REIT Returns vs. Building Your Own Rental Property: A 10-Year Comparison

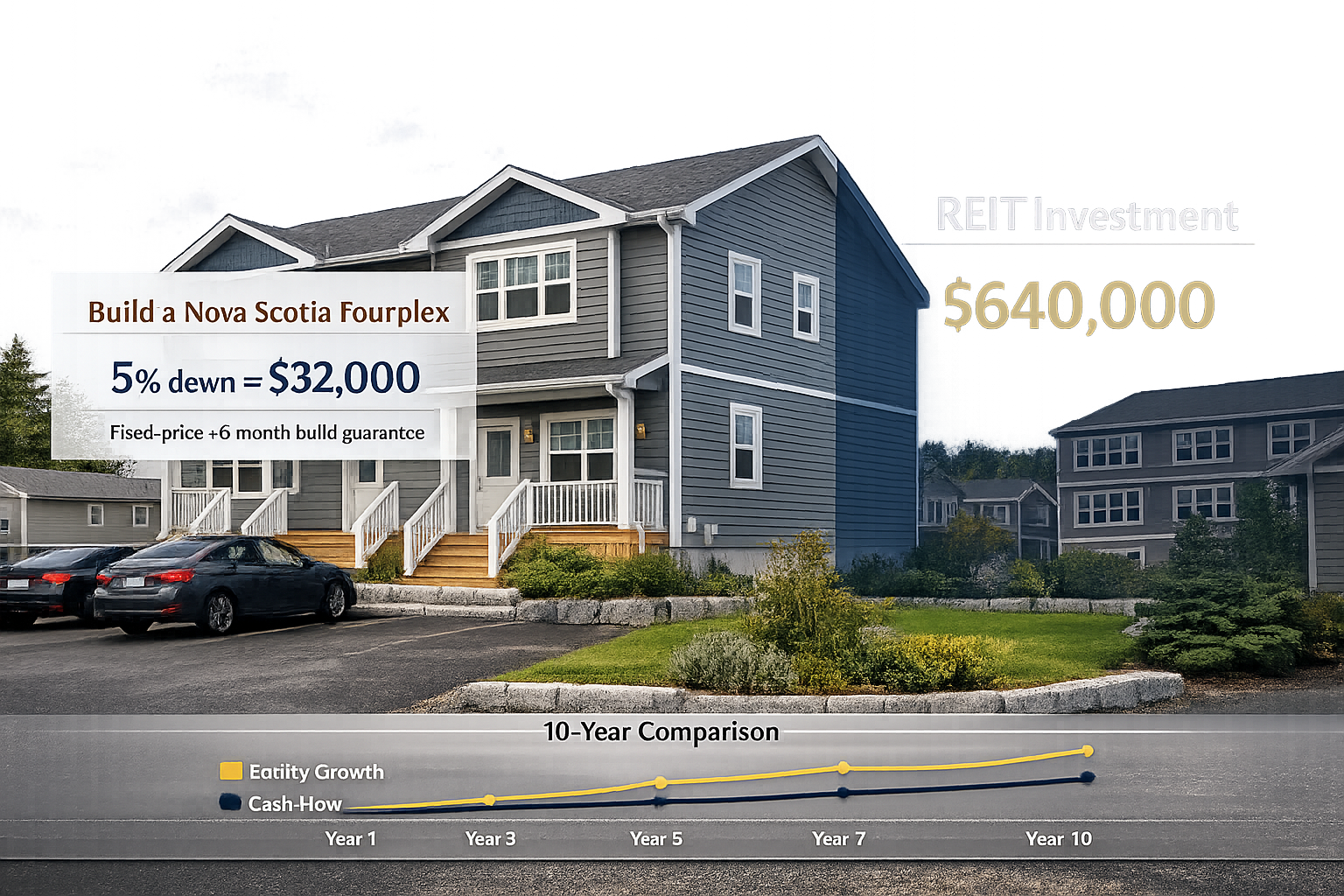

You’ve got $640,000 to invest and are weighing two options: buying shares in Canadian REITs like Killam Apartment REIT or building a fourplex in Nova Scotia. Both aim to grow your wealth, but which delivers better returns over the next decade?

In Halifax, rents hit $1,721/month in 2025, and CMHC’s MLI Select program lets you build a fourplex with just $32,000 down (5% of $640,000). Compare that to a REIT, where the full $640,000 is tied up as equity. This article breaks down the numbers - cash flow, equity growth, and effort - so you can decide which path fits your goals.

