How to Replace Your Salary with Rental Income from Purpose-Built Housing

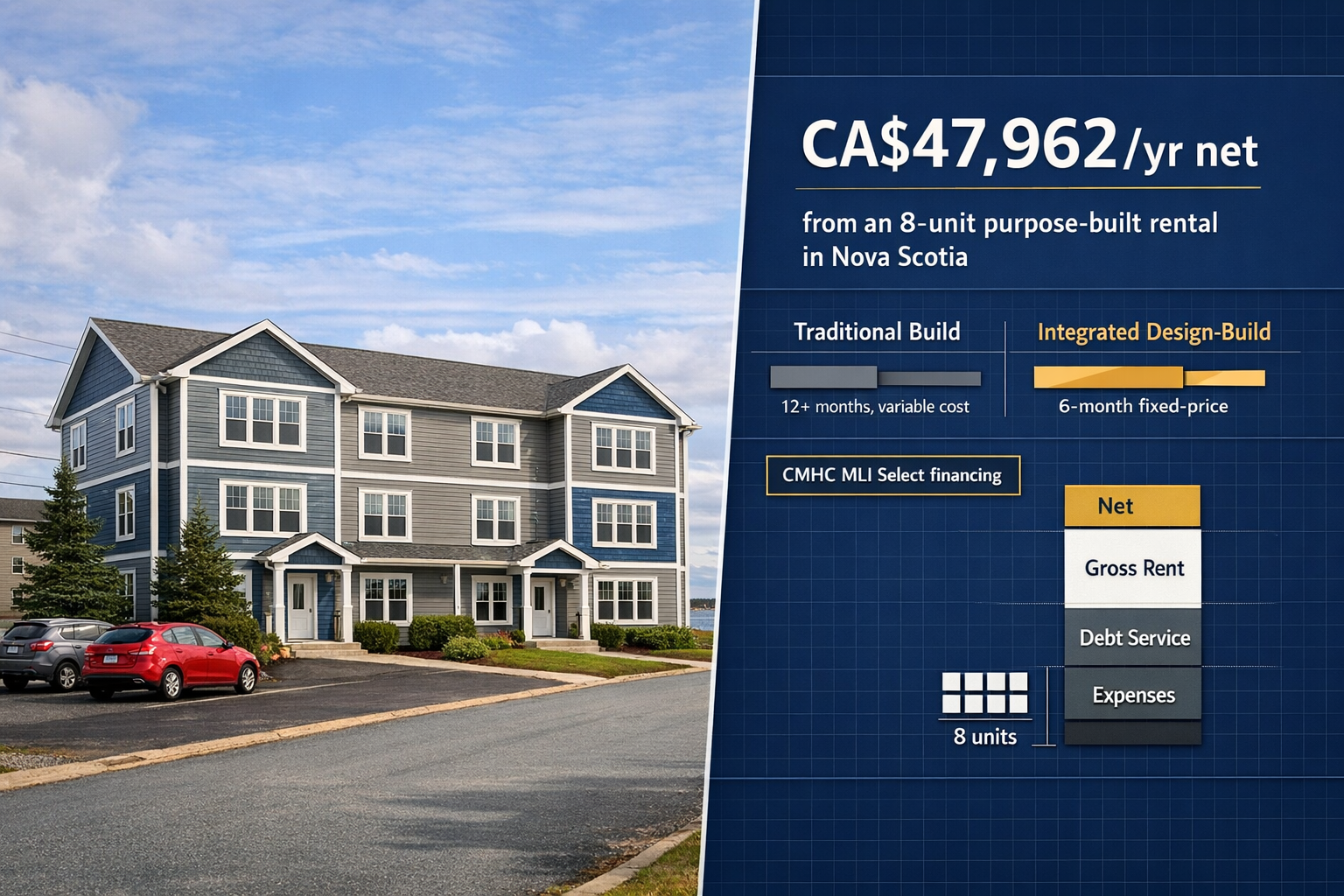

If you're wondering how to replace your salary with rental income, the numbers matter. In Nova Scotia, an 8-unit purpose-built rental property can generate $3,997 in monthly net cash flow - that’s $47,962 annually, enough to match many full-time salaries. With CMHC MLI Select financing, you can build with as little as 5% down, and extended amortization periods of up to 50 years keep your monthly payments low. Based on the Halifax rental market outlook, rents for new 2-bedroom units average $2,400 per month, making this strategy achievable for property owners with land and a plan.

