How Depreciation Works on New-Build Rental Properties in Canada

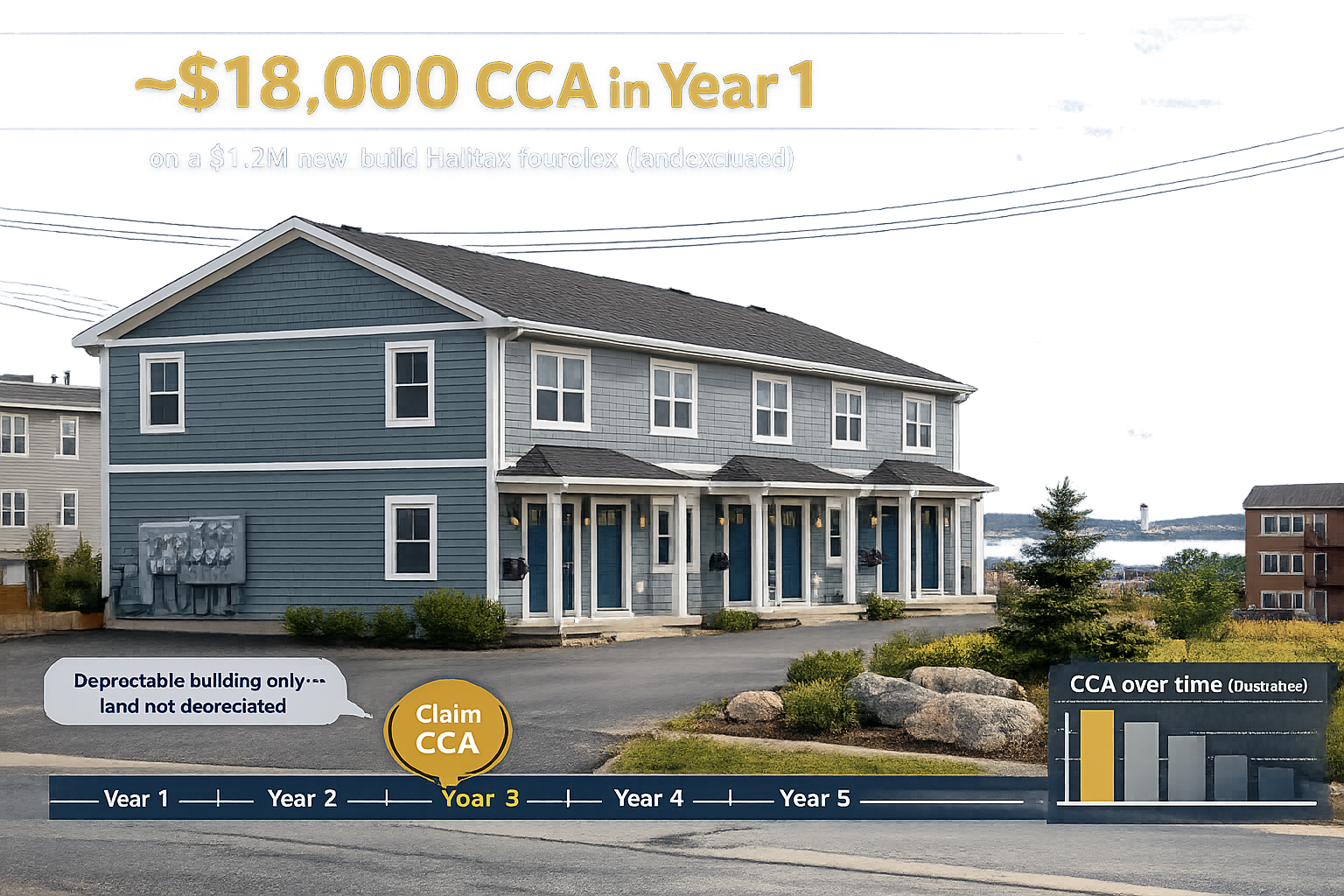

You’re probably here because you’ve heard about depreciation (or Capital Cost Allowance, CCA) and want to know how it can save you money on taxes for your Nova Scotia rental property. Let’s cut to it: if you’ve built a new fourplex in Halifax for $1.2 million, with $300,000 allocated to land, you could claim around $18,000 in depreciation in Year 1. That’s $7,200 in tax savings if you’re in a 40% tax bracket - and it doesn’t touch your cash flow. This guide will explain how CCA works, how to calculate it, and when to use it to maximize your returns.

