How Canadian Professionals Are Building Rental Portfolios on the Side

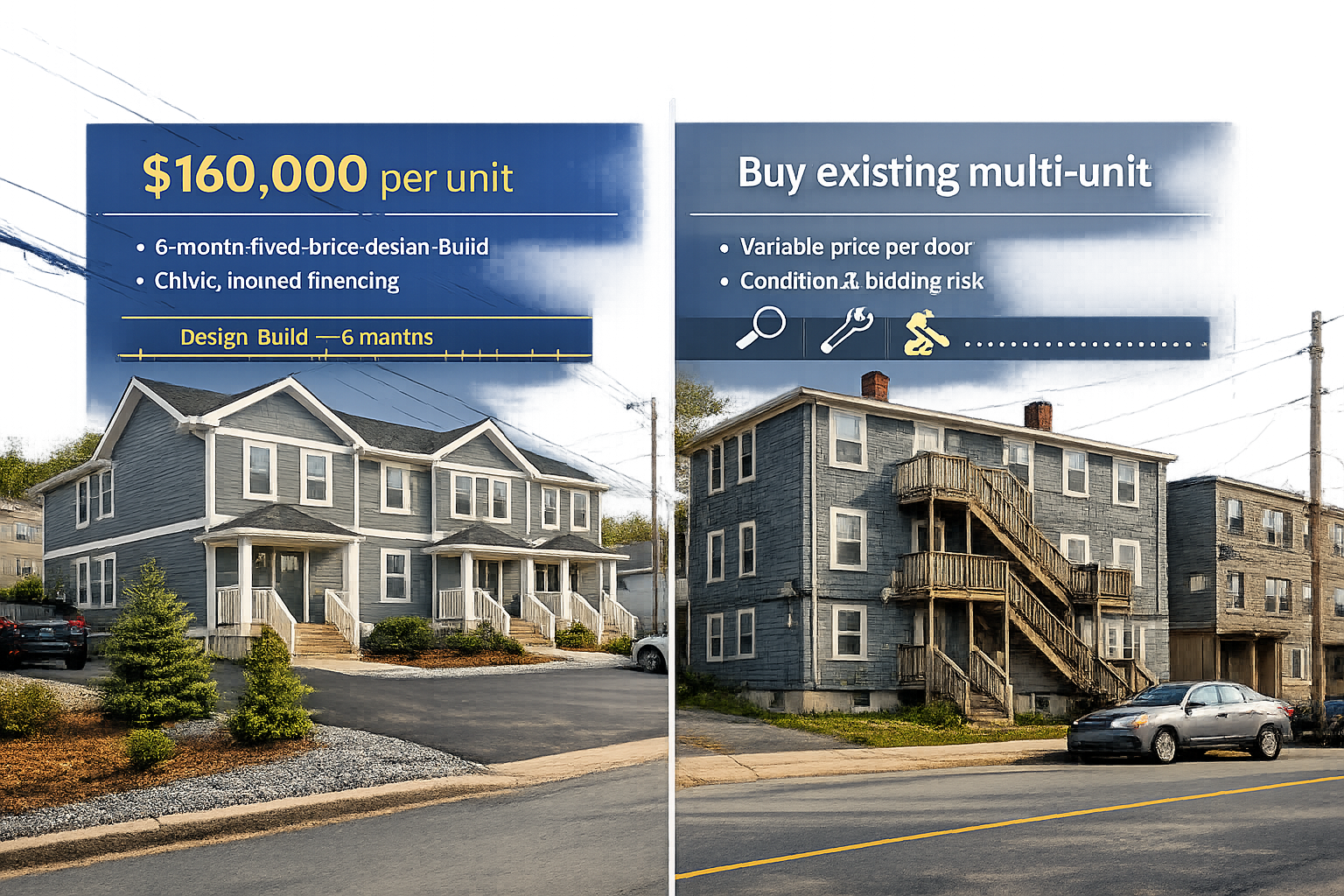

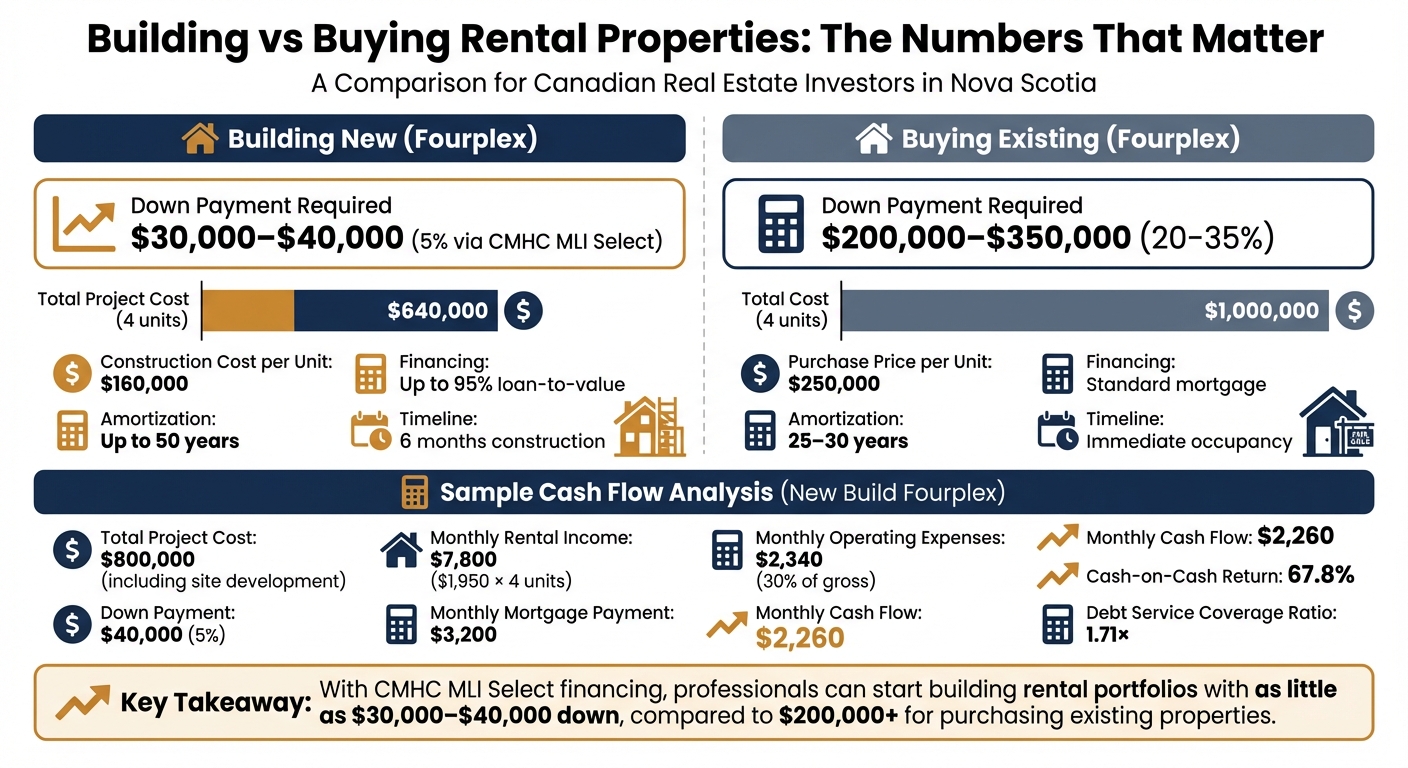

If you’re a professional in Nova Scotia wondering whether building rental properties is worth your time and money, here’s the answer: constructing a fourplex costs about $160,000 per unit or $640,000 total. Compare that to buying an older building in the same market, where units average $250,000 each. On top of that, CMHC’s MLI Select program lets you finance up to 95% of the cost, meaning you could start with as little as $30,000–$40,000 down. This article will walk you through what it takes to build purpose-built rentals, from zoning to financing, and whether it’s the right move for you.

