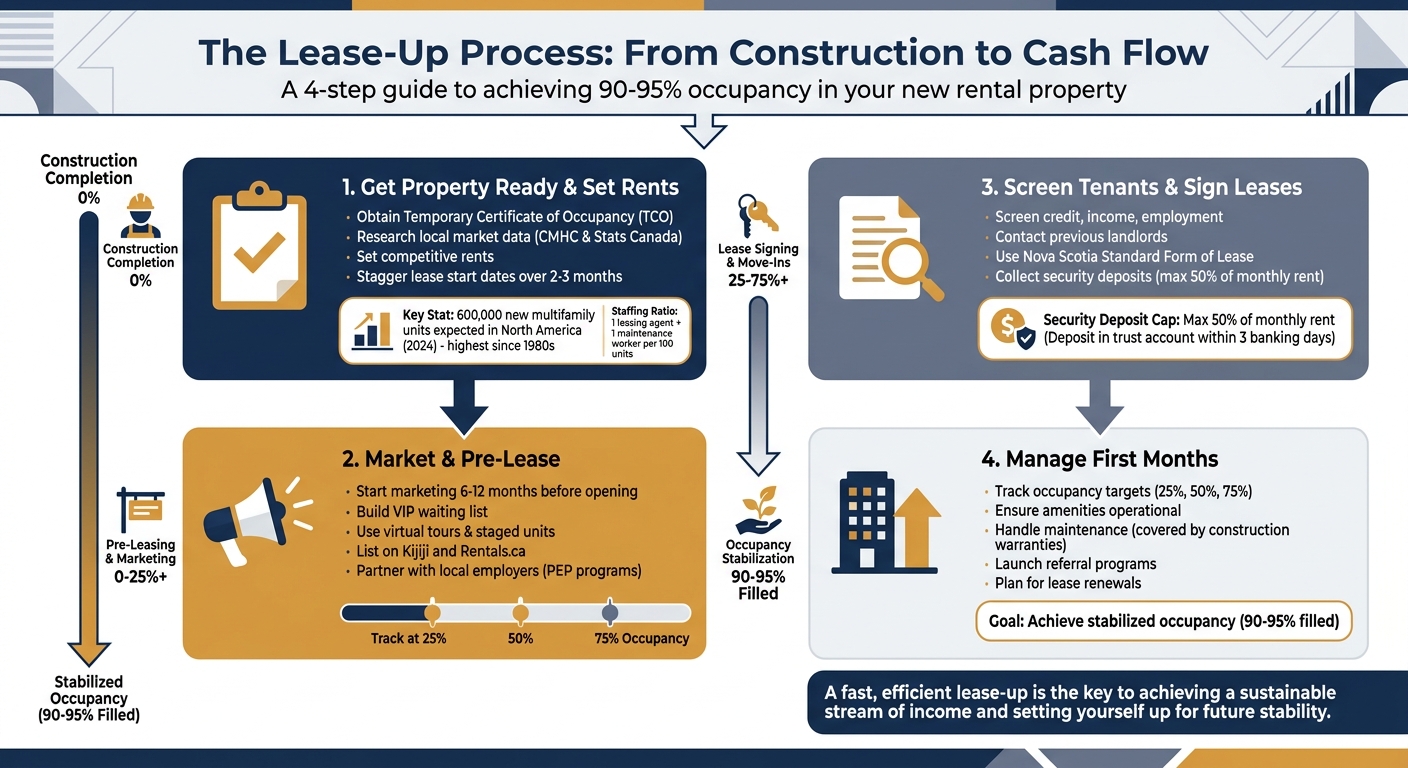

What Happens After Construction: The Lease-Up Process for New Rental Buildings

If you're holding the keys to a newly built rental property in Nova Scotia, you're probably asking: "How do I fill these units quickly without bleeding cash?" The lease-up phase is where the real financial pressure kicks in. Every empty unit means you're covering mortgage payments, property taxes, and insurance with no rental income to offset them. In Halifax, with the rental market seeing steady growth and competition from new builds, timing is everything. This article will break down how to get from construction completion to stabilized occupancy - typically 90–95% filled - as efficiently as possible. Let’s get into it.

4-Step Lease-Up Process for New Rental Properties in Nova Scotia

Understanding Lease Up Properties! 5 Tips for Marketing a Lease Up Property

sbb-itb-16b8a48

Step 1: Get the Property Ready and Set Your Rents

Before you start leasing, it's critical to finalize the steps that ensure legal occupancy and establish rents that attract tenants. These tasks directly impact how quickly your building fills and the income it generates.

Complete Final Inspections and Approvals

The Temporary Certificate of Occupancy (TCO) is your green light for move-ins. Without it, leasing units is off the table[1]. Delays in securing the TCO can derail your timeline, so work closely with your municipality to ensure inspections - especially for electrical systems and finishing touches like painting - are done on time. If you're conducting pre-completion tours, enforce safety measures such as hard hats and liability waivers for visitors[1]. Getting your TCO early not only avoids delays but also allows you to focus on marketing a move-in-ready property.

