How Tax Credits Impact Rental Construction ROI in Nova Scotia

Building rentals in Nova Scotia isn’t cheap, especially when construction costs hit $200–$250 per square foot. But what if I told you tax credits and incentives could shave off $50+ per square foot? That’s real money - on a 4,000-square-foot fourplex, you’re looking at $200,000 in savings. These programs aren’t just about cutting costs; they can also boost your ROI by 2–4 percentage points. This article breaks down the key tax credits, timelines, and eligibility rules you need to know to make your project pencil out.

Nova Scotia Rental Construction ROI: With vs Without Tax Incentives

Tax Incentives for Rental Construction in Nova Scotia

If you're a property owner in Nova Scotia planning to build multi-unit rentals, there are financial incentives available at the federal, provincial, and municipal levels. These programs can often be combined, helping to stretch your budget and improve returns.

Federal vs. Provincial Incentives

Federal programs, like the CMHC Rental Construction Financing Initiative (RCFi), aim to lower financing costs. They offer below-market interest rates and longer amortization periods, making it easier to manage debt. Another federal option, CMHC MLI Select, provides even better terms than standard financing, especially for projects that meet specific criteria like energy efficiency or affordability.

On the provincial side, Nova Scotia's programs focus on cutting direct costs. These include property tax reductions, subsidies for affordable housing units, and fee waivers tied to the province’s regulations. While federal programs primarily reduce borrowing costs, provincial incentives lower upfront expenses, combining to improve your return on investment (ROI). Understanding these distinctions is crucial to navigating the application process and maximizing benefits.

Eligibility Requirements and Application Deadlines

Each program comes with its own rules and timelines, so paying attention to details is critical. Federal programs typically require at least four units to qualify as multi-unit housing, along with commitments to affordability - such as offering a percentage of units at below-market rents - and long-term rental agreements, often for 20+ years under initiatives like RCFi.

Provincial programs in Nova Scotia may prioritize projects that include affordable housing or energy efficiency upgrades, aligning with local housing goals. Deadlines vary by program. For instance, the federal HST rebate for purpose-built rentals must be claimed within two years of renting the first unit, while energy efficiency rebates often require pre-approval before construction begins. Staying on top of these timelines can make or break your eligibility.

How Incentives Reduce Project Costs and Improve Financing

These incentives directly lower project costs, improving your ROI and making financing more accessible. Programs like tax credits, fee waivers, and property tax reductions cut upfront expenses, reducing the equity you need to invest. This also improves your loan-to-value ratio, which can qualify you for better interest rates and lending terms.

Take a practical example: a fourplex in Nova Scotia costing C$640,000 could benefit from a C$96,000 HST rebate. Add energy efficiency incentives of C$52 per square metre, and the effective project cost drops significantly. These savings improve debt coverage ratios, making it easier to secure lower lending rates. The result? Shorter payback periods, stronger cash flow, and an ROI boost of 2–4 percentage points. Small adjustments like these can make a big difference in the financial performance of your rental project.

sbb-itb-16b8a48

CMHC Rental Construction Financing Initiative (RCFi)

The CMHC Rental Construction Financing Initiative (RCFi) is a federal program designed to make rental property development more financially accessible. By reducing upfront equity requirements and improving cash flow, RCFi reshapes the economics of multi-unit projects, particularly in Nova Scotia. This program deserves a closer look for its ability to change how developers approach financing.

RCFi Program Features

RCFi operates on a points-based system that evaluates affordability, energy efficiency, and accessibility. The higher your score - 50, 70, or over 100 points - the better the financing terms you can secure. At the top tier, developers can access up to 95% loan-to-cost (LTC) for new construction. For example, a C$640,000 fourplex might only require a down payment of C$32,000 under RCFi, compared to the C$128,000 to C$160,000 typically needed with conventional financing.

The program also extends amortization periods up to 50 years, significantly lowering monthly payments and improving cash flow. With a minimum debt coverage ratio (DCR) of 1.10 and insured five-year fixed rates around 4.00% - compared to the 5.00% common in traditional financing - RCFi offers more favourable terms. For projects scoring over 100 points, CMHC even provides limited-recourse options, reducing personal liability for developers.

These features - lower equity requirements, longer amortization, and reduced interest rates - create a financing structure that frees up capital and improves cash flow for multi-unit developments.