Should you claim CCA on your rental property?

sbb-itb-16b8a48

How Capital Cost Allowance (CCA) Works for Rental Properties

CCA Depreciation Classes and Rates for Canadian Rental Properties

Capital Cost Allowance (CCA) plays a critical role in managing tax obligations for newly built rental properties. It allows property owners to spread the cost of a building's depreciation over its useful life, rather than deducting the entire expense in the year construction is completed. For example, if you’ve just built a fourplex, CCA lets you claim deductions gradually, reflecting the building’s long-term value rather than taking a one-time hit [1].

The process starts by separating the cost of the land from the building. Land itself doesn’t qualify for depreciation - only the building and its components are eligible for CCA [1]. This distinction is crucial for calculating deductions accurately.

Why this matters: You can choose to claim all, part, or none of the CCA in a given year, which gives you flexibility to align deductions with your income situation. For instance, if you're running a rental loss or planning to sell, this flexibility can help reduce recapture taxes [1].

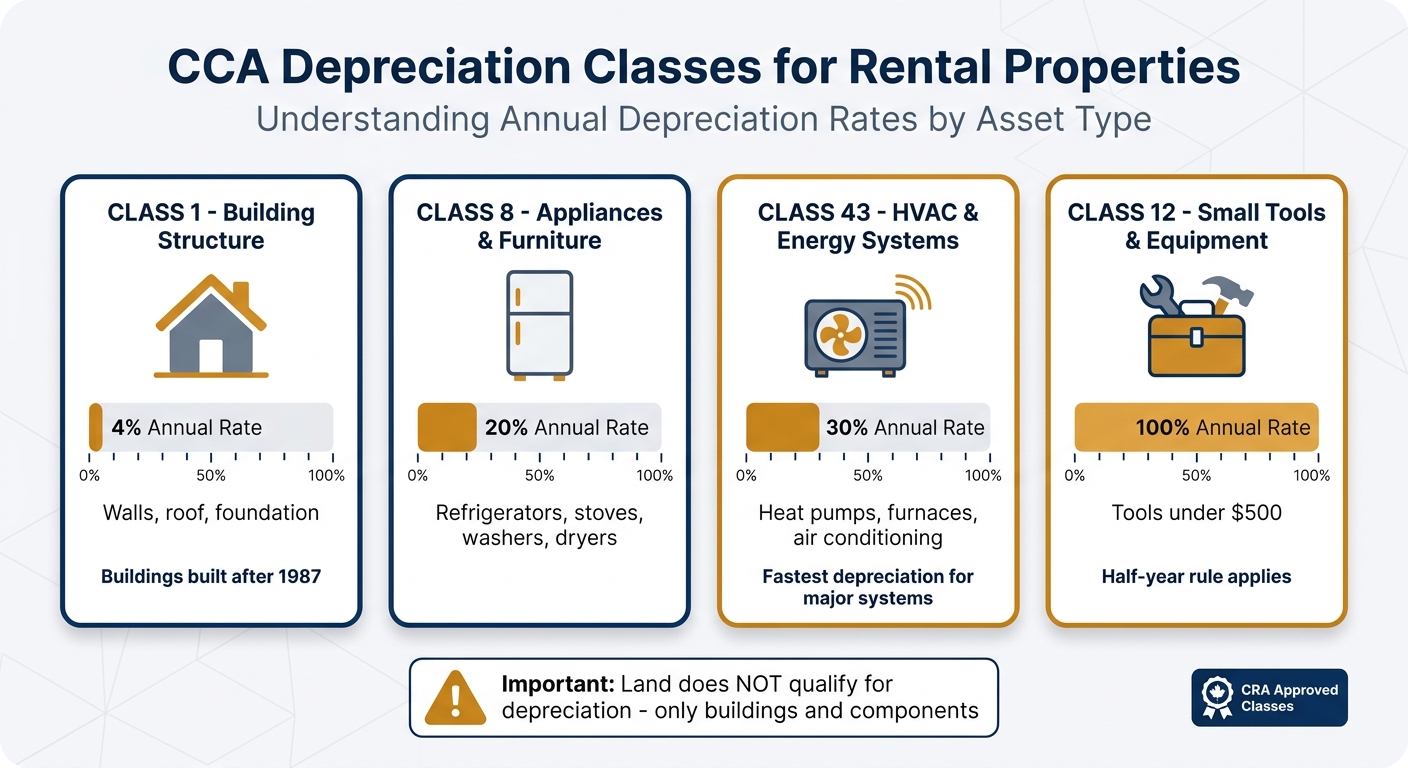

Depreciation Classes and Rates for New-Build Properties

The Canada Revenue Agency (CRA) assigns depreciation rates based on an asset’s expected lifespan. Most rental buildings built after 1987 fall under Class 1, which depreciates at a rate of 4% annually [1]. According to Landlii.ca:

"The 4% rule is slow... This is intentional - CRA expects buildings to last decades" [1].