Passive Income Showdown: REITs vs Rentals

sbb-itb-16b8a48

REIT Investment Scenario: 10-Year Historical Performance

Investing $640,000 in Killam Apartment REIT (KMP-UN.TO), listed on the TSX, gives you access to a professionally managed portfolio worth about $5.5 billion. This portfolio includes over 18,800 apartment units spread across Atlantic Canada and Ontario [6]. Killam's current share price is approximately $16.96 CAD, offering a 4.25% dividend yield [4][5]. By investing in this REIT, you avoid dealing with construction schedules, tenant issues, or maintenance, as all property management is handled by the REIT.

Since 2007, Killam has steadily increased its dividend, currently paying $0.06 per share monthly, which totals $0.72 CAD annually [4][5][6]. Over the last decade, its Funds From Operations (FFO) per share grew from approximately $0.57 in 2015 to $0.82 in 2024. With a 10-year dividend growth rate of 1.84% and a manageable payout ratio of 41.3%, Killam demonstrates a commitment to financial discipline [5][7]. Apartment occupancy rates are strong, sitting at 97.2% as of late 2025 [6]. These factors highlight the potential for compounding returns when dividends are reinvested.

Return Projections and Compounding Effects

Compounding plays a key role in boosting REIT returns. For context, the FTSE NAREIT All Equity REIT Index achieved an average annual return of 5.70% over the past 10 years (as of March 31, 2025). Over 25 years, its average return was 9.90%, outperforming both the S&P 500 (7.41%) and the Russell 2000 (6.83%) [1]. Killam's total returns are estimated at around 4.2% annually through 2030 [6]. By reinvesting dividends through a Dividend Reinvestment Plan (DRIP), you can purchase additional shares, further amplifying your returns over time.

At a 4.2% annual return with reinvested dividends, an initial $640,000 investment could grow to approximately $965,000 in ten years. This represents a gain of about $325,000, or roughly 51% on your original investment [2].

Benefits of REIT Investing

One of the standout advantages of REITs is liquidity. Selling REIT shares on the TSX takes just a few clicks, unlike selling a physical rental property, which can take months [12]. REITs also provide instant diversification across various property types and regions. Killam, for instance, has properties across multiple Atlantic provinces and Ontario, which helps cushion against downturns in any single market [10][11].

Additionally, all tenant and maintenance responsibilities are handled by professional management, saving you time and effort while reducing risks tied to direct ownership [12]. Another benefit is the steady income stream. By law, REITs must distribute at least 90% of their taxable income as dividends, making them a reliable source of high-yield income compared to other equities [9][10].

Direct Rental Property Scenario: Building a Nova Scotia Fourplex

Helio’s fixed-cost model estimates the construction of a fourplex in Nova Scotia at $160,000 per unit, totalling roughly $640,000 for the entire project [13]. With CMHC MLI Select financing offering 95% Loan-to-Value (LTV), the required down payment is just $32,000 - far lower than the upfront capital needed for traditional REIT investments [14][15]. This 95% LTV structure means you only need to cover 5% of the total cost, allowing you to maximize the impact of your initial investment. As David Chen from Dartmouth shared:

The fixed pricing model let me lock in my financing with confidence. My lender was impressed that every line item was guaranteed before we broke ground [13].

The MLI Select program provides additional advantages, such as amortization periods of up to 50 years for projects meeting 100 points through commitments to energy efficiency, affordability, or accessibility [14]. This extended amortization lowers monthly debt payments, improving cash flow from the start. The program also allows for a Debt Coverage Ratio (DCR) as low as 1.1, meaning your net rental income only needs to be 1.1 times your debt obligations to qualify [14][15]. These financing terms make it easier for a fourplex to generate positive cash flow quickly.

Annual Cash Flow and Equity Growth

In Dartmouth, where average rents for a fourplex hover around $1,324 per unit, total annual rental income could reach approximately $63,550 across four units [14]. After deducting operating expenses - typically 35–40% of gross rent to cover property taxes, insurance, maintenance, and vacancies - the net operating income (NOI) is likely in the range of $38,000 to $41,000 annually. With a 95%-financed mortgage of about $608,000 and a 50-year amortization, this setup could yield a positive cash flow of $8,000 to $11,000 in the first year.