ROI Example Using RCFi Financing

The advantages of RCFi financing become clear when looking at the numbers. Consider an eight-unit building in Halifax valued at C$2.62 million. With RCFi terms, including a 5% down payment, a 50-year amortization, and a 4% interest rate, your initial equity investment could be as low as C$20,000 once you factor in rental income during construction.

- Year 0: Annual cash flow could start at approximately C$15,882 positive.

- Year 5: Assuming a 3% annual rent increase, the property value might rise to C$3.24 million, equity could grow to C$730,000, and cumulative cash flow might total C$169,000.

- Year 10: The property could appreciate to C$4.01 million, with equity reaching C$1.61 million and cumulative cash flow hitting C$459,000.

This approach leverages "financing arbitrage" by combining high leverage and extended amortization to minimize upfront equity while maximizing cash flow. By contrast, conventional financing for the same project might require a 20% down payment (around C$524,000) and result in negative cash flow of roughly C$9,786 annually. RCFi can turn a project that would typically lose money into a cash-flow-positive investment from day one.

Moving from RCFi to Conventional Financing

RCFi's benefits are front-loaded, but transitioning to conventional financing later changes the financial picture. The program usually requires a 20-year commitment to below-market rents. Once this term ends - or if you exit earlier - you'll need to refinance with conventional terms, which generally involve a 20–25% equity requirement and a shorter amortization period of 25–30 years.

For the eight-unit example, this shift could turn annual cash flow from +C$15,882 under RCFi to approximately –C$9,786 with conventional financing. That’s a swing of about C$25,668 per year, underscoring the importance of planning your long-term financing strategy.

Provincial and Municipal Tax Benefits in Nova Scotia

Beyond federal programs like RCFi, Nova Scotia offers provincial and municipal incentives that help lower costs and speed up timelines for multi-unit rental projects. These measures aim to reduce upfront expenses, improve cash flow, and make projects more financially viable.

Property Tax Reductions and Direct Subsidies

Nova Scotia's Build Nova Scotia program provides substantial property tax abatements for affordable housing projects. Developers can receive up to a 100% reduction in municipal property taxes for the first 10 years if at least 20% of the units are designated as affordable. For instance, a 20-unit building valued at C$5 million in Halifax could save between C$100,000 and C$150,000 annually, based on property tax rates of 2–3% [1]. Eligibility requires provincial approval and adherence to affordability agreements.

The Affordable Housing Development Program (AHDP) offers direct subsidies of up to C$50,000 per affordable unit, with a maximum funding cap of C$10 million per project. For example, one Halifax-based fourplex secured a C$200,000 subsidy, cutting construction costs by about 15% [2].

In Halifax Regional Municipality (HRM), the Rental Housing Incentive Program provides a 75% property tax abatement for 15 years on new builds where at least 50% of the units are affordable. For a property assessed at C$10 million with a 1.5% tax rate, this translates to annual savings of approximately C$75,000 [4]. Additionally, HRM’s Multi-Year Tax Incentive Program offers phased tax reductions - 50% for the first three years and 25% for years four and five - for projects with 10 or more rental units. A C$4 million project could see total savings of over C$300,000 through this program [3].

These combined tax breaks and subsidies significantly improve project ROI by cutting both upfront and ongoing costs.

Energy Efficiency Rebates

Energy efficiency programs in Nova Scotia add another layer of cost savings. Efficiency Nova Scotia's Green Building Incentive provides up to C$5,000 per unit for ENERGY STAR–certified rentals, plus an additional C$20,000 for net-zero designs. For example, a 30-unit project could receive rebates exceeding C$200,000, reducing construction costs by roughly 10% [5].

The Home Efficiency Rebate Plus (HER+) program offers rebates of C$0.25 per kWh saved annually, up to C$15,000 per building. One fourplex project received a rebate of C$40,000 upfront, along with annual savings of C$2,500, which increased its net ROI from 7.2% to 9.1% over a 10-year period [6]. The Canada Green Building Council has suggested combining these rebates with AHDP subsidies. In one Dartmouth project, this approach reduced overall costs by 20–25% and shortened the payback period from 12 years to 8 [7]. These examples highlight how energy-efficient construction can align financial and environmental goals.