Building vs Buying Rental Properties in Nova Scotia: Cost and Financing Comparison

Windsor Rental Property Build Cost 2025 | Passive Income & Wealth Blueprint

sbb-itb-16b8a48

Is Multi-Unit Building Right for You?

Rental construction works best for professionals with steady income, access to capital, and limited time to oversee construction projects. Using a design-build approach simplifies the process by managing everything under one roof - no juggling multiple contractors - allowing you to develop rental units without stepping away from your career.

"As a first-time investor, having one team handle everything from design to occupancy made the difference between moving forward and remaining stuck." [1]

Who Builds Rental Properties Part-Time

If you're a busy professional, the design-build model offers a streamlined way to invest in rental properties. Instead of coordinating architects, engineers, and contractors, you work with one integrated team. You don’t need prior construction experience to succeed - what matters is your ability to review budgets, communicate effectively with tenants, and make informed decisions about zoning and financing. To help you decide if you're ready, consider the checklist below.

Self-Assessment Checklist

Ask yourself the following before diving into a multi-unit build:

- Can you meet a 5%–20% down payment requirement?

- Do you have a steady income to qualify for financing?

- Are you prepared to manage tenant relationships, whether directly or through a property manager?

- Are you comfortable with a six-month construction timeline?

- Is your chosen property aligned with local zoning rules?

Once you’ve confirmed your personal readiness, the next step is ensuring your property meets zoning and servicing requirements.

Nova Scotia Zoning and Property Requirements

Choosing the right property is critical. In Halifax, for example, building a fourplex typically requires R-2 or R-3 zoning, a lot size of at least 8,000 square feet, and 80 feet of frontage. Municipal water and sewer connections are a must - well and septic systems usually can’t handle the demands of multi-unit buildings.

To avoid costly surprises, verify zoning compliance early. Halifax's ExploreHRM interactive mapping tool can help you check setbacks and overlay restrictions. Expect to budget $35,000–$80,000 for site preparation, which includes clearing, grading, soil testing, and utility hookups. Ignoring zoning requirements can lead to reduced unit counts, cutting into your potential equity before construction even starts. [1]

