The Compounding Advantage: How One Build Becomes a Rental Portfolio

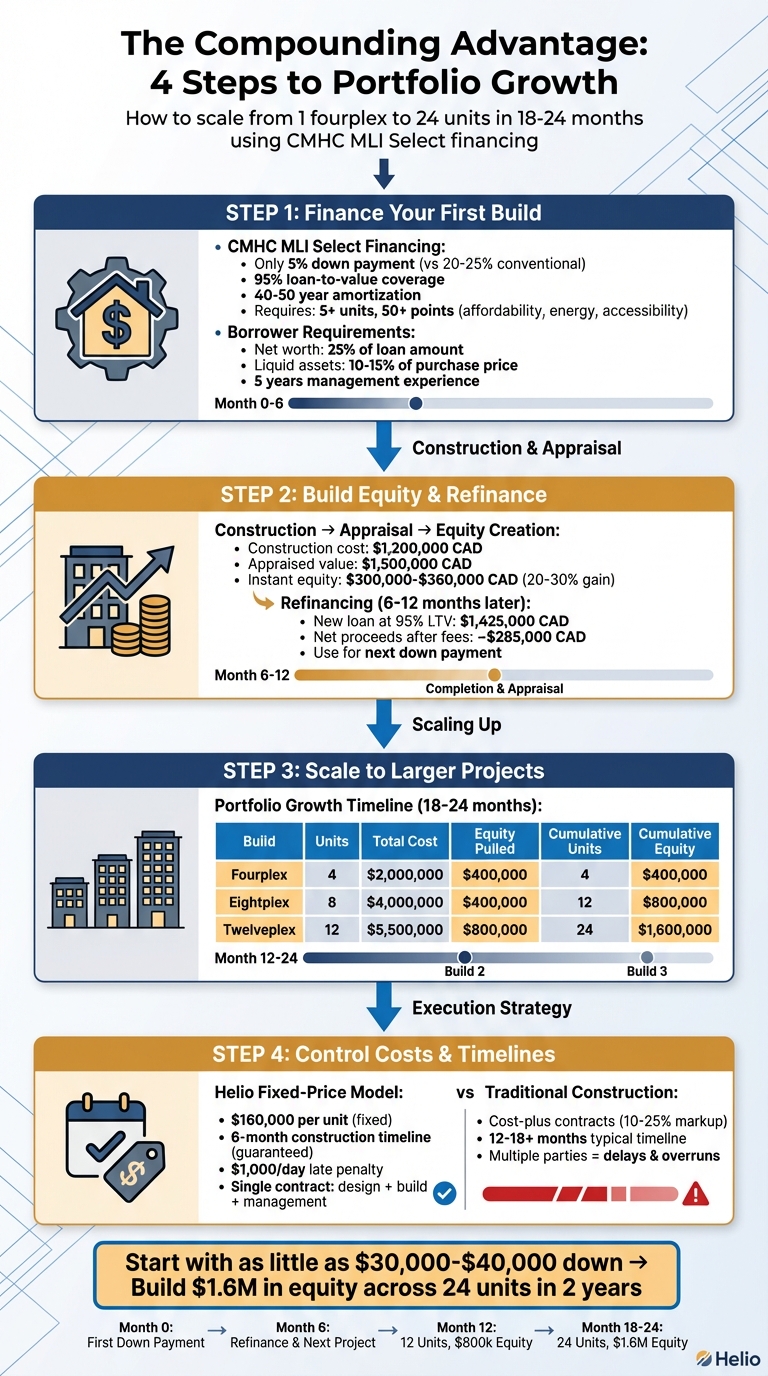

If you're trying to figure out how to turn one rental property into a growing portfolio, you're likely asking: how do I fund the next project without draining my savings? In Nova Scotia, where rental demand is high - especially in areas like Halifax - building a fourplex can create immediate equity you can use to scale. The key is using CMHC MLI Select financing, which allows you to start with as little as 5% down and refinance after completion. This article breaks down how one project can set the stage for steady portfolio growth, using real numbers and timelines to show what's possible.