This guide breaks down the 5 steps to replace your salary: setting income targets, securing financing, building at $160,000 per unit, projecting returns, and turning your land into tenant-ready units in just 6 months. Let’s dive into the details so you can decide if this approach fits your goals.

5 Steps to Replace Your Salary with Rental Income in Nova Scotia

Step 1: Calculate How Much Rental Income You Need

Set Your Income Replacement Target

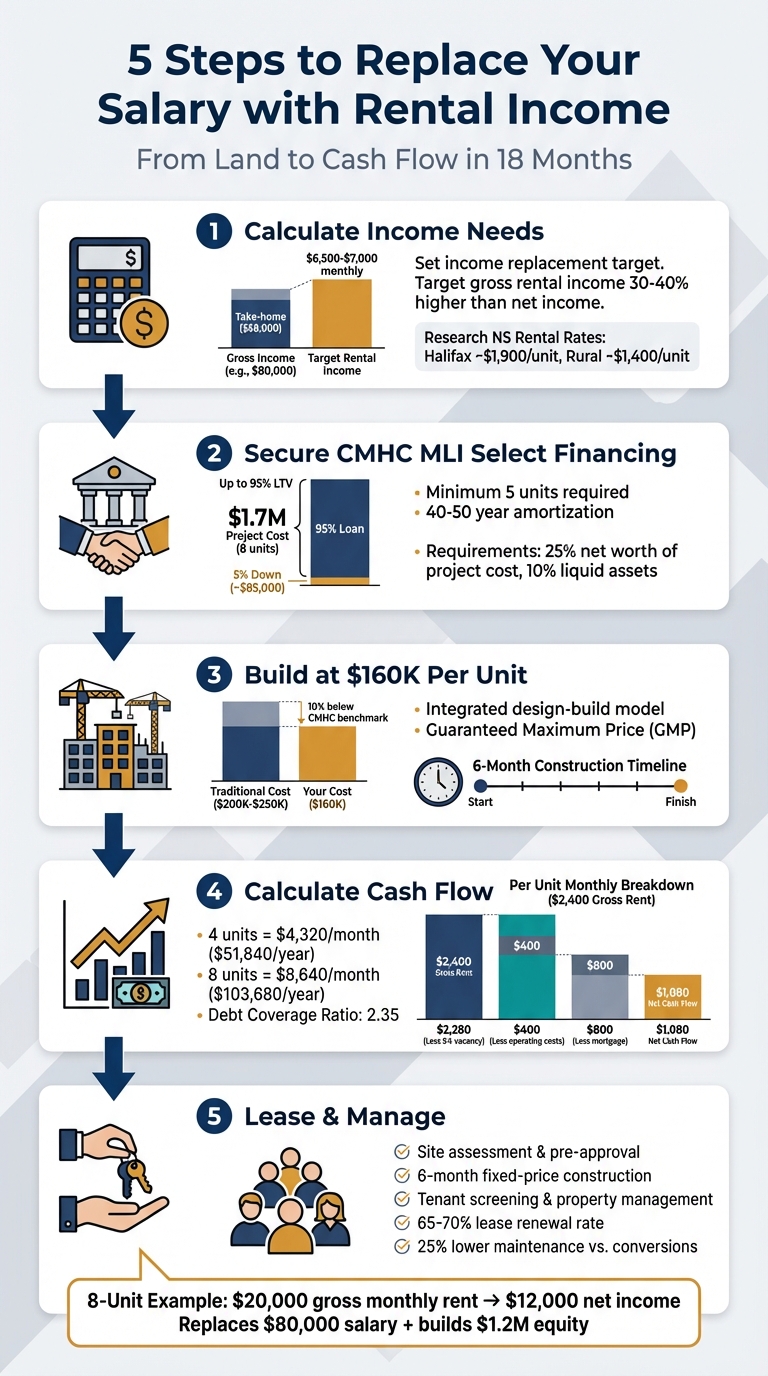

Start by figuring out how much after-tax income you need to replace. Use your latest pay stub or T4 form to determine your annual income after taxes and deductions like CPP and EI. In Nova Scotia, provincial tax rates vary from 8.79% on the first CA$29,590 to 21% on income above CA$150,000.

For example, if your gross annual income is CA$80,000, your take-home pay might be around CA$58,000 after taxes - roughly CA$4,833 per month. To account for rental operating costs, which typically eat up 25–35% of gross rent, aim for gross rental income that’s 30–40% more than your net income. This means targeting monthly rental income in the range of CA$6,500 to CA$7,000. A 4-unit property, with each unit renting for about CA$1,800, could meet this target and generate enough cash flow to begin replacing your salary.

Once you’ve set your income goal, compare it against local rental market data to ensure it’s realistic.

Research Nova Scotia Rental Rates