Over time, equity growth compounds through both mortgage principal reduction and property appreciation. For example, if the property appreciates by 3% annually, the original $640,000 investment could reach a value of approximately $860,000 after ten years. Combined with principal paydown, this creates a strong foundation for significant equity growth over the long term.

Benefits of Building a Rental Property

One of the standout advantages of direct property ownership is the ability to control a high-value asset with a relatively small initial investment - just 5% of the total cost. This amplifies the returns on your invested capital. Unlike REITs, where decision-making is handled by management, direct ownership gives you full control over operational decisions, such as rent increases and property improvements. This control not only boosts cash-on-cash returns but also accelerates equity growth through appreciation and mortgage paydown.

Additionally, direct ownership supports long-term wealth accumulation. While REITs distribute most of their income as dividends, owning a rental property allows you to reinvest gains through principal reduction and property appreciation. These benefits compound over time, often on a tax-deferred basis, providing a pathway to building lasting wealth.

Side-by-Side Comparison: ROI, Cash Flow, and Equity Growth

REIT vs Rental Property Investment Comparison: 10-Year Returns and Key Metrics

When you compare REIT investing to owning a Nova Scotia fourplex, the numbers tell two very different stories. Canadian REITs have delivered annualized returns of 7.17% to 8.61% over the past decade [16], with dividend yields typically falling between 3% and 7% [8]. On the other hand, owning rental properties in Nova Scotia, particularly when financed through CMHC MLI Select, can generate cash-on-cash returns of 8% to 12% annually [8][17]. And that’s before factoring in the additional equity growth from mortgage paydown and property appreciation, which can significantly boost total returns.

A major advantage of direct ownership is the leverage it provides. With a 95% LTV mortgage, a $32,000 down payment lets you control a $640,000 property. If the property appreciates by just 3% annually, you’re looking at a $19,200 gain in the first year alone - a 60% return on your initial $32,000. As Andrew Izyumov, CFA and Founder of 8FIGURES, explains:

A 20% property value increase - common in strong markets - produces a 100% return on the initial investment [through leverage] [8].

This kind of leverage isn't available with REITs, as their debt is managed at the corporate level, leaving individual investors without the same multiplier effect.

Tax Treatment and Leverage Impact

Tax rules further highlight the differences between these two investment paths. REIT dividends are taxed as ordinary income, with rates reaching as high as 37% unless held in an RRSP or TFSA [8]. In contrast, owning rental property allows you to claim deductions for mortgage interest, property taxes, maintenance, insurance, and depreciation [8][17]. These deductions can significantly reduce or even eliminate taxable income in the early years, helping you retain more cash flow while building equity through tenant-paid mortgage payments.

While REIT investors can reinvest dividends through DRIPs (Distribution Reinvestment Plans) [18], rental property owners see equity grow automatically through monthly mortgage paydowns. For example, over 10 years, a $608,000 mortgage with a 50-year amortization could generate $80,000 to $100,000 in equity from principal reduction alone - before even considering property appreciation.

