New Construction vs. Renovation: Which Path to Rental Income Makes More Financial Sense?

If you're a property owner in Nova Scotia deciding how to generate rental income, the choice between building new or renovating can feel like a tough call. In Halifax, new construction runs about $160,000 per unit (or $213,095 per unit when factoring in land, permits, and HST). Renovation costs, meanwhile, are harder to pin down, often swinging wildly based on the building’s condition and unforeseen issues. Beyond upfront costs, financing, operating expenses, and long-term returns all play a role in determining which approach makes more sense for your goals. This article breaks down the numbers so you can decide which strategy aligns with your timeline, budget, and risk tolerance.

New Construction vs Renovation Cost Comparison for Rental Properties in Nova Scotia

Renovating vs Building New: How to Determine

sbb-itb-16b8a48

Upfront Costs: New Construction vs. Renovation

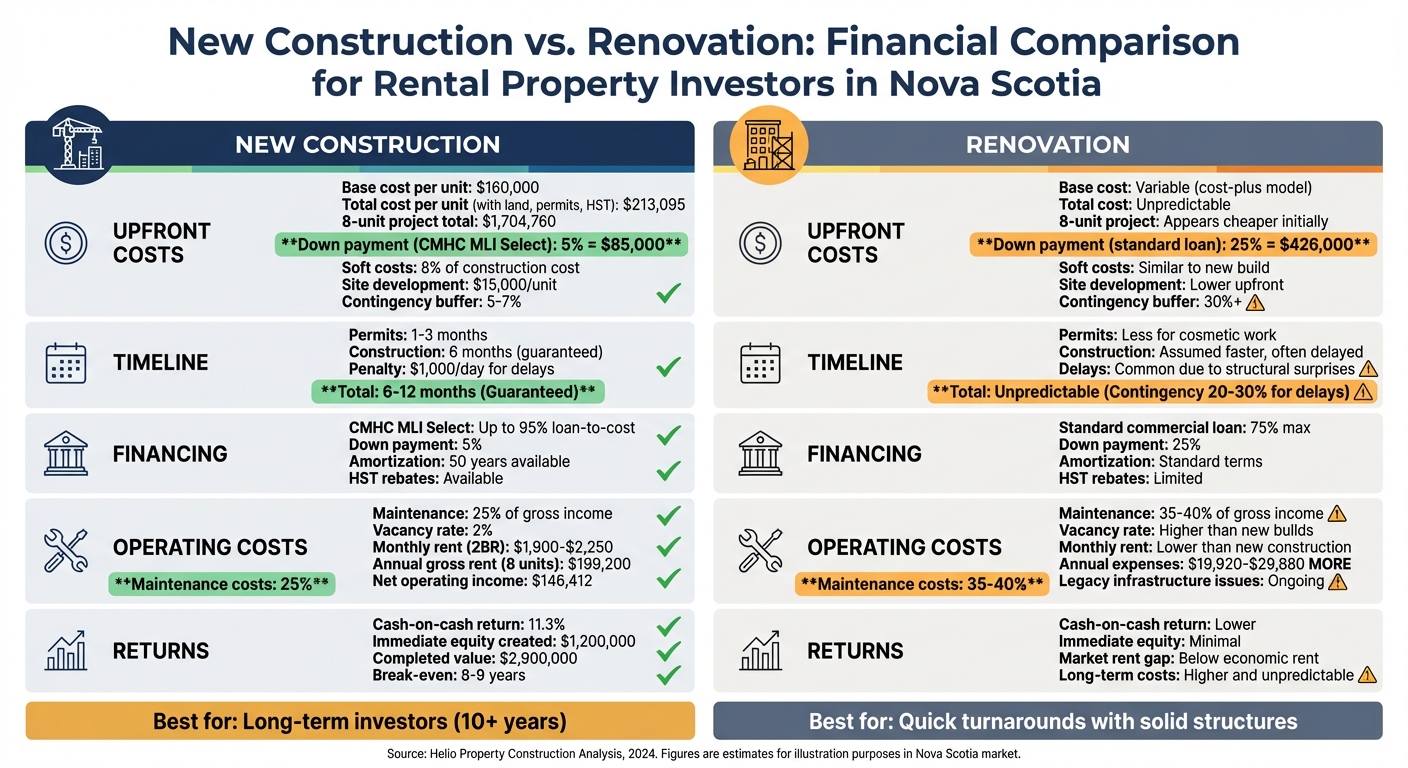

When comparing upfront costs, new construction in Nova Scotia starts at $160,000 per unit under a fixed-price contract. Renovation costs, on the other hand, depend heavily on the building's condition and operate on a cost-plus model, which makes final expenses harder to predict. For example, an eight-unit new build would cost approximately $1.28 million, while renovations might appear cheaper at first but often run over budget due to unexpected structural issues.