Check current rental rates in Nova Scotia to confirm whether your income target aligns with market conditions. The CMHC Housing Market Reports (available at cmhc-schl.gc.ca) provide up-to-date data. As of 2025, the average rent for a 2-bedroom unit in the province is about CA$1,650 per month. In Halifax, it’s closer to CA$1,900, while rural areas like Truro or Sydney see averages around CA$1,400.

For newer, well-finished units with features like quartz countertops, ductless heat pumps, and in-unit laundry, Halifax rents can climb to CA$2,000–CA$2,500 per month for a 2-bedroom unit. In smaller towns, similar units typically rent for CA$1,400–CA$1,800. To calculate Net Operating Income (NOI), deduct about 5% for vacancies and 25–35% for operating expenses from gross rents.

Let’s break it down: a 4-unit property renting for CA$1,800 per unit generates CA$7,200 in gross monthly rent (CA$86,400 annually). After deducting 35% for expenses and vacancies, the net annual income is about CA$56,160, or CA$4,680 per month. If you can push rents closer to CA$2,000 per unit and manage expenses down to 28%, gross monthly rent would rise to CA$8,000, with a net income of approximately CA$5,760 per month.

These figures are crucial for planning your financing and construction strategy in the next steps. Tools like the CMHC Rental Universe and input from MLI Select lenders can help validate these projections through detailed pro forma analyses.