Fee Waivers and Faster Permitting

Municipal programs also contribute to better project economics. In Halifax and Cape Breton, development fee waivers of up to C$50,000 are available for affordable rental projects, typically those with 50 or more units. These waivers eliminate impact fees and speed up permitting by 30–60 days, cutting soft costs by an estimated 2–5%. For example, a 2025 HRM project avoided C$75,000 in fees and began construction 45 days earlier. HRM’s Fast-Track Permitting for Multi-Unit Rentals further reduces review times from 120 to 60 days, saving C$20,000–C$40,000 in holding costs [8][9].

Other initiatives, like the Town of Yarmouth's Development Rebate Program, phase in increased taxable assessed values over up to 10 years. This approach lowers the tax burden during a project’s early years. For example, one investor reported total cost savings of 15–30%, with combined incentives totalling C$500,000 on a C$3 million project. To maximize benefits, rental property investors should confirm eligibility via the NS Housing portal, coordinate with municipal and provincial bodies, and consider hiring a consultant to navigate stacking multiple incentives effectively.

Tax Deductions During Operations

Tax credits can trim construction costs, but operational tax deductions are where rental properties can really improve cash flow. Once your property starts generating income, these deductions allow you to offset expenses against your rental revenue, reducing taxable income and keeping more money in your pocket. Unlike construction costs, which are spread out over time through depreciation, operational expenses can be deducted in the same year they occur. This makes managing your property more tax-efficient and increases your annual return.

Common Deductible Expenses

If you own rental properties in Nova Scotia, you can deduct a variety of operational expenses. The most significant is mortgage interest - but note, this applies only to the interest portion of your payments, not the principal. Let’s break this down with an example:

For a fourplex generating C$120,000 in annual gross rent, you might deduct C$40,000 in mortgage interest, C$12,000 in property taxes, C$15,000 in maintenance, and C$8,000 in insurance and management fees. That totals C$75,000 in deductions, leaving C$45,000 in taxable income. At a combined federal-provincial tax rate of 29%, you’d owe C$13,050 in taxes, leaving you with C$31,950 in net cash flow. That’s a 27% improvement compared to paying taxes on the full rental income.

Other deductible expenses include utilities (if you pay them), property management fees, advertising, and professional services like accounting or legal advice. You can also claim depreciation, known as Capital Cost Allowance (CCA), on the building at 4% annually on a declining balance. Many owners hold off on claiming CCA to retain favourable capital gains treatment when selling. On average, every deductible dollar saves you between C$0.29 and C$0.48 in taxes, giving a noticeable boost to your yearly returns.

Construction vs. Operational Tax Treatment

The way expenses are treated for tax purposes changes significantly once you move from construction to operations. During construction, costs like materials, labour, and design fees are capitalized - they’re added to your property’s cost base rather than deducted immediately. These costs are then depreciated over time through CCA once the property is complete.

In contrast, operational expenses - like repairs, property taxes, and interest - are fully deductible in the year they’re incurred, offering immediate tax benefits. However, distinguishing between repairs and improvements is crucial. For instance, replacing a roof for C$50,000 during operations is deductible because it restores the property’s function. If that same roof is installed during construction, it’s capitalized as part of the building’s cost. Always keep detailed records, including contractor invoices and bank statements, as the Canada Revenue Agency (CRA) can audit these expenses for up to six years.

GST/HST Rules for Long-Term Rentals

In Nova Scotia, long-term residential rentals (those over 30 days) are exempt from GST/HST. This means you don’t charge your tenants the 15% tax on rent. However, it also means you can’t claim Input Tax Credits (ITCs) on related expenses like maintenance, utilities, or insurance. For example, if you spend C$10,000 on exempt repairs, you lose out on C$1,500 in potential ITCs.

For new construction, eligible rental properties can receive a 100% GST/HST rebate on construction costs, as discussed earlier in the RCFi financing section. You can choose to register for GST/HST to claim ITCs, but charging tenants an additional 15% might make your units less competitive. If your property has commercial elements, like coin laundry services, where GST/HST does apply, you’ll need to track exempt and taxable portions separately. Most multi-unit rental owners in Nova Scotia stick with exempt status to keep rents affordable while maximizing the construction-phase rebate.