Once the TCO is in hand, you can shift to setting rents that reflect the local market.

Set Rents Using Local Market Data

Pricing units correctly from the start is critical. With about 600,000 new multifamily units expected across North America in 2024 - the most since the 1980s - competition is stiff, even in smaller markets[1]. Use CMHC Housing Market Reports and Stats Canada data to compare rents for similar unit sizes and amenities in your area. Establish benchmarks for occupancy rates at 25%, 50%, and 75% to assess whether your pricing strategy is working. To test your pricing, build a VIP list of prospective tenants and local real estate agents, and monitor the response. If inquiries are low, it could mean your rents are too high or your marketing approach isn’t connecting with the audience[1].

Once rents are set, plan lease start dates to ensure smooth operations.

Stagger Lease Start Dates

Starting all leases at the same time can overwhelm your team, especially when leases eventually expire. Spreading move-ins over two to three months helps balance the workload. For context, typical staffing ratios are one leasing agent and one maintenance worker per 100 units. If all tenants move out together, your team could be stretched beyond capacity. By staggering initial move-ins, you create a manageable cash flow pattern, prepare your team for future renewals, and maintain flexibility to adjust rents as market conditions shift[1].

Step 2: Market the Property and Start Pre-Leasing

With your property nearing completion and rental rates decided, the next move is to spark tenant interest through pre-leasing. This strategy helps you lock in tenants early, cutting down the risk of lingering vacancies once construction is finished.

Build a Waiting List Before Opening

Start marketing the property 6–12 months before opening to generate demand. Turn your initial VIP list into a more detailed waiting list that includes interested renters, local real estate agents, and representatives from major employers in the area. Use "Coming Soon" signage at the construction site, complete with QR codes that allow people passing by to sign up. A dedicated website featuring floor plans and video tours can act as your main tool for capturing leads. Adding AI chatbots to handle inquiries around the clock can also be a smart move. Early outreach lets you measure market interest and tweak your pricing if needed before signing leases.

Collaborate with local HR departments through Preferred Employer Programs (PEP) to offer perks like waived application fees or rent discounts for employees. Share behind-the-scenes updates of your construction progress on social media to build anticipation and create a relatable brand. Don’t forget to register the property on Google Maps and local directories early to attract online searches from individuals planning to relocate to the area.

Use Virtual Tours and Limited-Time Offers

Virtual tours on your website can help prospective tenants get a feel for the property without needing to visit in person. If in-person tours are feasible during pre-leasing, consider staging and furnishing one unit to give visitors a clear idea of the living experience - just ensure safety waivers are signed for any active construction site visits. Create urgency by offering "Early Access" to your VIP list, allowing them to tour staged units and secure leases before the general public. Limiting the number of available units shown can also encourage quicker decisions by creating a sense of scarcity.

You can enhance the appeal of pre-leasing by partnering with local businesses. For instance, offer early tenants deals like flat-rate moving services or discounts at nearby restaurants. These partnerships not only attract renters but also help establish your property as part of the neighbourhood.

List on Nova Scotia Rental Sites

When you’re ready to start accepting applications, post your property on platforms like Kijiji and Rentals.ca. Make sure your listings include professional photos, detailed floor plans, and transparent rent pricing. Track how well your listings perform at key occupancy milestones, such as 25% and 50%, and adjust your marketing efforts if interest seems low. A lack of applications could indicate that your pricing is too high or that your messaging isn’t connecting with your audience. Once applications begin coming in, you’ll move on to screening tenants and finalizing leases.

Step 3: Screen Tenants and Sign Leases

Once applications start rolling in, the next step is selecting tenants who can reliably pay rent and take care of the property. A solid screening process not only protects your investment but also helps ensure a smooth and stable tenancy.

Screen Applications Thoroughly

Check each applicant’s credit, income, and employment history. This includes running credit checks and contacting references. For those who lack traditional documentation, third-party rent-coverage insurance can be a good option to minimize risk while still accommodating qualified renters. Always contact previous landlords to confirm payment history and how well they maintained past properties.

Why this matters for property owners: Using consistent screening criteria for all applicants helps you maintain a fair process and reduces the risk of discrimination claims. It also ensures you’re choosing tenants who are more likely to meet their obligations.

Keep detailed records of your screening decisions. Once you’ve selected the right candidates, it’s time to finalize lease agreements.

Sign Lease Agreements

Use the Nova Scotia Standard Form of Lease to ensure you’re legally protected. Provide tenants with a copy of the lease, along with a summary of key tenancy rules [2][4].

Collect Deposits and Plan Move-Ins

After signing the lease, collect the required deposits and coordinate move-in dates to keep the process efficient. In Nova Scotia, security deposits are capped at 50% of one month’s rent [3]. These deposits must be placed in a trust account at a chartered bank, credit union, or trust company within the province by the third banking day after they’re received [2]. Keep detailed records for each tenant, showing all funds received and any undisbursed balances.

If you’re looking to speed up the lease-up process, consider offering deposit insurance options. These allow tenants to pay a small fee instead of a large upfront deposit, which can make your units more attractive.