How to Replace Your Job Salary with Rental Cash Flow

Step 2: Finance Your Property with CMHC MLI Select

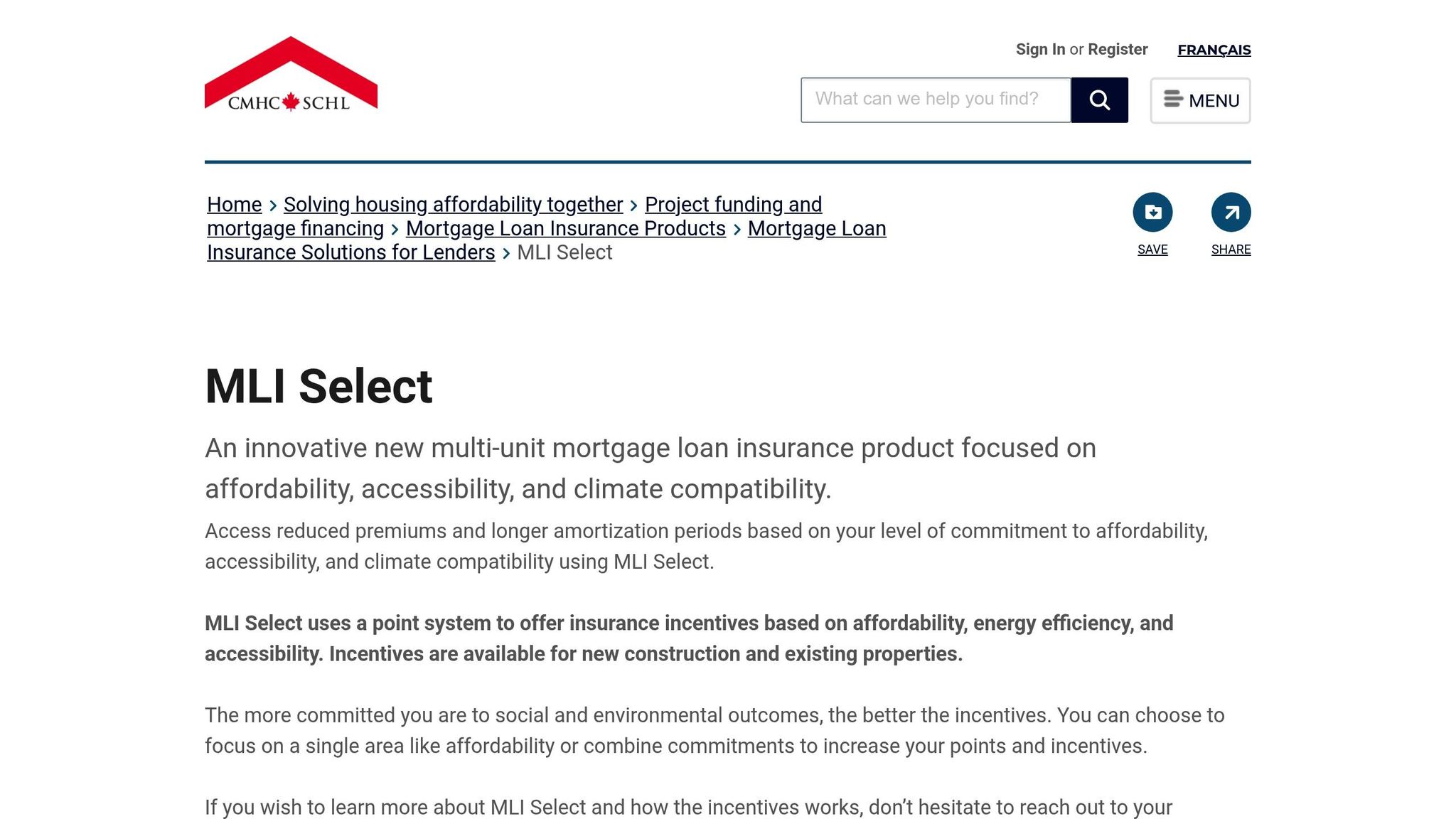

Once you’ve verified that your income targets align with Nova Scotia rental rates, the next move is securing financing that supports your project’s numbers. The CMHC MLI Select program is tailored for purpose-built rental properties with five or more units. It offers loan-to-value (LTV) ratios of up to 95% and amortization periods as long as 50 years. This means you can potentially build a rental property with just 5% down, minimizing the equity you need to contribute. This financing framework builds on the income targets from Step 1, helping you manage construction costs and plan for cash flow effectively.

CMHC MLI Select Qualification Requirements

To qualify for MLI Select, your property must include at least five units - this is the dividing line between standard residential financing and commercial rental financing [1]. CMHC evaluates projects using a points system, with scores based on affordability, energy efficiency, and accessibility. Properties scoring 50, 70, or 100 points are eligible for amortization periods of 40, 45, and 50 years respectively. Higher scores may also allow for limited-recourse lending, reducing your personal financial exposure [2][5].