How to Calculate ROI with Tax Credits

Figuring out how tax credits impact your returns means diving into the numbers. By factoring in various tax credits, you can clearly see how they enhance your project's profitability. The basic ROI formula - annual net operating income divided by total project cost - improves significantly when tax savings are included. Think of tax credits as a way to lower your effective project cost. For instance, if you're building a fourplex in Halifax for C$1,500,000 and qualify for C$200,000 in combined tax incentives, your effective cost drops to C$1,300,000. This adjustment alone can increase your ROI by about 15% compared to the standard calculation.

ROI Calculation Steps

- Estimate Total Project Cost: Include land purchase, construction, permits, and professional fees.

- Identify Tax Credits: Subtract the total value of tax credits from your project cost to determine your effective investment.

- Incorporate Financing Terms: If you're using programs like CMHC RCFi, account for reduced mortgage rates (1–2% below conventional rates).

- Project Annual Net Operating Income: Subtract operating expenses - like property taxes, maintenance, insurance, and management fees - from your gross rental income.

- Calculate ROI: Divide your annual net operating income by your effective project cost and multiply by 100. Each dollar of tax credit reduces your investment, meaning the same income produces a higher return.

This step-by-step approach lays the groundwork for evaluating specific examples.

Fourplex ROI Example with Incentives

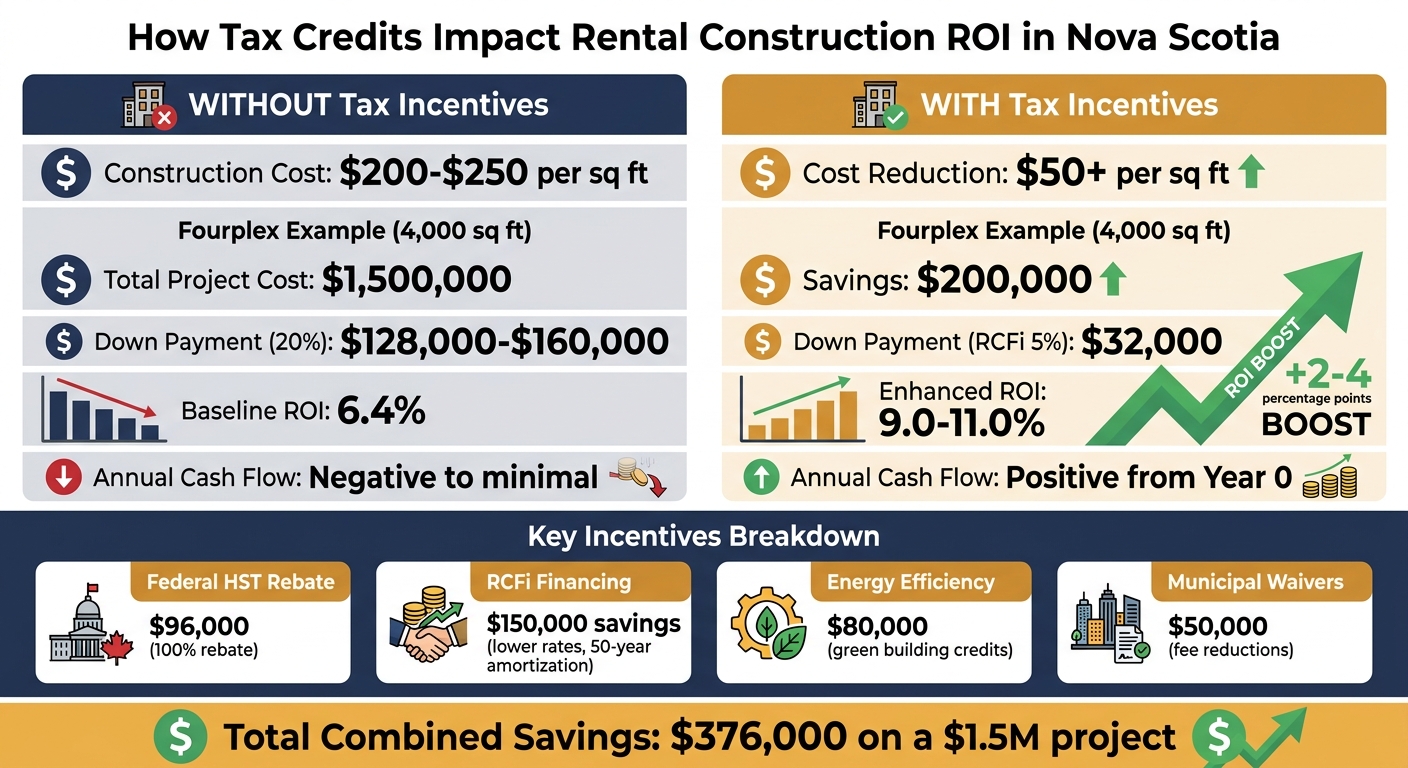

Let’s break it down with an example. Imagine a Halifax fourplex with a construction cost of C$1,500,000 that generates C$120,000 in annual gross rent. With operating expenses around C$24,000 (a 20% expense ratio), your net operating income comes to C$96,000. Based on these numbers, your baseline ROI is about 6.4%.

Now, consider tax credits. A 100% HST rebate worth C$96,000 and municipal fee waivers of C$50,000 reduce your effective cost to C$1,200,000. This adjustment raises your ROI to roughly 8.0%.

If you also stack energy efficiency credits and RCFi financing, your effective cost could drop further to around C$1,125,000. With these incentives, your net income might increase to C$100,800, boosting your ROI to approximately 9.0%.

Combining Multiple Incentives

Stacking various incentives can significantly enhance your returns, but it requires careful coordination. Federal, provincial, and municipal programs often allow you to combine benefits, provided you meet their specific requirements. For example:

- RCFi Financing: Reduces mortgage rates, potentially saving you around C$150,000.

- HST Rebate: Refunds construction taxes, worth approximately C$96,000.

- Energy Efficiency Credits: Covers green building costs, adding about C$80,000.

- Municipal Fee Waivers: Saves another C$50,000.