Financing Your Multi-Unit Build

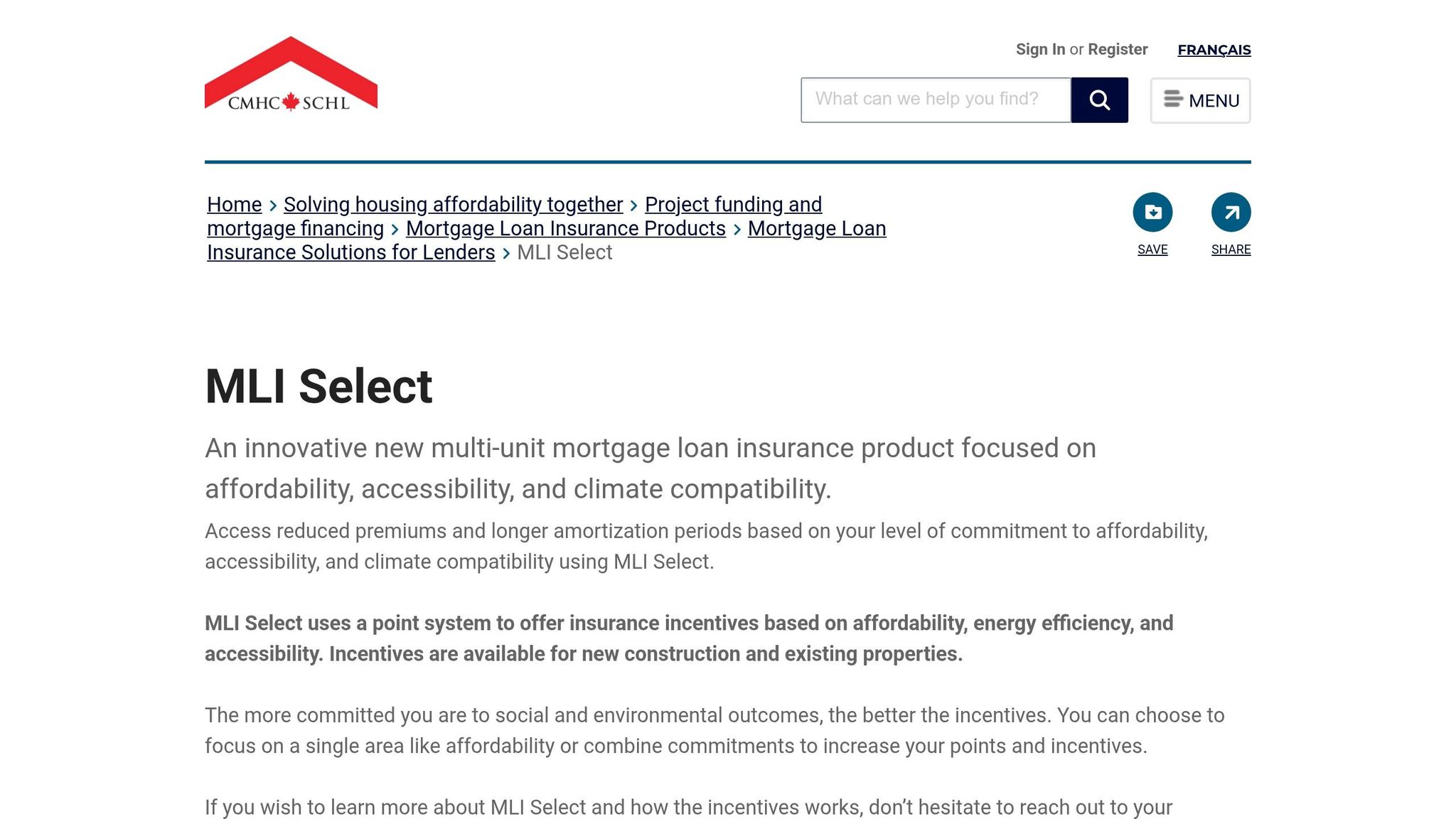

The CMHC MLI Select program has lowered the financial barrier for first-time rental builders in Canada. Instead of the typical 20–35% down payment required for conventional construction loans, eligible projects can secure financing with as little as 5% equity. This comes with extended amortization periods of up to 50 years and debt service coverage ratios as low as 1.10×. For example, a $960,000 sixplex in Nova Scotia would need only about $48,000 down instead of $192,000 - a massive difference that makes rental construction more achievable for professionals who might otherwise spend years saving. This program allows individuals to start building rental portfolios without the burden of excessive upfront capital.

CMHC MLI Select: Low Down Payment Financing

CMHC MLI Select offers financing terms that include up to 95% loan-to-value, 50-year amortizations, and reduced insurance premiums for developments with at least five self-contained units. Projects are assessed on a points-based system across three key areas: affordability, energy efficiency, and accessibility. Higher scores in these categories unlock better loan terms. To qualify for the best benefits, you’ll generally need 60–80% of your units priced at or below 30% of the median renter income for your area, energy-efficient building designs, and accessibility features such as barrier-free units or wider entryways.

To access this program, borrowers must meet specific financial requirements: a net worth of at least 25% of the project cost and liquid funds to cover a 5–10% deposit plus a 10% contingency reserve. For a $1,200,000 turnkey fourplex, this means demonstrating a net worth of $300,000 and having approximately $180,000 in accessible capital, including the down payment. Helio’s designs are already pre-qualified for MLI Select, simplifying the underwriting process and ensuring your project meets the necessary points to secure favourable terms. Keep in mind that the application-to-funding process typically spans 4–6 months, so plan carefully when aligning your land purchase and construction start dates. The next sections will dive into how MLI Select compares to traditional financing and share practical tips for saving your down payment.