Energy efficiency is a particularly achievable category for many Nova Scotia property owners. You can earn points by incorporating features like ductless heat pumps, triple-pane windows, and a Heat Recovery Ventilator (HRV) system [1]. These upgrades require energy simulations conducted by accredited professionals such as Professional Engineers, Architects, or Certified Energy Managers (CEM) [2]. For affordability points, at least 10% of units in your project must be priced so tenants spend no more than 30% of the median renter income for the municipality. CMHC provides this income data for each area [2][4]. Affordability commitments must last at least 10 years, but extending them to 20 years can earn extra points [2].

From a financial standpoint, borrowers need a net worth equal to 25% of the project costs, along with liquid assets sufficient for a 5–10% deposit and a 10% contingency [3][4][2][5]. For example, if you’re building an eight-unit property with a total cost of CA$1,704,760, you’d need a net worth of about CA$426,000 and liquid assets of roughly CA$255,000.

Financing Benefits for Multi-Unit Rentals

If your goal is to replace your salary with steady rental income, MLI Select financing can provide a major advantage. With a 95% LTV option, an eight-unit project costing CA$1,704,760 would require just 5% in equity - about CA$85,000 - far less than the standard 25% down payment required for most conventional financing [1][3][2]. The extended amortization period, up to 50 years, also reduces your monthly debt payments, improving cash flow.

High-scoring projects under CMHC’s points system can unlock additional benefits, such as reduced insurance premiums and access to competitive 10-year mortgage rates [3][5]. If your project scores 100 points or keeps its LTV below 65%, you may also qualify for limited-recourse lending, further lowering your personal financial risk [2][4]. This combination of reduced equity requirements, extended amortization, and risk mitigation positions MLI Select as a strong choice for building income-generating rental properties.

Step 3: Build at $160K Per Unit

Once you’ve secured MLI Select financing, keeping construction costs in check becomes critical to maintaining the cash flow projections you established earlier. Traditional builds typically run between CA$200,000 and CA$250,000 per unit, but an integrated design-build approach can bring this down to CA$160,000 per unit - about 10% lower than CMHC's benchmark pricing. This cost reduction is achieved by cutting out unnecessary coordination and multiple contractor markups.

Integrated Design-Build vs Cost-Plus Construction

In a traditional cost-plus model, separate contractors handle design, engineering, and construction. Each adds their own markup, and the property owner bears the risk of budget overruns and schedule delays. In contrast, the integrated design-build model uses a single contractor from the start, locking in a Guaranteed Maximum Price (GMP). This eliminates bidding wars and focuses on delivering value within a set budget [6].

Why this matters to property owners: A fixed-price contract ensures you know exactly what you’ll spend before construction even begins. This removes the risk of unexpected costs derailing your project. Additionally, design managers collaborate directly with in-house estimators to ensure that every design decision aligns with your budget.

For even more efficiency, pre-designed multi-unit buildings can simplify the process further.

Pre-Designed Multi-Unit Buildings

Pre-designed multi-unit buildings skip the lengthy custom design phase, saving both time and money. These layouts are specifically designed for rental properties, with features like durable fixtures to withstand tenant turnover and bedrooms placed on opposite sides of the unit to appeal to roommates [7]. Integrated design-build methods also improve operational efficiency, reducing maintenance costs over the long term [7].

For property owners looking to replace their salary with rental income, this approach means fewer unexpected repair bills and steadier expenses. Plus, these pre-designed buildings meet CMHC financing criteria, ensuring your project qualifies for MLI Select right from the start.

sbb-itb-16b8a48

Step 4: Calculate Your Cash Flow and Returns

Using the CA$160,000 per unit cost from Step 3, it’s time to figure out if your rental income can replace your salary. This means breaking down the monthly cash flow per unit and scaling the building size until it hits your income target. Start by projecting gross rents, subtract operating costs and mortgage payments, and ensure you meet at least a 1.10 Debt Coverage Ratio (DCR). Let’s dive into the numbers for per-unit cash flow and see how scaling your portfolio can work in your favour.

