The Real Estate Investment Blind Spot: Why Nobody Talks About Building New

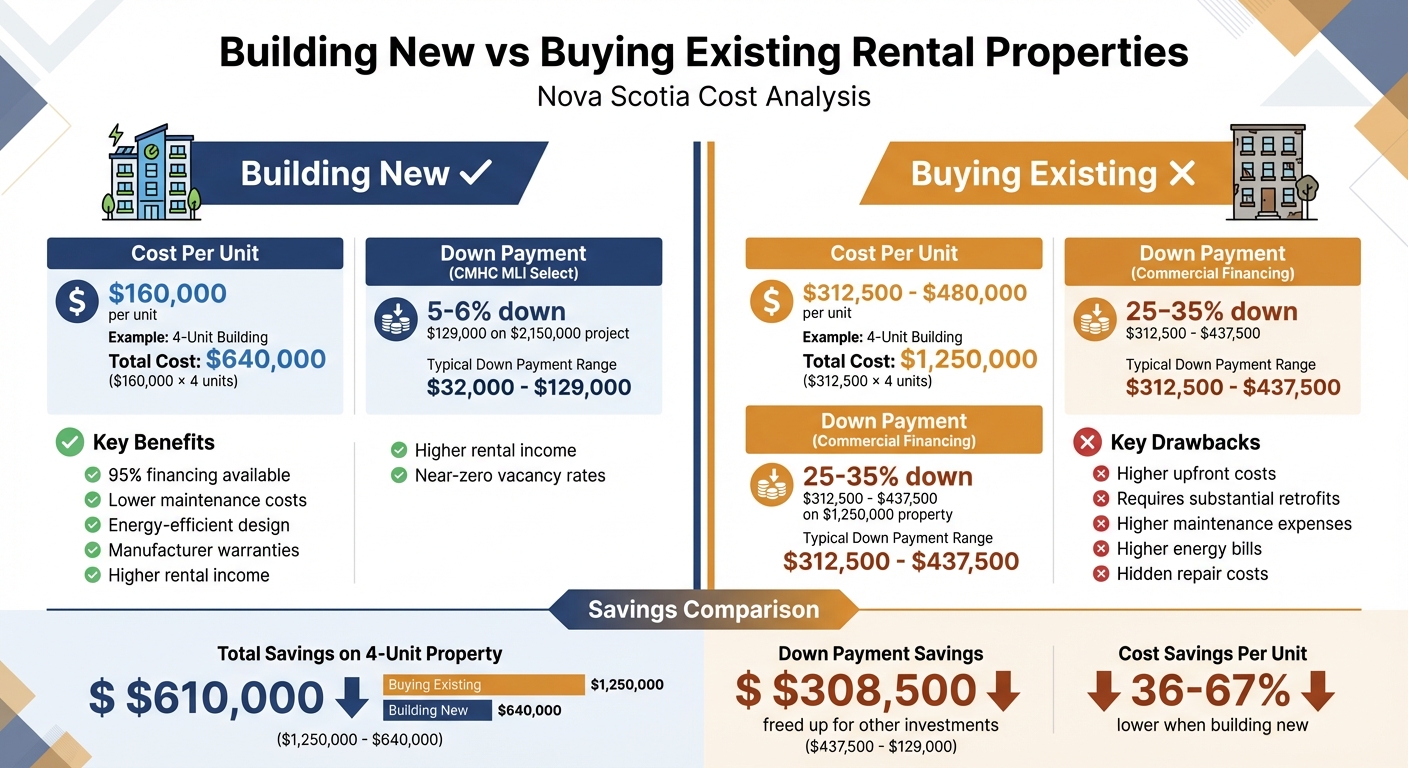

If you’re trying to figure out whether building a rental property in Nova Scotia makes sense, let’s start with the numbers. Buying an existing fourplex in Halifax costs between $312,500 and $480,000 per unit, but building one from scratch averages $160,000 per unit. That’s a savings of 36–67% per unit. Add to that CMHC’s MLI Select program, which lets you finance up to 95% of the project cost, and you’re looking at a much lower upfront investment compared to buying existing properties.