This cost disparity sets the stage for understanding the breakdown of hard and soft costs.

Hard Costs and Soft Costs

Hard costs in new construction - materials and labour - are locked in under the fixed-price contract. Soft costs, which cover architectural design, engineering, permits, and project management, typically add about 8% to the construction cost [1]. For an eight-unit project costing $1.28 million, soft costs amount to roughly $102,400. Additionally, Nova Scotia's 15% HST applies to the total project cost. However, for new residential rental properties, a portion of this HST may be recoverable [1].

Renovations face similar soft costs but come with added risks. Structural repairs, foundation work, and code compliance upgrades often emerge after demolition begins, making the final bill unpredictable. To account for these surprises, renovation budgets typically require a 30%+ contingency. In contrast, new construction offers the certainty of fixed pricing, reducing financial surprises.

Site development costs add another layer to the overall investment.

Site Development and Preparation

For new construction, site preparation is essential. This includes grading, utility connections (water, sewer, power), driveway installation, and basic landscaping. Helio’s Site Development Package covers these infrastructure needs at $15,000 per unit [1]. For an eight-unit building, this adds $120,000 to the total cost.

While renovations avoid some of these upfront site development costs, they often face higher long-term expenses. Issues like foundation repairs or outdated electrical and plumbing systems can lead to costly replacements.

Factoring in land, soft costs, and HST, the total investment for a new eight-unit build in Nova Scotia typically comes to $213,095 per unit [1]. Fixed-price contracts provide property owners with a clear, upfront cost structure, eliminating much of the budget uncertainty before the project begins.

Timelines: Construction Speed vs. Renovation Delays

When managing rental properties, having a predictable timeline is just as important as keeping costs under control. In the Maritimes, new construction projects typically take between 6 and 12 months to complete [3]. In Halifax, modern design-build firms have stepped up to offer fixed-price contracts with guaranteed timelines, removing much of the uncertainty that used to plague construction schedules [1]. For instance, Helio commits to a 6-month timeline from permits to handing over the keys, with a contractual penalty of $1,000 per day if they miss the deadline [1]. This level of certainty is invaluable for aligning project completion with rental market demand and income projections.

Renovations, on the other hand, are often assumed to be quicker, especially when the existing structure is solid. However, they frequently encounter delays due to unexpected issues [3][5]. Structural surprises, like hidden foundation damage or outdated wiring, can significantly extend renovation timelines [5]. To manage these risks, renovation budgets typically include a contingency fund of 20–30% for unforeseen delays, compared to just 5–7% for new builds [5].

This clarity in timelines makes new construction a more reliable option for property owners aiming to match rental income with mortgage payments. Renovation delays, on the other hand, can lead to higher carrying costs and disrupt cash flow.

Permits and Approvals

The permitting process also highlights the timeline differences between new construction and renovations. For new builds in Nova Scotia, permits take 1 to 3 months to secure before construction begins [3]. These permits cover everything from building and electrical work to plumbing, sewer connections, and site tests for water and soil conditions [4]. Once permits are in place, the construction timeline becomes much more predictable.

Renovations usually involve less permitting for cosmetic updates [5]. However, when structural changes are required, the same permits as new construction are often necessary. If unexpected issues like foundation repairs or electrical upgrades arise, the permitting process can stretch timelines unpredictably. To streamline this phase, professional developers in Nova Scotia often bundle permit applications with project management services, reducing coordination delays and helping projects move smoothly from design to "rental ready" [1].

Construction and Renovation Milestones

Once permits are approved, the next stages of the process further demonstrate why new construction tends to stay on schedule. New builds follow a clear sequence of milestones: laying the foundation, framing, reaching lock-up (when the structure is enclosed), insulating, and finishing [4]. Each step requires municipal inspections, but design-build firms coordinate these inspections to avoid unnecessary delays. The lock-up stage is especially critical in Nova Scotia’s climate, as it allows interior work to continue regardless of weather conditions [4].