Monthly Cash Flow Per Unit

Start with market rents. As of March 2026, a new 2-bedroom unit in the Halifax metro area typically rents for around CA$2,400 per month. Factor in a 5% vacancy rate, and your gross rent drops to CA$2,280 per unit monthly. Operating costs - covering property taxes, insurance, maintenance, and management - average about CA$400 per unit each month. That leaves you with a Net Operating Income (NOI) of CA$1,880 per month per unit.

Now, let’s look at financing. Using CMHC’s MLI Select program with 95% loan-to-value, a 5% interest rate, and a 45-year amortization, the mortgage payment comes to about CA$800 per unit per month. This leaves a net cash flow of approximately CA$1,080 per unit monthly (CA$2,280 – CA$400 – CA$800), or CA$12,960 annually per unit. With a 2.35 DCR, this setup offers a solid financial cushion.

Scale from 4 Units to 8 Units

Scaling up increases both income and financing advantages. A fourplex generates around CA$4,320 in monthly net cash flow, enough to replace a CA$50,000 salary but with limited room for growth. Moving to an eightplex, you’re looking at roughly CA$8,640 in monthly cash flow, which comfortably replaces a CA$100,000 salary. Plus, an eightplex qualifies for CMHC’s 50-year amortization, lowering your monthly debt payments even further.

Here’s the bigger picture: an 8-unit building costs CA$1,704,760 (including HST and soft costs) and has an immediate property value of CA$2,900,000. That’s CA$1,195,240 in equity on day one, along with the cash flow to step away from your job [1].

Step 5: Turn Your Land into Rental Income

To turn your land into a dependable income source, follow these steps: evaluate your site, secure financing, build the property, and lease it to tenants. This process unfolds in three main phases - site approval, construction, and tenant management - each critical to transforming your land into a steady monthly income stream.

Site Assessment and Financing Pre-Approval

Before breaking ground, two key steps are required: confirming your land is suitable for development and obtaining financing pre-approval. This phase builds on your earlier financial planning and ensures your project aligns with CMHC MLI Select requirements. Start with a professional site assessment to check zoning compliance, utility access (water, sewer, power, gas), and whether the lot can support at least 5 units, the minimum for CMHC MLI Select financing. A land survey will define boundaries and topography, while a geotechnical analysis will flag any grading or foundation concerns. These evaluations cost between CA$3,000 and CA$5,000 but can save you from costly mid-project surprises.

Once the site passes inspection, move to financing pre-approval. CMHC financing requires a detailed investment breakdown, including project costs, projected Net Operating Income (NOI), and a fixed-price construction contract. Why this matters: Pre-approval confirms your project's financial feasibility, and the fixed-price model gives lenders the cost certainty they need to offer up to 95% loan-to-value financing.

6-Month Fixed-Price Construction

Once financing is secured, construction begins. A fixed-price contract takes the project from permits to tenant-ready units in just 6 months. The base construction cost is CA$160,000 per unit, covering architectural design, engineering, permits, foundation, framing, roofing, insulation, windows, plumbing, electrical, and HVAC. Add CA$30,000 per unit for site work and tenant-ready finishes. For an 8-unit building, the total cost averages CA$213,095 per unit, inclusive of HST and soft costs (approximately 8% of construction).

The fixed-price approach eliminates the chaos of managing multiple contractors, a common issue with cost-plus construction. Instead of juggling 6–7 different trades and absorbing delays or overruns, you get one integrated design-build contract. Helio offers this model with a CA$1,000-per-day penalty for delays, ensuring the builder is motivated to meet deadlines and stay on budget.

Tenant Screening and Property Management

After construction, the focus shifts to finding reliable tenants and maintaining your property. A thorough tenant screening process is non-negotiable: run credit checks, verify employment, and contact previous landlords to avoid risks like inconsistent income or poor rental histories. Amenities also play a big role in tenant retention. High-speed internet is a must for 64% of renters, particularly remote workers, while in-unit laundry and pet-friendly policies can justify higher rents and attract long-term tenants.