To avoid confusion during move-ins, arrange for utilities to be transferred to tenants and set clear move-in dates. If construction is still ongoing in shared areas, let tenants know which facilities are unavailable and when they’ll be ready. You could also partner with local moving companies to offer flat-rate services as a bonus for new tenants. This kind of coordination helps create a seamless start for everyone involved.

Step 4: Manage the First Months of Operation

With tenants moving in and leases signed, your focus now shifts to running the property effectively. The initial months are crucial for keeping occupancy rates high and ensuring smooth operations.

Track Occupancy and Adjust Marketing

Set clear occupancy targets - like 25%, 50%, and 75% - to evaluate how well your marketing efforts are performing. At each checkpoint, analyse which unit types are leasing quickly and which are slower to move. For units that aren’t renting, consider offering move-in perks or discounts through partnerships with local businesses instead of lowering base rents right away [1]. This approach protects your long-term rental income while creating an incentive for prospective tenants.

Use property management software to link occupancy data with your financial metrics, ensuring cash flow aligns with your projections for loan payments and property taxes [5]. Stick to earlier staffing plans to maintain quality service. If leasing traffic is below expectations, consider boosting your digital marketing budget or hosting more open house events. These adjustments can help refine your tenant acquisition strategy.

For property owners: Tracking occupancy by unit type - not just overall numbers - lets you focus your marketing where it’s needed most, avoiding unnecessary rent cuts that could reduce your profitability.

Handle Move-Ins and Maintenance Requests

Ensure shared amenities like gyms, lounges, and pools are fully operational and stocked when tenants arrive. If some areas are still under construction, communicate clearly with residents about what’s accessible and the timeline for completion [1].

Most early maintenance concerns in new buildings fall under construction warranties, which can help keep your expenses minimal [1]. Use property management tools or mobile apps to handle service requests quickly. Prompt responses during these early months not only improve tenant satisfaction but also build a strong reputation [5]. Create a feedback loop to identify and address tenant concerns before they escalate.

Plan for Lease Renewals

Tenant retention starts from the very beginning. Providing excellent customer service during the first months builds trust and increases the chances of lease renewals [1]. Launch a referral program early on, offering incentives for tenants who bring in new renters, and actively manage your online reputation by responding to reviews [1].

When it’s time to renew leases, consider modest rent increases that reflect current market conditions. Retaining tenants is far more cost-effective than continually marketing vacant units, saving you both time and money in the long run.

Conclusion

Getting your building leased up quickly transforms it from a construction site into a revenue-generating asset. By focusing on early pre-launch marketing, setting rents that match the local market, and thoroughly screening tenants, you can achieve full occupancy faster. This speed is crucial for maintaining cash flow and ensuring long-term stability.

To break it down: treat lease-up as a structured process, not a last-minute scramble. Start building a waiting list before construction wraps up, stage a few units to help potential tenants picture themselves living there, and monitor occupancy rates closely. Adjust your marketing efforts as needed to stay competitive. In Nova Scotia, where rental markets are seeing steady new supply, these proactive steps can give your property a noticeable advantage. As The Guarantors put it, "A fast, efficient lease-up is the key to achieving a sustainable stream of income and setting yourself up for future stability." [1]

The first months are critical for establishing your property's reputation. Respond quickly to maintenance requests, follow through on promises made during tours, and prioritize tenant satisfaction right from the start. Satisfied tenants are more likely to renew their leases, recommend your property to others, and leave positive reviews - helping you cut down on future marketing costs and vacancy rates. These efforts reinforce your overall strategy for success.

A well-thought-out plan ensures you move efficiently from construction completion to stabilized occupancy, delivering the returns you’ve planned for.

FAQs

How long does a lease-up take in Nova Scotia?

In Nova Scotia, the process from the start of construction to full occupancy for a rental property generally takes between 38 and 54 weeks. This timeline accounts for several crucial steps, including acquiring the land, planning the project, securing permits, completing construction, and undergoing final inspections.

How do I price rents without guessing?

Setting rental prices requires a careful balance of market research and adherence to regulations. Start by analysing local rental data, focusing on units similar in size, amenities, and condition to your property. This will give you a realistic range for competitive pricing.

In Nova Scotia, keep in mind the province’s rent cap regulations, which restrict annual rent increases to 5% until December 31, 2027. Staying compliant is non-negotiable, so build this into your pricing strategy.

To avoid relying on guesswork, explore multiple sources for data. Market reports, conversations with real estate professionals, and online rental listings can all provide valuable insights into current trends. This approach ensures your rates are both fair and attractive to potential tenants.

What should I do if leasing is slow after opening?

If leasing slows down after opening, it’s crucial to adopt a clear lease-up strategy. Start by actively marketing the property both before and after completion. Use tools like virtual tours and targeted advertising to reach potential tenants effectively. Establish clear occupancy targets and keep an eye on local rental trends. If necessary, adjust rents or consider offering incentives to attract tenants.

In Nova Scotia, remember to comply with rent control regulations, including the 5% rent cap in place until December 2027. Staying within these rules ensures you remain competitive while avoiding potential penalties.