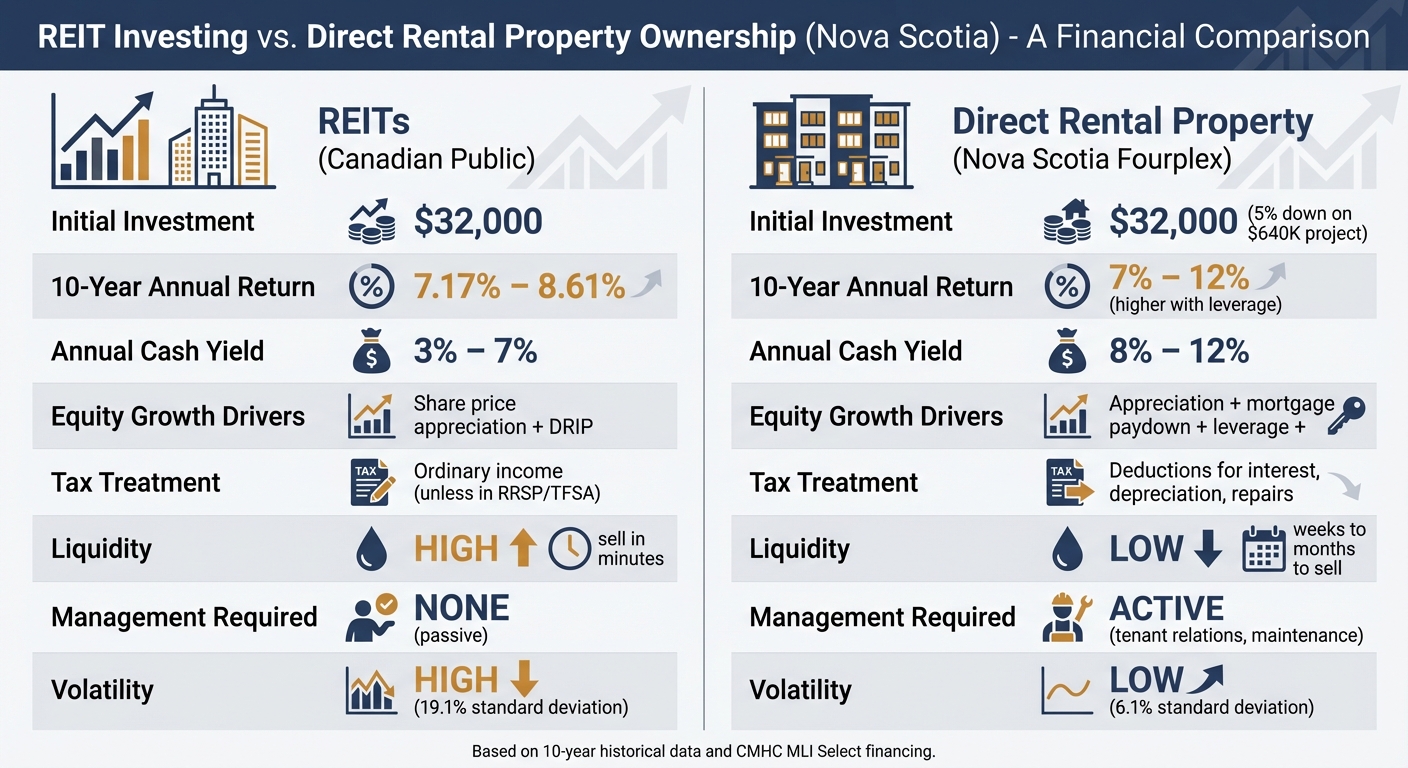

Full Comparison Table

Here’s a side-by-side breakdown of key metrics to help clarify the differences:

| Metric | REITs (Canadian Public) | Direct Rental Property (Nova Scotia Fourplex) |

|---|---|---|

| Initial Investment | $32,000 | $32,000 (5% down on a $640K project) |

| 10-Year Annual Return | 7.17% – 8.61% [16] | 7% – 12% (higher with leverage) [8][17] |

| Annual Cash Yield | 3% – 7% [8] | 8% – 12% [8] |

| Equity Growth Drivers | Share price appreciation + DRIP [18] | Appreciation + mortgage paydown + leverage [8] |

| Tax Treatment | Ordinary income (unless in RRSP/TFSA) [8] | Deductions for interest, depreciation, repairs [8][17] |

| Liquidity | High (sell in minutes) [8] | Low (weeks to months to sell) [8] |

| Management Required | None (passive) [8] | Active (tenant relations, maintenance) [8] |

| Volatility | High (19.1% standard deviation) [8] | Low (6.1% standard deviation) [8] |

What this means for property owners: For those with $32,000 to invest, the choice between REITs and direct ownership comes down to priorities. If you’re looking for higher equity growth through leverage and tax efficiency, building a fourplex with CMHC MLI Select financing is a strong contender. However, it does require active involvement in managing tenants and maintenance, unlike the passive nature of REITs.

Risk and Effort Analysis: Liquidity, Management, and Market Exposure

When deciding between REITs and direct property ownership, you need to weigh how much time you're willing to commit and how quickly you might need access to your investment. Public REITs provide near-instant liquidity, while selling a property like a fourplex can take months and comes with 5–6% in commissions and legal fees [20][18]. As the Parvis Team explains:

Public REITs... enjoy instant liquidity, like with any other publicly-listed security. But in exchange, they accept correlation with the public markets – and the volatility that comes with it [19].

This difference in liquidity also sets the tone for the varying management demands of these two approaches.

Management Time Requirements

REITs are essentially hands-off. Professional teams handle everything - acquisitions, tenant relations, and maintenance. In contrast, direct property ownership requires active involvement. Even if you hire a property manager, which typically costs 8–12% of monthly rents [22][3], you’ll still need to dedicate time to oversee operations. This includes approving major repairs, screening tenants, verifying invoices, and conducting periodic property inspections. These tasks can add up to 5–20 hours per month per property [23].

