, steadily advancing your portfolio.

Planning Your Next Build

To keep the momentum going, start scouting for your second site while your first project is still underway. In Halifax, multi-unit development often requires land zoned for properties like ER-3, with minimum lot sizes of 600–700 m² for five or more units. Set aside $3,000 to $5,000 for professional site evaluations, including geotechnical studies and utility checks, to avoid unexpected issues mid-project.

What Nova Scotia Property Owners Should Know

Following a step-by-step guide to building in Nova Scotia is crucial for navigating zoning and permitting rules while staying on track with your project’s timeline and budget. For multi-unit developments, R-3 (Multi-family) zoning is typically required, as it permits apartments and higher-density housing compared to R-1 or R-2 zones [13][17]. Before purchasing land, confirm its zoning using tools like Halifax's ViewPoint or the Nova Scotia Geomatics Centre [13]. A RE/MAX Nova representative highlights the importance of this:

"The reality is that there is no such thing as an 'in-law suite' when it comes to zoning & properties in HRM. Unless the property has the appropriate zoning and permits to allow for multi-family use (ie. R2), HRM can force the owner to remove those second unit features" [17].

Understanding zoning is just the first step. You'll also need various permits: a Development Permit (to confirm land use compliance), a Building Permit (to ensure structural safety), and potentially Lot Grading or Water/Sewer permits [14][15]. For larger projects - anything over four units or 600 sq. ft - permit approval requires architectural drawings and structural engineering reports stamped by a P.Eng [15][16]. In areas with high demand, like East Hants, the permitting process can take six to ten weeks [15].

Why this matters for property owners: Coordinating permits, engineering, and design can be overwhelming. An integrated design-build firm simplifies this process by handling everything in-house. If your designs are pre-qualified for CMHC MLI Select financing, you can cut down on permitting delays and access up to 95% loan-to-value financing. For a four-unit building, this means you could start with as little as $42,600 down.

Municipal parking requirements also play a role. Most municipalities require one to two parking spaces per unit [13][14]. Development standards often dictate setbacks of about 20–30 ft at the front, 25 ft at the rear, and 5–10 ft on the sides, along with maximum building heights (commonly 35 ft for residential) and lot coverage limits [13]. For questions about optimizing density or obtaining variances, municipal planning offices usually offer free consultations with zoning officers [13]. This kind of local expertise makes an integrated approach even more valuable, ensuring every detail of your build aligns with regulations.

Conclusion

Financial advisors often avoid recommending rental property construction, largely because they’re more comfortable with traditional investments like stocks and bonds. They also tend to lack a deep understanding of construction economics. But the numbers tell a different story. Fixed, predictable unit pricing builds immediate equity, eliminates the need for costly retrofits on older properties, and generates stable cash flow right from the start. For instance, an eight-unit building can provide net income comparable to a full-time salary while also building long-term wealth through equity growth and mortgage paydown.

Using CMHC MLI Select financing and fixed-price contracts addresses two of the biggest hurdles: the large upfront capital requirements and the uncertainty of construction budgets. Traditional cost-plus contracts often lead to overruns and coordination headaches, but an integrated design-build approach simplifies everything - one contract, one price, and a clear timeline. Purpose-built rentals are also about 25% cheaper to maintain and provide steady income, even when a unit is temporarily vacant. This approach doesn’t just improve returns; it reshapes how wealth can be built in Nova Scotia’s rental market.

With a $42,600 down payment, you could start building a fourplex and grow your portfolio using the equity you create. Nova Scotia’s rental market, backed by low vacancy rates and strong demand for modern, energy-efficient housing, makes this strategy even more compelling. By managing the construction process from day one, you avoid hidden costs like structural issues, energy inefficiencies, and code compliance problems. Instead, you’re creating an investment designed to deliver consistent, predictable returns.

FAQs

What are the biggest risks when building a multi-unit rental?

Building a multi-unit rental in Nova Scotia comes with three major risks: budget overruns, delays, and compliance challenges. If construction costs are underestimated, you could see expenses climb by 30–60%. Delays - whether caused by weather, labour shortages, or slow permit approvals - can cut into your rental income, sometimes by months. On top of that, meeting zoning laws and NECB 2020 energy standards can demand pricey changes mid-project. Opting for an integrated design-build approach with fixed costs and timelines is one way to keep these risks in check and ensure the project stays on track.

How do I qualify for CMHC MLI Select financing?

To access CMHC MLI Select financing, your project needs to satisfy specific program requirements. This means presenting clear development plans, a practical budget, and proof of effective property management skills. The program assesses applications with a points-based system, focusing on factors like rent affordability, alignment with local market needs, and the overall feasibility of the project.

How soon can I refinance and build the next property?

Refinancing is generally an option 6 to 12 months after completing construction, though the exact timing depends on your loan type and the lender's terms. Conventional loans often offer the flexibility to refinance earlier. To avoid delays, ensure you meet all the lender's conditions before starting the process.