This article breaks down why building new is often overlooked, how the costs compare, and what you need to know about financing, timelines, and risks. If you own land or are thinking about investing in Nova Scotia’s rental market, this guide will help you decide if building is the smarter move.

The Numbers: Why Building New Costs Less

Building vs Buying Rental Properties in Nova Scotia: Cost Comparison

Cost Per Unit: New Construction vs. Existing Properties

In Nova Scotia, building new costs around $160,000 per unit, compared to $312,500–$480,000 per unit for existing properties.

Take recent sales in Halifax as examples: a fourplex on Williams Street listed for $1,250,000, which works out to $312,500 per unit. An eight-unit building on Clyde Street sold for $2,995,000, or roughly $374,375 per unit. A newer eight-unit property on Highland Avenue fetched $3,840,000, breaking down to $480,000 per unit. Even in Dartmouth, a relatively modern six-unit building priced at $2,150,000 came to $358,333 per unit - more than double the cost of building new.

Now, compare that to constructing a fourplex for $640,000 (4 × $160,000). That’s a saving of $610,000 over purchasing the $1,250,000 fourplex. This difference can be directed toward other investments or used to reduce financing costs. Lower unit costs also mean better cash flow and stronger long-term returns.

Return on Investment: Cash Flow and Long-Term Gains

Lower costs upfront directly improve your bottom line. New builds typically generate better cash flow thanks to higher rental income, reduced maintenance expenses, and lower energy bills. Modern construction methods, like insulated concrete forms, metal roofing, and ductless heat pumps, not only cut maintenance to a minimum but often come with warranties covering major systems for the first two years. Energy-efficient designs reduce utility costs and appeal to tenants, especially when the layouts - like two-bedroom, two-bathroom units - match high-demand market preferences. These types of units often maintain near-zero vacancy rates.

In contrast, existing properties often require substantial retrofits, eating into any initial "savings" from the purchase price. With new construction, the improved cash flow is further amplified by financing options tailored specifically for these types of projects.