Renovations, in contrast, often lack a fixed sequence of milestones. Scope creep - when the project grows beyond its original plan - can derail schedules. For instance, a simple cosmetic update might turn into a full structural overhaul once work begins, adding months to the timeline. For property owners relying on rental income, this unpredictability can delay cash flow and increase carrying costs, making renovations a riskier choice from a timeline perspective.

Financing Options: CMHC MLI Select vs. Standard Loans

The financing terms you choose can make or break the viability of a rental property project. For new builds with five or more units, CMHC MLI Select financing offers a game-changing advantage: a drastically lower down payment. This difference doesn't just impact your initial investment - it ripples through your monthly cash flow, long-term returns, and ability to grow your portfolio.

Under standard commercial loans, renovation projects typically require a 25% down payment. In contrast, CMHC MLI Select allows eligible new construction projects to secure up to 95% of the loan-to-cost ratio, meaning you could start with as little as 5% down [1]. Let’s break it down: for an eight-unit project costing $1,704,760, a standard loan would need a down payment of around $426,000. With MLI Select, you’re looking at just $85,000 [1]. That’s a massive difference, freeing up capital to reinvest or cover unexpected costs. These terms make new construction especially appealing in Nova Scotia’s rental market, where scaling efficiently is key.

Down Payments and Loan-to-Value Ratios

Only projects with five or more units qualify for CMHC MLI Select financing [1][6], which leaves most renovation projects out of the running. Standard commercial loans stick to the 25% down payment rule [1], but MLI Select slashes that to just 5% of the total project cost. This lower barrier to entry can be a decisive factor when considering new builds over renovations.

Financing Costs and Incentives

CMHC MLI Select doesn’t just stop at lower down payments. Approved new construction projects also benefit from reduced insurance premiums and eligibility for HST rebates [1]. In Nova Scotia, the 15% HST can feel like a heavy upfront cost, but the combination of high-leverage financing and these rebates often balances out the initial expense within the first few years of operation. This makes the program particularly attractive for long-term investors looking to optimize their cash flow and returns.

Long-Term Returns: Maintenance Costs and Rental Income

New construction tends to offer more predictable and lower-maintenance cash flow over the years, while renovated properties often face challenges from ageing infrastructure and unexpected repair costs. These factors have a direct impact on long-term cash flow and return on investment (ROI).

Maintenance and Capital Expenditure Differences

A major factor influencing long-term returns is how maintenance costs evolve over time. New builds are equipped with modern, energy-efficient systems like ductless heat pumps, HRV units, and durable materials such as quartz countertops, engineered hardwood floors, and triple-pane windows. These features help reduce the need for frequent repairs and keep operating costs consistent. In the Halifax rental market, maintenance costs for new properties are typically estimated at around 25% of effective gross income [1].

What sets new construction apart is the integration of design and build processes. This approach includes a single, comprehensive warranty, oversight by a Professional Engineer, and multiple inspections during construction. Together, these measures significantly lower the risk of unexpected expenses.

On the other hand, renovated properties often come with legacy infrastructure that can lead to unpredictable repair costs. Even after upgrades, older systems like electrical wiring, plumbing, or roofing may still require major repairs. The lack of a unified warranty further complicates long-term maintenance planning.

Keeping maintenance costs stable helps support higher rental values over time.

Rental Income and Vacancy Rates

New construction allows property owners to charge premium rents, thanks to modern designs and features. For example, newly built two-bedroom, one-bathroom units (about 800 square feet) in Halifax can command monthly rents ranging from $1,900 to $2,250. Vacancy rates for these units are projected to stay as low as 2% [1]. Features such as in-unit laundry, individual climate control, and superior soundproofing give new builds a competitive advantage that older buildings often struggle to match without significant investment.

Renovated properties, however, generally bring in lower rents, even after substantial upgrades. According to CMHC research, there’s often a gap between "market rents" (what tenants currently pay) and "economic rents" (the rent required to make new construction financially viable). This gap highlights why new builds need to charge higher rents to offset their development costs [2]. Renovated properties may fall short in generating enough rental income to cover ongoing repair expenses, while new construction supports a more sustainable model with premium rental income.

Nova Scotia Programs: Financial Benefits for New Construction

In Nova Scotia, provincial and federal programs offer financial perks that make new construction more appealing than renovation projects. One key advantage is the ability to recover part of the 15% HST charged on construction costs. For residential rental developments, rebate programs allow builders to reclaim a portion of this expense. For instance, on an 8-unit project with a base construction cost of $1,482,400, the HST adds $222,360 to the total cost. These rebates play a crucial role in improving the financial feasibility of new builds [1].