To keep your property running smoothly, schedule bi-annual inspections to catch small issues before they become expensive repairs. Purpose-built rentals typically have 25% lower maintenance costs than converted residential properties, and well-designed units see lease renewal rates of 65% to 70% [8]. Property management software can automate rent collection, accounting, and maintenance tracking, cutting down on operational headaches. Finally, set aside 3 to 6 months' worth of rental income as a buffer for unexpected vacancies or repairs. With careful tenant screening and proactive management, you can secure the steady cash flow needed to replace your salary.

Conclusion

Replace your salary in five practical steps: set your rental income target (consider Nova Scotia rents of CA$2,000–2,300 per unit); secure CMHC MLI Select financing with as little as 5% down; build purpose-built rentals at CA$160,000 per unit through an integrated design-build approach; ensure positive cash flow from the start; and transform your land with a 6-month fixed-price construction plan. For example, an 8-unit project generating CA$20,000 in gross monthly rent can produce CA$12,000 net income, replacing an CA$80,000 salary in under 18 months.

For property owners, this strategy means creating a cash-flowing asset with 95% loan-to-value (LTV) financing from CMHC and a 1.1 debt service coverage ratio, all while reducing personal risk. An 8-unit property can build CA$1,200,000 in equity, provided you start with at least 5 units to qualify for the best financing terms. Using a fixed-price contract ensures there are no budget surprises - an issue that often derails conventional builds.

To get started, evaluate your land's potential for 5+ units, confirm CMHC eligibility (25% net worth of project cost, 10% liquid assets, and 5–10% down payment), secure pre-approved financing, and request quotes for a CA$160,000-per-unit fixed-price build. Reach out to CMHC for a pre-application consultation, and use their Housing Market Reports to research current rental rates in your area. This will help refine your income projections and confirm your target is realistic.

Nova Scotia’s rental market - characterized by low vacancy rates and a steady 5% annual rent growth - offers a dependable income stream that can outperform conventional employment. With CMHC’s 50-year amortization, fixed construction costs, and strong tenant demand, you’re looking at a reliable path to financial independence that builds equity while providing steady cash flow.

Take the first step by calculating your income target and assessing your land’s development potential. This isn’t just a theory - it’s a proven, actionable plan supported by CMHC’s lending framework and Nova Scotia’s robust rental market. Your path to financial freedom starts today.

FAQs

What risks could reduce the projected cash flow?

Managing rental properties comes with its share of risks that can chip away at your projected cash flow. These include construction delays and cost overruns, which can stretch timelines and budgets; rising interest rates, which increase borrowing costs; and compliance requirements, like meeting stricter energy efficiency standards.

Additionally, market fluctuations - whether it's a dip in rental prices or higher-than-expected vacancy rates - can significantly impact revenue. There's also the potential for unexpected operational expenses, such as major repairs or maintenance, and economic or regulatory changes, like the introduction of rent control policies, which can limit income growth.

To stay ahead, property owners need to focus on detailed planning, strong project management, and keeping a close eye on market trends. These steps can help reduce risk and keep your investment on track.

How do I know if my land can support 5+ units?

To figure out if your property can accommodate five or more units, start by examining local zoning regulations and land use policies. In Halifax, for instance, ER-3 zoning permits multi-unit developments, but only on lots that meet certain criteria - like a minimum size of 600–700 m² for developments with five or more units. Measure your lot's size, frontage, and topography, and compare these against the zoning requirements. If you're unsure, reach out to your local planning department for clarification.

How many units do I need to replace my salary?

When deciding how many units you need, start by working backwards from your income goal and the rental income each unit can bring in. For instance, a properly managed fourplex in Halifax can bring in about $93,600 per year after expenses. If your target is $80,000 annually, a single fourplex might be enough. However, if you're aiming for a higher income, you'll likely need more units.

The key is to focus on net income - what’s left after covering all your expenses. To make financing easier, consider using programs like CMHC’s MLI Select, which can help you secure favourable terms.