In total, these incentives could add up to C$376,000 on a C$1,500,000 project, reducing your effective investment to about C$1,124,000. This significantly improves your ROI. To maximize these benefits, keep detailed records and meet all deadlines for applications and documentation.

Conclusion

Tax credits and financing programs play a critical role in making rental construction more feasible in Nova Scotia. By combining tools like CMHC's RCFi financing, provincial property tax reductions, energy efficiency rebates, and municipal fee waivers, property owners can cut effective project costs by 12–18%. This directly improves cash-on-cash returns and accelerates portfolio growth. For example, a fourplex with a 7% ROI without incentives can achieve 10–11% when these programs are utilized - a boost of 2–4 percentage points. Over a 20-year hold, this improvement could add hundreds of thousands of dollars to your net worth.

As outlined earlier, layering federal, provincial, and municipal incentives creates a well-rounded financial approach to maximize returns. RCFi financing lowers debt service costs throughout the project’s lifecycle. HST rebates and municipal fee waivers reduce your upfront expenses, while operational tax deductions enhance your yearly cash flow. These incentives don’t just work in isolation - they amplify each other, creating a compounding effect that strengthens your financial outcomes.

To fully benefit, you need a strategic approach from the start. Work with a tax accountant experienced in rental property incentives, consult CMHC early on to confirm RCFi eligibility, and explore municipal programs before finalizing your project plans. Careful documentation and meeting deadlines should be part of your planning process, not something left until later.

FAQs

Can I stack federal, provincial, and municipal incentives on one build?

Yes, it's possible to stack federal, provincial, and municipal incentives for a single build in Nova Scotia. For instance, you can take advantage of the federal GST/HST rebate, claim provincial tax credits, and apply for municipal support programs. However, you’ll need to meet the specific eligibility requirements for each incentive to combine them successfully.

What deadlines could cause me to lose an HST or energy rebate?

Missing important deadlines can cost you an HST or energy rebate. For instance, you need to apply within two years of completing construction or paying the HST. Specifically for the HST rebate, your project must begin after September 13, 2023, and wrap up by December 31, 2036. If you miss these timelines, you could lose your eligibility entirely.

How do affordability commitments affect refinancing and cash flow later?

Affordability commitments, like energy efficiency rebates and municipal support programs, can directly improve your bottom line. By cutting upfront construction costs and reducing ongoing operating expenses, these initiatives free up cash flow. Over time, they can also increase rental income, making the property more attractive to tenants while improving your overall return on investment (ROI) for multi-unit rentals.