Financing: Building vs Buying Existing Properties

Financing a new build differs significantly from purchasing an existing property. Loans for existing properties depend on current rent rolls, while new construction financing uses pro forma rents, often resulting in better terms. With MLI Select financing, underwriting is based on stabilized rents rather than potentially lower in-place income. For instance, a $1,200,000 fourplex financed at 85% loan-to-value (LTV) with a 4.75% interest rate and 40-year amortization would result in monthly mortgage payments of approximately $4,900–$5,100. Assuming market rents of $2,000 per unit and monthly operating expenses of $1,600, the net operating income of $6,400 leaves $1,300–$1,500 in monthly cash flow before reserves. This equates to a debt service coverage ratio well above 1.20.

On the other hand, purchasing existing properties typically requires a 20–35% down payment, shorter amortization periods (25–30 years), and qualification based on current rent rolls. While buying an existing property provides immediate rental income and avoids construction risks, it often comes with older systems, higher capital expenditure needs, and limited financing leverage. New builds, despite the 12–18 month ramp-up period without rental income, often deliver stronger cash-on-cash returns thanks to extended amortization and lower operating costs. In the next section, we’ll explore strategies to build your down payment effectively.

How to Save for Your Down Payment

Even with low down payment programs, saving strategically is essential. Start by setting a clear savings target. For instance, to accumulate $150,000 in three years, you’d need to save about $4,200 per month from your salary, bonuses, and side income. Max out your TFSA contributions and invest in low-cost ETFs to grow your funds tax-free. Avoid tapping into RRSPs for rental investments since the Home Buyers’ Plan is limited to owner-occupied properties, and withdrawing RRSP funds for rentals triggers a taxable event that reduces your capital.

Another strategy is using a HELOC secured against your primary residence to bolster your down payment. Interest on funds used for rental income is typically tax-deductible, allowing you to use this capital as part of your equity injection without selling off other investments. Alternatively, consider purchasing an income-generating duplex, holding it for 2–3 years, and refinancing to access $80,000–$150,000 in equity for your next project. This approach spreads risk, provides valuable experience, and helps you transition into larger developments without needing to save the entire down payment in cash from your salary alone.

Fixed-Price Design-Build for Busy Professionals

For those juggling demanding schedules, the fixed-price design-build model offers a straightforward way to minimize oversight and financial uncertainty. Traditional construction, often based on a cost-plus structure, requires you to cover actual expenses plus a contractor fee. This approach exposes you to fluctuating material costs, labour shortages, and unexpected change orders. It also demands constant involvement and creates financial unpredictability, which can make lenders hesitant.

Fixed-Price vs Cost-Plus Construction

With fixed-price construction, your total cost is locked in at the start, shifting the risk of budget overruns to the contractor. If material prices rise or subcontractors back out, it's the builder's responsibility to handle it - not yours. In contrast, cost-plus construction passes every surprise expense directly to you. This makes it harder to secure financing and predict your final return on investment. In volatile markets, cost-plus projects can exceed initial estimates by 20–30%, potentially turning a projected 12% return into a break-even situation. For part-time investors, fixed-price contracts eliminate the need to track invoices, approve changes, or renegotiate with trades during the project.

| Criteria | Fixed-Price Contracts | Cost-Plus Contracts |

|---|---|---|

| Budget Predictability | Pricing locked in upfront | Costs unknown until completion |

| Owner Involvement | Minimal – contractor handles decisions | High – frequent approvals needed |

| Risk Allocation | Contractor bears cost overruns | Owner assumes all cost risks |

| Financing | Fixed costs attract lenders | Open budgets deter lenders |

| Timeline | Often tied to penalties for delays | Changes often slow progress |

This approach is at the core of Helio Urban Development's streamlined process.