Other components, such as appliances and mechanical systems, depreciate at faster rates because they wear out sooner. Below is a breakdown of common CCA classes for multi-unit rental properties:

| CCA Class | Asset Type | Annual Rate | Examples |

|---|---|---|---|

| Class 1 | Building structure | 4% | Walls, roof, foundation |

| Class 8 | Appliances and furniture | 20% | Refrigerators, stoves, washers, dryers |

| Class 43 | HVAC and energy systems | 30% | Heat pumps, furnaces, air conditioning |

| Class 12 | Small tools and equipment | 100% | Tools under $500 (half-year rule applies) |

For Nova Scotia property owners, installing energy-efficient heat pumps - a common choice to meet updated building codes - can result in faster tax deductions. With a 30% depreciation rate under Class 43, a $20,000 heat pump system could provide a much larger first-year deduction compared to the 4% rate for the building structure. This can improve cash flow during the early years of ownership.

How the Declining Balance Method Works

The declining balance method determines how CCA is applied yearly. Instead of deducting the same amount annually (as in straight-line depreciation), this method calculates deductions based on the remaining balance of the asset - called the Undepreciated Capital Cost (UCC).

As Landlii.ca explains:

"The CCA rate is applied to your Undepreciated Capital Cost (UCC) - the remaining balance of the asset after previous years' depreciation" [1].

Here’s how it works in practice: imagine you install a $5,000 furnace in a Halifax fourplex. In the first year, you can only claim half the rate due to the half-year rule. So, 30% of $2,500 equals a $750 deduction, leaving a UCC of $4,250. In Year 2, applying the full 30% rate to the $4,250 balance results in a $1,275 deduction, reducing the UCC to $2,975. By Year 3, the claim would be 30% of $2,975, or about $893. Each year, the deduction decreases as it’s based on the lower UCC, continuing until the asset is sold.

This method is particularly useful for forecasting tax savings and planning for long-term growth in your rental portfolio. By understanding how CCA works, you can better manage your cash flow and make informed decisions about reinvesting in your properties.

Rules and Limitations When Claiming Depreciation

Claiming Capital Cost Allowance (CCA) can reduce your taxes, but the Canada Revenue Agency (CRA) imposes strict rules on how and when you can use it. Knowing these rules helps you avoid surprises and make better decisions about your investments. Here’s a breakdown of the key limitations.

The Half-Year Rule for First-Year Claims

The half-year rule restricts your first-year CCA claim to 50% of the usual rate, no matter when you buy the property during the year [1]. For example, whether you purchase a fourplex in January or December, the rule applies the same way. If you own a Class 1 building with a typical 4% depreciation rate, you can only claim 2% in the first year. On a $400,000 building (excluding the land value), this means your deduction is capped at $4,000 instead of $8,000 [1].

This rule isn’t limited to buildings - it applies to all asset classes. For instance, a Class 43 HVAC system with a 30% depreciation rate is limited to a 15% claim in the first year [1].

Beyond this initial limitation, there are other rules to consider for long-term planning.

CCA Recapture When You Sell

When you sell a property for more than its undepreciated capital cost (UCC), the CRA reclaims the depreciation you’ve claimed by taxing it as regular income, not at the lower capital gains rate [3][4]. If the sale price also exceeds your original purchase price, you’ll face both recapture (on past CCA claims) and capital gains tax (on the amount above the original cost) [3][4].

What this means for you: If you plan to sell a property within a few years, claiming the maximum CCA might not be the smartest move. The tax savings you enjoy now could be outweighed by a hefty recapture bill when you sell. Since claiming CCA is optional, you can choose to claim less - or skip it altogether - to reduce future recapture [1][4].

CCA Cannot Create a Rental Loss

The CRA doesn’t allow you to use CCA to create or increase a rental loss [3]. You can only claim enough CCA to bring your rental income down to zero - it can’t be used to offset other types of income, like employment or business earnings. For example, if your rental expenses (like mortgage interest, property taxes, and maintenance) already exceed your rental income, you won’t be able to claim CCA for that year [1][3]. As Kinden CPA puts it:

"One can't use a CCA claim to produce a rental loss" [3].