On top of this, the Affordable Housing Development Program (AHDP) further boosts the economics of multi-unit construction in Nova Scotia [1]. This program, when paired with favourable financing options like CMHC’s MLI Select, can significantly lower the equity required to start a project. With these combined resources, permanent equity requirements can drop to as little as 5% of the total project cost, accompanied by a 50-year amortization period. For an 8-unit project valued at around $1.7 million, this means a property owner might only need $85,000 in equity - much less than the 20–25% typically required for traditional financing or renovation loans.

Together, HST recovery and specialized financing options can reduce upfront capital needs by over $250,000 for a standard 8-unit project. The extended amortization period provided by federal programs also lowers monthly debt payments, improving cash flow from day one. These measures reflect government efforts to make purpose-built rental housing more financially accessible.

Break-Even Analysis: When New Construction Outperforms Renovation

When you break down the numbers, new construction starts to outperform renovation in cumulative returns within 8–9 years. This calculation accounts for upfront capital, financing structures, operating costs, and rental income premiums.

Let’s take an 8-unit project as an example. Financing plays a big role in narrowing the initial cost gap. With CMHC MLI Select financing, new construction may only require 5% equity - around $85,000 for a project of this size. In contrast, renovation loans typically need 20–25% down, which translates to $240,000–$350,000. This difference in equity requirements gives new construction a significant advantage upfront.

Operating costs also tilt the scale. New construction is generally more cost-efficient to manage. In Halifax, operating expenses for new builds average around 25% of gross rent, while older properties can range between 35–40% due to aging systems and deferred maintenance. For an 8-unit property earning $199,200 in annual gross rent, this 10–15% difference means an extra $19,920–$29,880 in yearly expenses for a renovated property.

Beyond operating costs, new construction units command higher rents. In Halifax, modern 2-bedroom units typically rent for $1,900 to $2,250 per month, while older units lag behind. Vacancy rates are another factor - new builds often maintain a low vacancy rate of around 2%, which further boosts net operating income.

To illustrate, Helio Urban Development conducted an analysis of an 8-unit new construction project in Halifax for 2024–2025. The total investment was $1,704,760, with monthly rents averaging $2,075 per unit. This property generated an annual net operating income of $146,412. Using a traditional financing structure with a 25% down payment (approximately $426,190), the project achieved an 11.3% cash-on-cash return. It also created about $1,200,000 in immediate equity, as the completed property was valued at $2,900,000.

Conclusion: Choosing the Right Path for Your Property

Deciding between new construction and renovation comes down to your timeline, budget, and comfort with risk. New construction often suits property owners with a long-term outlook - 10 years or more - who want predictable costs, reduced maintenance, and access to CMHC MLI Select financing. Renovation, on the other hand, might be the better route if you’re looking for faster results or already own a property in good structural condition. This matches earlier points about lower maintenance costs and CMHC MLI Select’s favourable financing terms.

When you break down the numbers, new construction frequently comes out ahead. CMHC MLI Select financing can require as little as 5% equity, whereas renovation loans typically demand much higher equity contributions. This means new construction allows up to 95% loan-to-value financing, freeing up cash for other investments or expanding your portfolio.

Operating costs also play a big role in profitability. Modern systems in new builds cut down on maintenance expenses compared to older properties, directly increasing net operating income. For instance, with an 8-unit property generating $200,000 in annual rental income, even small differences in expense ratios can lead to significant yearly savings that compound over time.

FAQs

Do I qualify for CMHC MLI Select financing for my project?

If you're working on a project in Halifax, you might be eligible for CMHC MLI Select financing, provided it meets the program's criteria for energy efficiency and affordability. This type of financing comes with some practical perks, including positive cash flow, a low 5% down payment, and longer amortization periods. For qualifying projects, it’s a financing option worth considering.

How much contingency should I budget for a renovation in Nova Scotia?

Budgeting a contingency of 5–15% of your total renovation costs is a smart move for projects in Nova Scotia. The percentage you choose will depend on how complex your renovation is and the current market conditions. This buffer can help cover unexpected costs, keeping your project financially stable and on schedule.

What rent premium do new-build units typically earn in Halifax?

In Halifax, newly built rental units typically command a 6.7% rent premium over older properties. With rents continuing to climb and vacancy rates remaining low, these newer developments often generate higher rental income, making them an attractive option for property owners looking to maximise returns.