How Helio Urban Development Works

Helio Urban Development integrates architecture, structural engineering, construction, and project management into a single company under one contract. This eliminates the coordination issues that often cause delays and budget overruns in traditional builds. Helio fixes the per-unit cost at $160,000 - 10% lower than CMHC benchmarks - and imposes a $1,000 daily penalty for delays beyond six months. All designs are pre-approved for CMHC MLI Select, ensuring lenders can confidently underwrite the project before construction begins.

"The fixed pricing model let me lock in my financing with confidence. My lender was impressed that every line item was guaranteed before we broke ground." [1]

What this means for property owners: You sign one contract, pay one price, and work with one team from zoning feasibility to final completion. This single-contract model eliminates disputes between trades and unexpected charges, giving you peace of mind.

The Design-Build Process: Zoning to Tenant-Ready

Helio’s design-build process is built around fixed-price contracts to ensure a seamless path from planning to occupancy. It starts with a detailed site analysis to confirm zoning setbacks and unit capacity before contracts are signed. This step avoids costly design errors that could reduce the number of units you can build. Once zoning is confirmed, Helio’s integrated team manages everything: architectural plans, engineering, permits, construction, and final inspections - all within a six-month timeline. Prefabrication and fixed bids further cut down project durations, which traditional builds often stretch to 12–18 months.

"As a first-time investor, having one team handle everything from design to occupancy was the difference between moving forward and staying stuck in analysis paralysis." [1]

With a perfect on-time delivery record and over 40 units currently under construction across Nova Scotia - including projects on Arthur Street in Truro, Chadwick Street in Dartmouth, and Richard Street in Kentville - this model aligns with Nova Scotia's growing rental demand and helps you start generating cash flow faster.

Calculating Returns: Cash Flow, Cash-on-Cash Return, and Portfolio Growth

Once you’ve secured fixed pricing and financing, it’s time to evaluate your returns. For part-time investors focused on building rental portfolios, three metrics are especially important: monthly cash flow, cash-on-cash return (a specific type of ROI), and the debt service coverage ratio (DSCR). These numbers give you a clear picture of your immediate income potential and the scalability of your portfolio. Let’s break this down using a practical example of a fourplex project in Nova Scotia.

Sample Pro Forma for a Nova Scotia Fourplex

Take a fourplex built at Helio’s fixed pricing of $160,000 per unit, bringing the construction cost to $640,000. Adding site development and soft costs, the total project cost lands at approximately $800,000. With a 5% down payment of $40,000, the remaining $760,000 is financed over 50 years, resulting in monthly mortgage payments of about $3,200.

At an average market rent of $1,950 per unit, the fourplex generates $7,800 in monthly rental income, or $93,600 annually. Operating expenses - covering property taxes, insurance, maintenance, and property management - consume roughly 30% of the gross income, which works out to about $28,080 per year. This leaves a net operating income (NOI) of approximately $65,520. After subtracting annual mortgage payments of $38,400, your net cash flow is around $27,120 per year, or $2,260 per month.

This means your $40,000 down payment yields an annual cash flow of $27,120, translating to a 67.8% cash-on-cash return. That’s a strong outcome compared to more traditional investments.

Key Metrics: Cash-on-Cash Return, DSCR, and Building Equity

Another vital metric is the DSCR, which measures your ability to cover debt obligations with your NOI. Traditional lenders often look for a DSCR of at least 1.25×, but CMHC’s MLI Select program may accept ratios as low as 1.1×. In this example, dividing the NOI of $65,520 by the annual mortgage payments of $38,400 gives a DSCR of roughly 1.71×. This provides a solid buffer if rental income drops or expenses rise unexpectedly.

Equity growth is another benefit to consider. As you pay down the mortgage and the property appreciates, your equity increases. Even modest appreciation, combined with a shrinking loan balance, can significantly boost your wealth over time. These metrics not only highlight strong initial returns but also lay the groundwork for scaling your portfolio.