The good news is that unclaimed CCA isn’t lost. It carries forward indefinitely, so you can use it in future years when your property is profitable or when you’re in a higher tax bracket [1][3]. Knowing these restrictions helps you plan your tax strategy and maximize your investment returns over time.

CCA Calculation Examples for New-Build Properties

Building on the depreciation rules discussed earlier, let’s break down how CCA calculations work with a detailed example. This will focus on a new-build fourplex in Nova Scotia, showing how depreciation impacts taxes over the years.

Year-by-Year Depreciation for a Fourplex

Take a fourplex in Halifax with a total cost of $640,000 ($160,000 per unit). Out of this, $140,000 is allocated to land (non-depreciable), leaving $500,000 for the building and related assets. These are divided into different CCA classes: $440,000 for the building structure (Class 1, 4% annual rate), $40,000 for a heat pump system (Class 43, 30% rate), and $20,000 for appliances (Class 8, 20% rate).

Year 1: The half-year rule applies, so only 50% of the annual rate is used for the first year. For Class 1, $440,000 at 2% results in an $8,800 deduction. The heat pump (Class 43) gets a 15% deduction, or $6,000, and the appliances (Class 8) are deducted at 10%, totalling $2,000. Altogether, the first-year CCA deduction amounts to $16,800.

Year 2: Moving into the second year, the undepreciated capital cost (UCC) for each class is adjusted:

- Class 1 (Building): UCC is $431,200 ($440,000 minus $8,800). At 4%, the deduction is $17,248.

- Class 43 (Heat Pump): UCC is $34,000 after Year 1, leading to a $10,200 deduction at 30%.

- Class 8 (Appliances): UCC is $18,000, with a deduction of $3,600 at 20%.

The total CCA for Year 2 is $31,048. This increase reflects how deductions grow after the half-year rule's initial limitation, offering more substantial tax savings as the property stabilizes and generates steady income.

How Property Improvements Affect CCA

Significant property upgrades are added to the relevant class's UCC and depreciated over time. For example, if you install a $30,000 solar panel system in Year 3, it would qualify under Class 43 with a 30% rate. Due to the half-year rule, only 15% of the cost ($4,500) could be claimed in the first year of the improvement.

Smaller upgrades, however, may be expensed immediately. Larger enhancements, such as a $25,000 paved driveway, are capitalized and assigned to Class 6 (10% annual rate) for depreciation.

As Landlii explains:

"Putting a furnace in Class 1 at 4% would significantly understate your deduction." [1]

These examples highlight the importance of correctly categorizing assets and improvements to maximize your CCA claims.

Tax Benefits of Depreciation for Multi-Unit Rentals in Nova Scotia

Claiming the Capital Cost Allowance (CCA) doesn’t just reduce your taxes - it also boosts your cash flow without requiring any cash out of pocket. Since CCA is a non-cash deduction, it lowers your taxable income while keeping more cash in your hands for reinvestment [3][2]. For example, if a fourplex generates $48,000 in annual rental income and qualifies for $16,800 in first-year CCA, you could save about $6,700 in taxes, assuming a 40% marginal tax rate. That’s money you can put toward reinvestments or paying down debt.

These tax benefits directly improve your property’s cash flow. Essentially, CCA allows your building to act as a tax shelter, creating liquidity while your property value continues to rise. Over time, the savings grow even more, especially after the half-year rule no longer restricts your deductions.

The benefits become even more pronounced when paired with financing through CMHC’s MLI Select program. With 95% loan-to-value financing, your upfront equity investment on a $640,000 fourplex could be as low as $30,000–$40,000. As Ben Kinden of Kinden CPA explains:

"The claimed amount could then be used as an investment in some other security. You end up making more money from these amounts, which offsets any potential recapture you could incur" [3].

Another advantage is flexibility. You can decide when to claim CCA. If you’re in a low-income year or already facing a rental loss, you can skip the deduction and preserve your Undepreciated Capital Cost (UCC) for future years when the tax savings would have a bigger impact [1][3].

Filing Requirements and Provincial Considerations in Nova Scotia

To claim Capital Cost Allowance (CCA) on your rental property, you’ll need to file Form T776 (Statement of Real Estate Rentals) with the Canada Revenue Agency. The annual CCA amount should be reported on Line 9936 of this form. This applies whether you own a fourplex in Halifax or a sixplex in Cape Breton.