For property owners: If you prioritize flexibility and minimal involvement, REITs are the better option. However, if you prefer being directly involved in tenant selection, property improvements, and overall management, direct ownership could be more appealing [24].

These management differences also tie into the types of risks each investment faces.

Market and Economic Risks

Both REITs and direct property ownership come with their own market risks, which can shape your long-term returns. REITs are exposed to stock market volatility, driven by investor sentiment and interest rate changes. Rising rates, for instance, can increase borrowing costs and reduce demand for dividend-yielding stocks [26]. On the other hand, owning property in Nova Scotia subjects you to local risks, including shifts in the job market, vacancy rates, and fluctuating construction costs [26]. For example, building in 2026 could mean dealing with unpredictable material prices and rising insurance premiums [27][28].

Direct ownership, however, offers some advantages as an inflation hedge since rents tend to rise with inflation. It also gives you control over tenant selection and property upgrades, which can help maintain or increase property value [26].

To reduce the concentrated risk of owning a single property, some investors turn to REITs, which diversify holdings across multiple regions and asset types [18][21]. For those leaning toward development, programs like CMHC MLI Select can lower upfront equity requirements to just 5% of project costs, easing the burden of high initial capital demands [25]. Jonathan Krieger, Partner at Doane Grant Thornton, highlights the importance of creative financing in today’s market:

Structured deals like vendor take‑back mortgages, reduced‑rate financing, longer closing periods, and equity participation are essential to reviving the real estate market [28].

10-Year Results: Which Investment Delivers Better Returns?

Here’s how the numbers stack up after 10 years. Your decision ultimately depends on what you value more: a hands-off approach or taking control to build wealth actively. REITs provide steady, hands-free returns, typically ranging from 8–10% annually, and you can liquidate shares instantly if needed [17]. On the other hand, building a multi-unit rental property in Nova Scotia offers something REITs can’t: immediate equity. For example, a fourplex can generate substantial equity right from the start, even before you make your first mortgage payment [25].

For those willing to take an active role in managing their investment, direct ownership delivers stronger numbers. You’re looking at 11.3% cash-on-cash returns, $47,962 in annual cash flow after covering debt payments, and the ability to drive appreciation by renovating or optimizing rents [25]. Plus, REITs can’t match the leverage you get with a 95% loan-to-cost mortgage through CMHC MLI Select. With just $32,000 down, you can control a $640,000 property [25].

The key trade-off is effort versus liquidity. REITs shine if you want instant liquidity and minimal involvement, making them ideal for busy professionals focused on diversification and simplicity [29]. But if you’re ready to put in the work, direct ownership in Nova Scotia offers tax advantages, leverage, and equity growth that can significantly boost your wealth over the next decade.

Jeremy Pagan, Research Analyst at Morningstar, puts it well:

Between the tax benefits and leveraged nature of housing, this approach [direct investment] can compound returns quickly [29].

Ultimately, the right choice comes down to your financial goals, risk appetite, and how much time you’re willing to invest.

FAQs

What interest rate does CMHC MLI Select assume?

The CMHC MLI Select program offers property owners the potential for lower down payments and extended amortization periods - sometimes stretching up to 50 years. However, the program does not publicly disclose specific interest rates. For precise and up-to-date information, it’s best to consult CMHC's official resources directly.

How does a 50-year amortization change my cash flow?

A 50-year amortization reduces monthly mortgage payments, easing short-term cash flow pressures by cutting monthly expenses. The trade-off? A larger portion of each payment goes toward interest in the early years, which means building equity takes much longer. While this setup improves immediate cash flow, it also results in higher total interest costs over the life of the loan and delays principal repayment. For investors, the key is weighing the benefit of better short-term cash flow against the downside of slower equity growth and increased overall costs.

What happens if rents or vacancies move against me?

If rents drop or vacancy rates climb, your cash flow and returns could take a hit. Higher vacancies mean less rental income, which can make it tougher to cover operating costs or mortgage payments. Similarly, falling rents reduce income and slow down equity growth. While Halifax's vacancy rates are currently low - hovering around 1% - there’s always the chance they could inch up. To manage these risks, focus on flexible planning, stay informed about market trends, and consider strategies like pre-leasing to keep your properties stable.