4-Step Portfolio Growth Strategy: From One Fourplex to 24 Units in 24 Months

5 Ways to Scale Your Portfolio FAST (with Just 1 Rental Property!)

sbb-itb-16b8a48

Step 1: Using CMHC MLI Select to Finance Your First Build

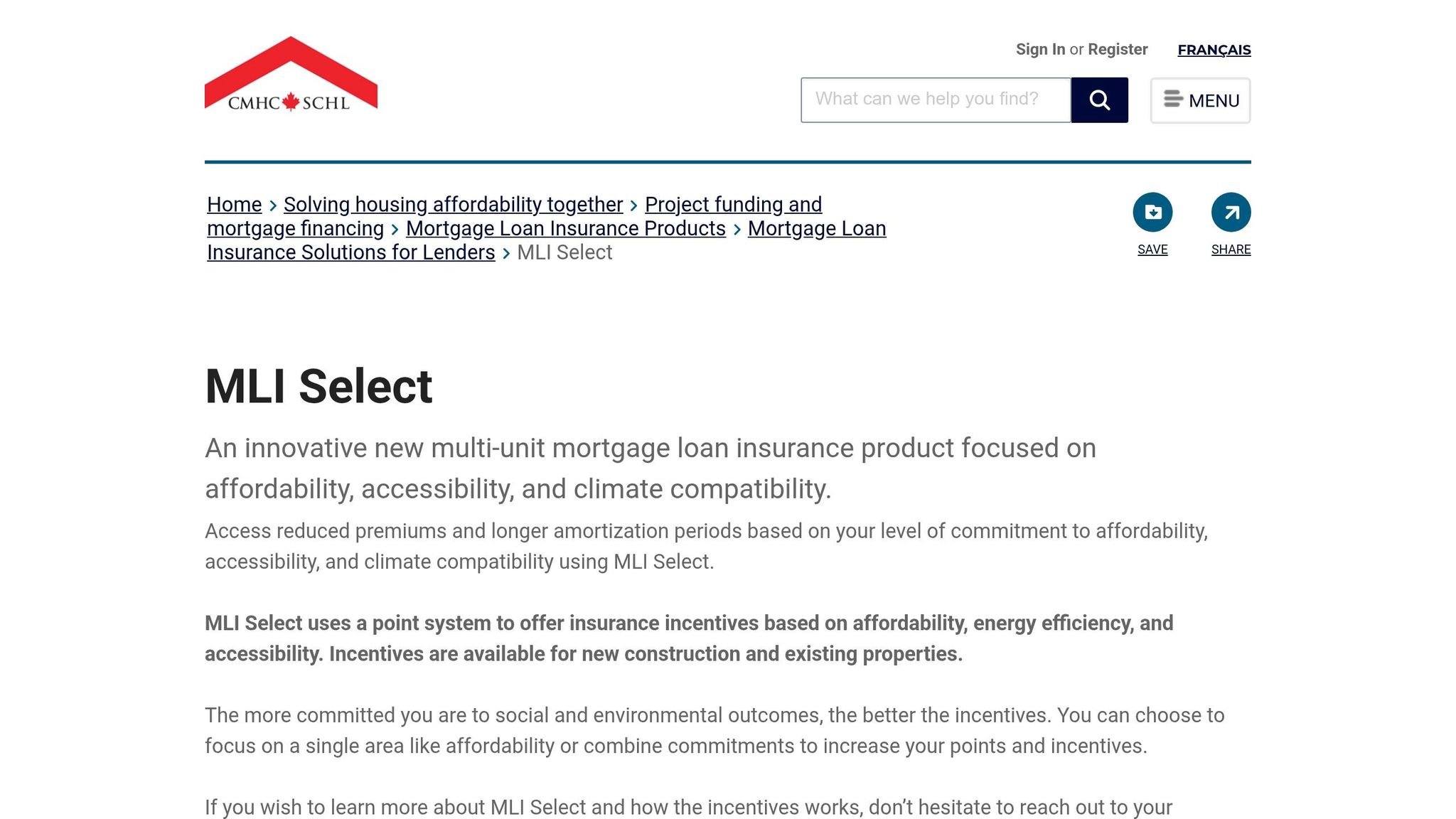

The CMHC MLI Select program is a game-changer for first-time builders, offering financing with just a 5% down payment and loan amortization periods of up to 50 years. This structure lowers upfront capital requirements and reduces monthly debt payments compared to conventional loans, which typically demand a 20–25% down payment and offer amortization over only 25–30 years. By easing these financial pressures, MLI Select leaves more room for future projects and ensures your first build achieves positive cash flow right out of the gate.

CMHC MLI Select Requirements

To qualify, your project must include at least 5 rental units and score a minimum of 50 points across three categories: affordability, energy efficiency, and accessibility [3][4]. For energy efficiency, your building needs to exceed the National Building Code 2020 baseline by 25%. Accessibility features, certified by organizations like the Rick Hansen Foundation, also contribute to the score [3]. Achieving 50 points unlocks financing at 95% loan-to-value and a 40-year amortization, while reaching 100 points extends the amortization to 50 years [6].

Applications require signed attestations from professionals such as a Professional Engineer or Certified Energy Manager to validate your energy and accessibility commitments [3]. These conditions make MLI Select especially appealing when compared to conventional financing options.