One key step for property owners in Nova Scotia is separating the purchase price into land and building values. Only the building portion qualifies for depreciation. To do this, you can rely on the local municipal property assessment ratio or opt for a professional appraisal. For example, if the Halifax Regional Municipality assesses a property as 70% building and 30% land, you would use that ratio to allocate your total capital cost before calculating your CCA.

If you’re developing new multi-unit rentals, you might qualify for HST rebates in Nova Scotia. These rebates lower your overall capital cost, which, in turn, reduces your CCA base. Additionally, land transfer taxes paid during the purchase aren’t deductible as current expenses. Instead, they’re added to your property’s capital cost, increasing your Undepreciated Capital Cost (UCC). This higher UCC allows for greater CCA claims over time [5]. These adjustments not only impact your capital base but also tie into your broader tax planning efforts.

It’s essential to keep thorough records of expenses like land transfer taxes, pre-rebate HST, and site development costs. These directly affect your UCC and your ability to claim future CCA deductions.

Nova Scotia also provides the Capital Investment Tax Credit (NS CITC), a refundable corporate tax credit equal to 25% of the capital cost of eligible property [6]. However, for federal tax purposes, this credit reduces your capital cost before you calculate CCA [6]. This adjustment further fine-tunes your CCA calculations and boosts your overall tax benefits.

Understanding these provincial details and incorporating them into your CCA strategy can improve your long-term tax efficiency and investment returns.

What This Means for Your Property Investment

Understanding how Capital Cost Allowance (CCA) works is a game-changer for managing long-term tax strategies and keeping more cash in your pocket. The way you handle CCA today will ripple through your net income for years, directly impacting your cash flow and return on investment (ROI).

Timing matters, especially in Nova Scotia. CCA isn’t mandatory - you can choose to skip or reduce claims during low-income years and save the deductions for when you’re in a higher tax bracket. As Ben Kinden from Kinden CPA explains:

"The claimed amount [from CCA] could then be used as an investment in some other security. You end up making more money from these amounts, which offsets any potential recapture you could incur" [3].

This flexibility opens the door to smarter strategies, such as asset segregation.

Asset segregation offers better tax efficiency. Instead of applying a flat 4% depreciation rate to the entire building, you can separate components like heat pumps and HVAC systems (Class 43 at 30%) or appliances (Class 8 at 20%). This approach accelerates your deductions, boosting cash flow in the early years when you might need it the most.

On top of these tax benefits, structuring your capital effectively can further improve returns. For example, if you're building with plans to refinance, new construction adds forced equity. Once the property is tenanted, you can refinance based on its appraised value - typically using a 5% cap rate - to recover your initial investment and HST rebates. This "build-refinance-repeat" cycle not only grows your portfolio faster but also allows CCA to reduce your taxable income along the way.

Keep meticulous records. Track every dollar spent on capital costs, including land transfer taxes, pre-rebate HST, and site development expenses. These costs increase your Undepreciated Capital Cost (UCC), giving you more room for CCA claims over time. Additionally, the $1,500 safe harbour rule allows you to treat smaller improvements as operating expenses rather than capital costs [1]. This simplifies bookkeeping and maximizes your current-year deductions while aligning with your broader tax strategy.

FAQs

Should I claim CCA if I might sell in a few years?

Claiming Capital Cost Allowance (CCA) can lower your taxable rental income, giving you upfront tax savings. However, when you sell the property, any CCA you've claimed may be taxed as "recapture", turning into a liability.

If you're planning to sell in the near future, skipping the CCA might help you avoid these recapture taxes. On the other hand, if you intend to hold the property for the long term, claiming CCA could boost your cash flow in the interim. It's crucial to evaluate your ownership timeline and consult a tax professional to ensure your approach aligns with your financial goals.

How do I split my new-build cost between land and building?

To calculate depreciation costs in Canada, you’ll need to separate the land value (which doesn’t depreciate) from the building value (which does). Start by referencing your purchase agreement or an appraisal to identify the land’s value. Subtract this amount from the total purchase price to determine the building’s value. This building value is what you can use to claim Capital Cost Allowance (CCA) at the appropriate rate. Remember, land cannot be depreciated.

Which items in a new fourplex can use faster CCA rates than 4%?

If you construct a new fourplex between April 16, 2024, and December 31, 2030, you can take advantage of an accelerated 10% Capital Cost Allowance (CCA) rate. This is a significant bump from the usual 4% rate, allowing you to depreciate the property faster and enjoy greater tax savings during that timeframe.