Growing Your Portfolio

Once your first property stabilizes and delivers consistent cash flow, many investors explore ways to grow their portfolio. After about 24 months, you can refinance to access the equity built through mortgage paydown and property appreciation. This approach, often referred to as the BRRRR method (Buy, Renovate, Rent, Refinance, Repeat), allows you to fund new projects while keeping your primary career largely undisturbed. It’s a practical way to scale your investments without overextending yourself.

Getting Started with Your First Rental Property

Before diving into your first rental property project, take a close look at your finances. To qualify for CMHC MLI Select financing, you'll need a credit score of at least 680, liquid funds for a 5–10% down payment, and an additional 10% set aside for contingencies. On top of that, your net worth should equal at least 25% of the project cost. For example, if you're planning to build a $1,000,000 fourplex, you'd need $50,000–$100,000 for the down payment, $100,000 in reserves, and a net worth of at least $250,000 to meet these requirements [2].

Next, find the right lot for your project. Look for vacant land zoned R-2 or R-3 in municipalities across Nova Scotia. These zoning categories usually allow for duplexes, triplexes, and fourplexes. Focus on areas close to major employers like hospitals or universities, as these locations tend to attract reliable tenants. Before committing to a site, check the zoning regulations on municipal websites to avoid unexpected hurdles. Additionally, complete a Phase 1 environmental assessment (roughly $2,000) and a geotechnical report to ensure the land can handle multi-unit construction.

Once you've secured a lot, it's time to arrange financing. Apply for CMHC MLI Select through lenders such as BMO, providing detailed pro formas to demonstrate a debt service coverage ratio of at least 1.10. With an annual income of about $150,000, you could qualify for projects worth up to $1,500,000 with a $75,000 down payment [3]. CMHC's program offers up to 95% loan-to-cost financing and 50-year amortisation, making it easier for professionals to fund multi-unit developments while managing other commitments.

After financing is in place, the next step is choosing the right construction partner. Opt for a fixed-price design-build firm, such as Helio Urban Development, to simplify the process. Start with a free lot feasibility analysis, which will confirm zoning, soil conditions, and overall project viability. Signing a fixed-price contract - at a rate of $160,000 per unit - ensures your costs are locked in, and your involvement is limited to quarterly updates. This approach allows you to stay focused on your primary career while your project progresses smoothly.

Breaking into rental property development requires careful financial planning, smart site selection, and a reliable construction partner. With CMHC MLI Select financing and a straightforward fixed-price build model, professionals in Canada can develop multi-unit rentals without stepping away from their day jobs. By following these steps, you can set yourself up for success in the rental property market.

FAQs

What are the biggest risks when building a small multi-unit rental?

Building rental properties comes with a set of risks that need careful attention. One of the biggest concerns is meeting building codes and safety regulations, especially when it comes to fire separations and overall safety measures. Falling short here can result in hefty fines or expensive rework, both of which eat into your margins.

Other hurdles include construction delays, unexpected cost overruns, and the often-complicated process of navigating zoning laws and securing permits. Once the property is up and running, there are ongoing challenges like managing tenants, keeping units occupied, and dealing with market shifts that can affect your returns.

To stay ahead of these issues, thorough planning is key. An integrated design-build approach - where all aspects of the project are coordinated from the start - can help minimize delays, control costs, and ensure compliance with regulations. This proactive strategy can make a big difference in keeping your project on track and profitable.

How can I determine if my lot is suitable for a fourplex?

To determine if your lot in Nova Scotia can accommodate a fourplex, start by reviewing the local zoning bylaws to ensure multi-unit residential buildings are permitted. Next, check if your lot meets the minimum size and setback requirements, as these differ between municipalities. Finally, you'll need to obtain the necessary permits from local authorities to confirm the project aligns with building codes and land-use regulations. Reaching out to municipal planning offices can provide clarity and help confirm these details.

When does a new build typically start cash flowing?

When undertaking a new build, cash flow typically begins once construction wraps up and the units are rented out. This entire process usually spans 12 to 18 months from the project's initiation. The timeline can vary based on factors like permitting, unexpected delays, and the level of demand in the rental market.