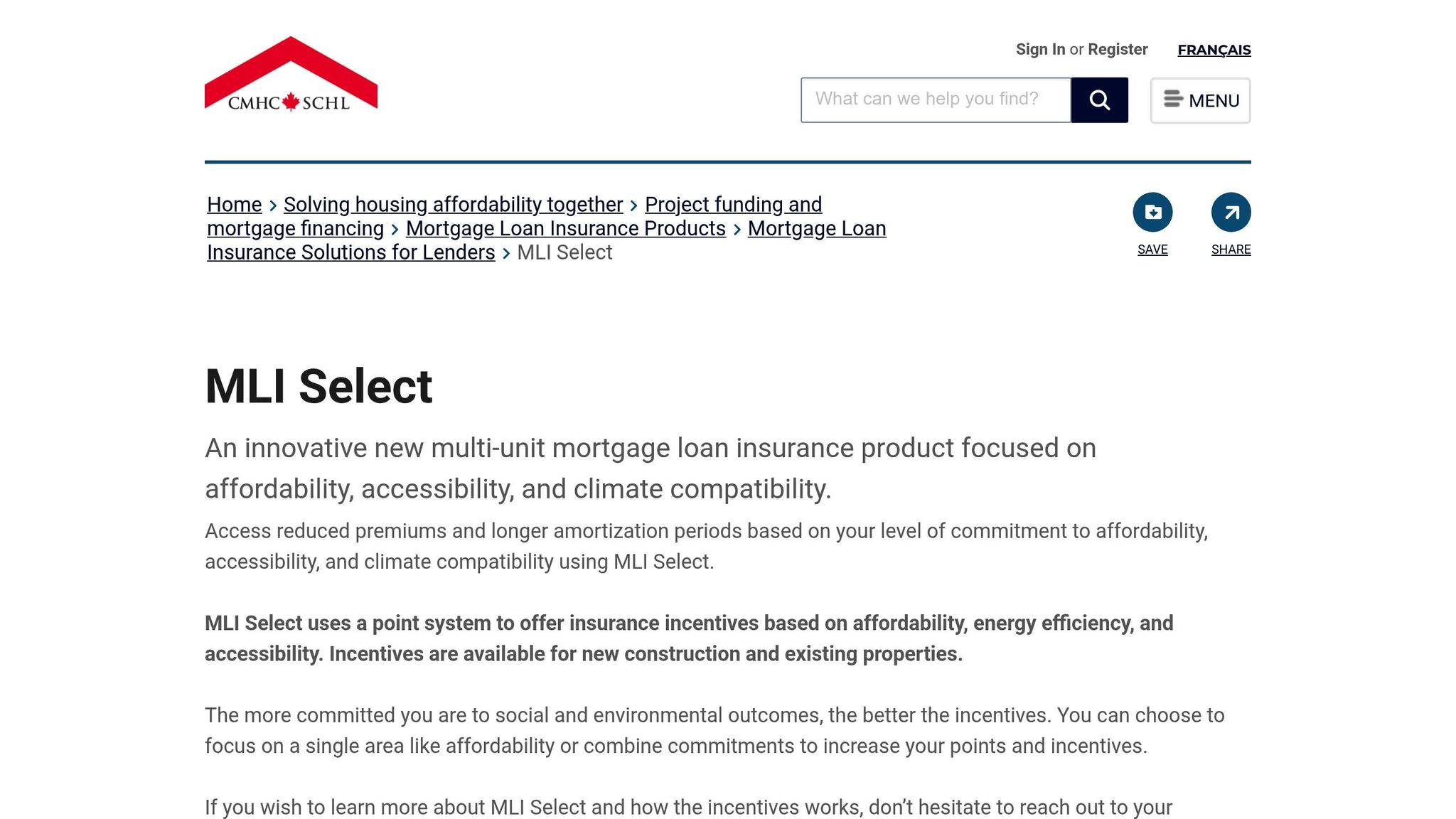

CMHC MLI Select: 95% Financing for New Builds

Financing is a game-changer when it comes to new builds. The CMHC MLI Select program offers up to 95% loan-to-value financing for qualifying projects, meaning you can start with as little as a 5% down payment. For instance, a six-unit building in Dartmouth recently qualified for the program with just 6% down - about $129,000 on a $2,150,000 project.

Compare that to standard commercial financing for existing properties, which typically requires 25% to 35% down. On a $1,250,000 fourplex, that means an upfront payment of $312,500 to $437,500. With MLI Select, you’d only need $129,000 instead of $437,500, freeing up approximately $308,500 for other investments or to lower your overall financing risk.

David Chen, a property investor in Nova Scotia, shared his experience:

The fixed pricing model let me lock in my financing with confidence. My lender appreciated the guaranteed pricing for every line item.

This pricing certainty is a major draw for lenders and one of the reasons CMHC programs are designed to encourage new construction over purchasing existing properties.

sbb-itb-16b8a48

Common Myths About Building New (And Why They're Wrong)

Myth 1: Construction Projects Always Run Late

Delays aren’t inevitable. They often happen when property owners hire multiple independent contractors - like architects, engineers, general contractors, tradespeople, surveyors, and project managers - who fail to communicate effectively. The solution? Integrated design-build companies. By consolidating all roles under one team, these companies eliminate coordination breakdowns. At Helio Urban Development, for instance, every project comes with a 6-month guaranteed timeline from permit to keys. To drive the point home, Helio even includes a $1,000-per-day late penalty in its contracts if the deadline is missed. This level of confidence stems from having one team manage both design and construction.

Government programs recognize the importance of this approach. Nova Scotia’s Affordable Housing Development Program, for example, requires developers to either have a proven track record of completing similar projects on time and on budget or to work with a general contractor under a fixed-price contract [2]. Fixed timelines aren’t just a perk - they’re often a requirement for securing funding.

Myth 2: Construction Costs Always Go Over Budget

Cost overruns are common with traditional contracts that leave too much room for surprises. Cost-plus contracts, which charge a percentage markup on actual expenses, give contractors little incentive to control spending. On top of that, change orders during construction can push costs far beyond initial estimates.

Fixed-price contracts eliminate this uncertainty. For example, if you sign a fixed-price agreement to build a fourplex for $640,000, that’s the final cost - no surprise invoices, no creeping budgets. This clarity is why lenders and government housing programs prefer fixed-price contracts. Nova Scotia’s affordable housing loan program, for instance, requires applicants to either have a history of delivering projects on time and on budget or to work with an experienced general contractor under a fixed-price agreement [2].

That said, it’s still smart to set aside extra funds as a contingency for unforeseen issues. While fixed-price contracts provide financial certainty, having a buffer ensures you’re prepared for any unexpected challenges.

Myth 3: You Need Developer Experience to Build

You don’t need a background in construction or development to build a rental property - you need the right team. Nova Scotia’s housing programs make this clear. If you lack five years of property management experience, you’re required to hire a professional management company [2]. The same principle applies to construction. Property owners can access government funding by partnering with experienced contractors.

Take the example of a six-unit building at 80 Cannon Terrace in Dartmouth, completed in March 2026. It was marketed as a turnkey investment for the CMHC MLI Select program, allowing buyers to enter with as little as 6% down [1][3]. For those who prefer to build rather than buy, integrated design-build teams handle everything - architecture, engineering, permitting, construction, and project management - under a single contract. Provincial housing departments even assign “affordable housing specialists” to guide developers through the proposal and evaluation process [2].

In short, you don’t need to know how to swing a hammer or draft blueprints. What you do need is a team with the right systems and a proven track record to help you navigate the process.

Why Nova Scotia's Market Favours New Construction

Nova Scotia's Rental Shortage: More Demand Than Supply

From 2024 to 2025, Nova Scotia's population grew by over 20,000 people, with most of this surge concentrated in Halifax. This rapid growth has far outpaced the available rental supply, creating a tight market where vacancy risk is minimal, and landlords have stronger leverage in rent negotiations [4]. For property owners, this translates into more stable occupancy and the potential for higher rental income. Adding to this, government initiatives help offset construction costs, making new builds an attractive option in today’s market.

Government Programs That Lower Construction Costs

The CMHC MLI Select program provides up to 95% financing and allows for amortization periods of up to 50 years, significantly lowering upfront financial barriers. Even first-time developers can take advantage of this program by partnering with experienced property managers, as long as they meet net worth and liquidity requirements - 25% and 10% of the project cost, respectively [5][7][8][9]. These kinds of incentives make constructing new properties in Nova Scotia a more financially appealing choice compared to buying existing ones. Lower initial expenses and improved project feasibility are key benefits of these programs.

New Buildings Attract Better Tenants and Lower Costs

Modern buildings come equipped with manufacturer warranties on major systems and are designed with energy-efficient features, which help keep maintenance expenses low. Units with updated finishes and layouts also tend to attract tenants who are willing to pay higher rents and are more likely to stay longer. This means fewer turnovers and less time spent on repairs, especially during the first 10 years of ownership. These operational efficiencies, combined with the ability to attract higher-quality tenants, contribute to stronger returns over the long term.

How to Decide: Should You Build or Buy?

Choosing between building a new rental property or buying an existing one comes down to three straightforward questions: Is your land suitable, do the financials make sense, and can you handle the risks? Many investors skip over key calculations related to these factors, which can lead to costly mistakes. Here's a framework to help you assess whether developing a property is the right move for you, especially in Nova Scotia's rental market.

Evaluating Your Land for Multi-Unit Development

The first step is to confirm whether your land meets the basic requirements for multi-unit construction. To qualify for CMHC MLI Select financing, your property must be zoned for at least five rental units[6][9]. This makes zoning verification an essential task. Start by contacting your municipal planning department to confirm the zoning status. In many areas within 90 minutes of Halifax, multi-unit zoning is already in place, but some locations may require rezoning. If rezoning is necessary, expect it to add three to six months to your timeline.

Beyond zoning, assess the physical readiness of your site. This includes commissioning an environmental assessment, ensuring utilities (like water and sewer) are accessible, and confirming that the lot meets setback and parking requirements. For property owners with residential lots in growth areas, this step could reveal untapped development potential.

Running the Numbers: Project Costs and Cash Flow

Once your land checks out, it's time to crunch the numbers. Start with a pro forma that breaks down construction costs, financing, and projected rental income. For instance, building a fourplex at $160,000 per unit adds up to $640,000 in construction costs. On top of that, factor in site development expenses - typically $10,000 to $25,000 depending on site conditions - and municipal fees.

Next, calculate your debt service coverage ratio (DSCR). To qualify for financing, this ratio must be at least 1.10×. If your project scores 70 or more points on CMHC's criteria for affordability, energy efficiency, and accessibility, you could also secure a 45-year amortization period. This extended timeline reduces monthly payments, improving cash flow and boosting long-term returns. With these numbers in place, you’ll be ready to tackle the next challenge: managing construction risks.

Understanding Risks and Exit Options

Construction always comes with risks, such as cost overruns and delays. Fixed-price contracts are a solid way to manage these risks. For example, contracts with late penalties - like $1,000 per day for missed deadlines - shift the burden of delays onto the contractor. These agreements also eliminate the inefficiencies of hiring multiple subcontractors, which can lead to inflated costs.

Once your property is complete, you’ll have several exit options. You can hold onto the building for rental income, which becomes especially appealing if you qualify for up to a 50-year amortization period by scoring 100+ points on CMHC’s system. Alternatively, you can refinance the property once rental income stabilizes, taking advantage of improved terms, or sell the building at market value. Building new gives you more control over costs and timelines compared to buying existing properties, which often come with hidden maintenance issues.

Conclusion: Building New as a Practical Investment Strategy

Constructing new multi-unit rentals offers clear financial advantages and operational benefits that are hard to ignore. In Nova Scotia, building costs average $160,000 per unit - up to 36% less than purchasing existing properties, which often exceed $250,000 per unit. Financing options further enhance this appeal, with programs like CMHC MLI Select allowing entry with as little as a 6% down payment. For example, the 80 Cannon Terrace project in Dartmouth exemplifies how these financing options can make new construction accessible[1].

New builds also bring operational efficiencies that older properties simply can't match. Using durable materials and energy-efficient systems, they minimize maintenance headaches and unplanned repair expenses. Projects like 3620 Highland Avenue demonstrate how new construction can achieve near-zero vacancy rates and immediate revenue generation, eliminating the need for costly renovations from day one[1].

These benefits are amplified by fixed-price contracts and guaranteed timelines. With agreements that include $1,000-per-day late penalties and a 6-month construction guarantee, investors gain predictability and control - qualities often lacking in traditional property acquisitions. This structure allows rental income to flow right away, without the delays or surprises that come with renovating older buildings.

When you combine lower upfront costs, favourable financing terms, reduced maintenance expenses, and higher tenant retention, it’s clear that building new outshines buying existing properties. For landowners with multi-unit zoning within 90 minutes of Halifax, this approach offers a straightforward path to generating rental income. With financing tools like CMHC MLI Select, new construction in Nova Scotia consistently delivers stronger financial outcomes compared to traditional buying strategies. The real question is whether you’re ready to seize this often-overlooked opportunity.

FAQs

What are the hidden costs when building a new rental (soft costs, fees, servicing)?

Building a rental property in Nova Scotia comes with expenses that go beyond just construction. There are soft costs, which include permits, municipal fees, and financing charges like interest on construction loans. On top of that, servicing costs - things like utility hookups, site infrastructure, and environmental assessments - can quickly pile up. Delays caused by weather, labour shortages, or permit approvals can also drive up your expenses. This makes thorough financial planning and securing fixed-price contracts critical to keeping your project on budget.

Do I qualify for CMHC MLI Select, and what down payment will I really need?

You might be eligible for CMHC MLI Select with a down payment as low as 5%. For an $800,000 project, that works out to about $40,000. However, the exact amount and eligibility will depend on your financial details and the specifics of your project.

How can I quickly check if my land supports 5+ units (zoning, parking, services)?

To determine if your land can accommodate 5 or more units, begin by examining local zoning regulations and permit requirements. Contact your municipal planning office or consult land use bylaws to confirm whether multi-unit development is permitted. Check if any variances or special permissions might be necessary. Don’t overlook parking requirements and ensure the property has access to essential services such as water, sewer connections, and utilities. A quick phone call to your municipal planning office can help clarify these details early on.