CMHC MLI Select vs Conventional Financing

Under MLI Select, you can finance up to 95% of construction costs with just a 5% down payment, compared to the 20–25% required by conventional lenders [6]. Amortization periods of 40–50 years further reduce monthly payments, making it easier to scale your portfolio. The program’s popularity is evident - over 127,000 rental units were insured through MLI Select in 2023 alone [6].

Nova Scotia’s rental market aligns well with the program’s requirements. A minimum debt coverage ratio of 1.10 is achievable thanks to high demand and CMHC’s 2026 rent increase cap of 4.7% [3]. These factors make MLI Select a reliable choice for developers in the region.

Borrower Qualification Requirements

To qualify as a borrower, you’ll need to meet specific financial thresholds. Your net worth must be at least 25% of the requested loan amount, and you’ll need 10–15% of the purchase price in liquid assets separate from your down payment [6]. Experience matters too - you or your affiliated corporation must have at least five years of management experience with similar multi-unit residential properties [6].

A comprehensive financial package is also required, including three years of tax returns, bank statements, a detailed equity breakdown of your existing real estate holdings, and cash flow projections for the new property [5][6]. Keep in mind that non-residential spaces, such as commercial units, cannot exceed 30% of the gross floor area or total lending value [6][3].

These borrower requirements may seem rigorous, but they ensure you’re well-prepared to manage the financial and operational demands of your first build.

Step 2: Using Equity from Your Completed Build

Once your multi-unit property is built, fully rented, and generating income, the equity it holds becomes a powerful tool for funding your next project. Refinancing allows you to access this equity, enabling you to grow your portfolio without injecting fresh capital. Here's how final appraisals contribute to this process.

How Appraised Value Creates Instant Equity

After construction wraps up, your property undergoes a final appraisal. Typically, the appraised value exceeds your total construction costs by 20–30%. For instance, if you build a fourplex for $1,200,000 CAD (or $300,000 CAD per unit), it might appraise at $1,500,000–$1,560,000 CAD[2]. This difference arises because appraisers factor in market rents, location, and income potential - not just what it cost to build.

Canada Mortgage and Housing Corporation (CMHC) underwriting standards, such as maintaining a minimum debt coverage ratio of 1.1, further support this valuation. If your actual rents align with or surpass projections, the property's net operating income pushes its appraised value above your construction expenses.

Why this matters: You're not just constructing a rental property - you're creating $300,000–$360,000 CAD in equity right off the bat. This equity becomes the foundation for refinancing, helping you fund your next project and expand your portfolio[2].

Refinancing to Access Your Equity

Refinancing typically happens 6–12 months after construction, once your property has stabilized with full tenancy[1][7]. Here’s an example of how this works:

- Original loan: You take out a $1,140,000 CAD MLI Select loan, which covers 95% of the $1,200,000 CAD construction cost.

- Appraised value: Your property appraises at $1,500,000 CAD.

- New loan: Refinancing at 95% loan-to-value gives you a new loan of $1,425,000 CAD.

- Net proceeds: After paying off the original loan and accounting for 1–2% in fees, you walk away with approximately $285,000 CAD.

This $285,000 CAD can then be used as the down payment for your next property. Keep in mind that to qualify for refinancing, you’ll need a net worth equal to at least 25% of the new loan amount - around $350,000 CAD in this case - as well as a solid track record in rental property management and compliance with CMHC’s affordability and accessibility guidelines[2].

Step 3: Building Your Second and Third Properties

With $400,000 CAD in equity from your initial fourplex, you're now in a position to scale up. This is where you can transition from a fourplex to larger projects like an eightplex or even a twelveplex. Let’s break this down with a practical example.

Example: From Fourplex to Eightplex

Imagine your fourplex was purchased for $2,000,000 CAD (about $500,000 per unit) and appraises at $2,200,000 CAD after completion. This gives you $400,000 CAD in equity to work with.

Now, consider an eightplex. If the cost per unit remains $500,000, the total project cost is $4,000,000 CAD. With CMHC MLI Select financing covering up to 95% of the cost, your required down payment is only about $200,000 CAD - well within the equity you’ve already built. Once the eightplex is completed and stabilized, you can refinance it, pulling out more equity to fund your next project, such as a twelveplex. This method allows you to grow your portfolio systematically.

Portfolio Growth Numbers

Here’s how this strategy plays out over 18–24 months, showing how unit count and equity can compound:

| Build | Units | Total Cost | Equity Pulled | Cumulative Units | Cumulative Equity |

|---|---|---|---|---|---|

| Fourplex | 4 | $2,000,000 | $400,000 | 4 | $400,000 |

| Eightplex | 8 | $4,000,000 | $400,000 | 12 | $800,000 |

| Twelveplex | 12 | $5,500,000 | $800,000 | 24 | $1,600,000 |

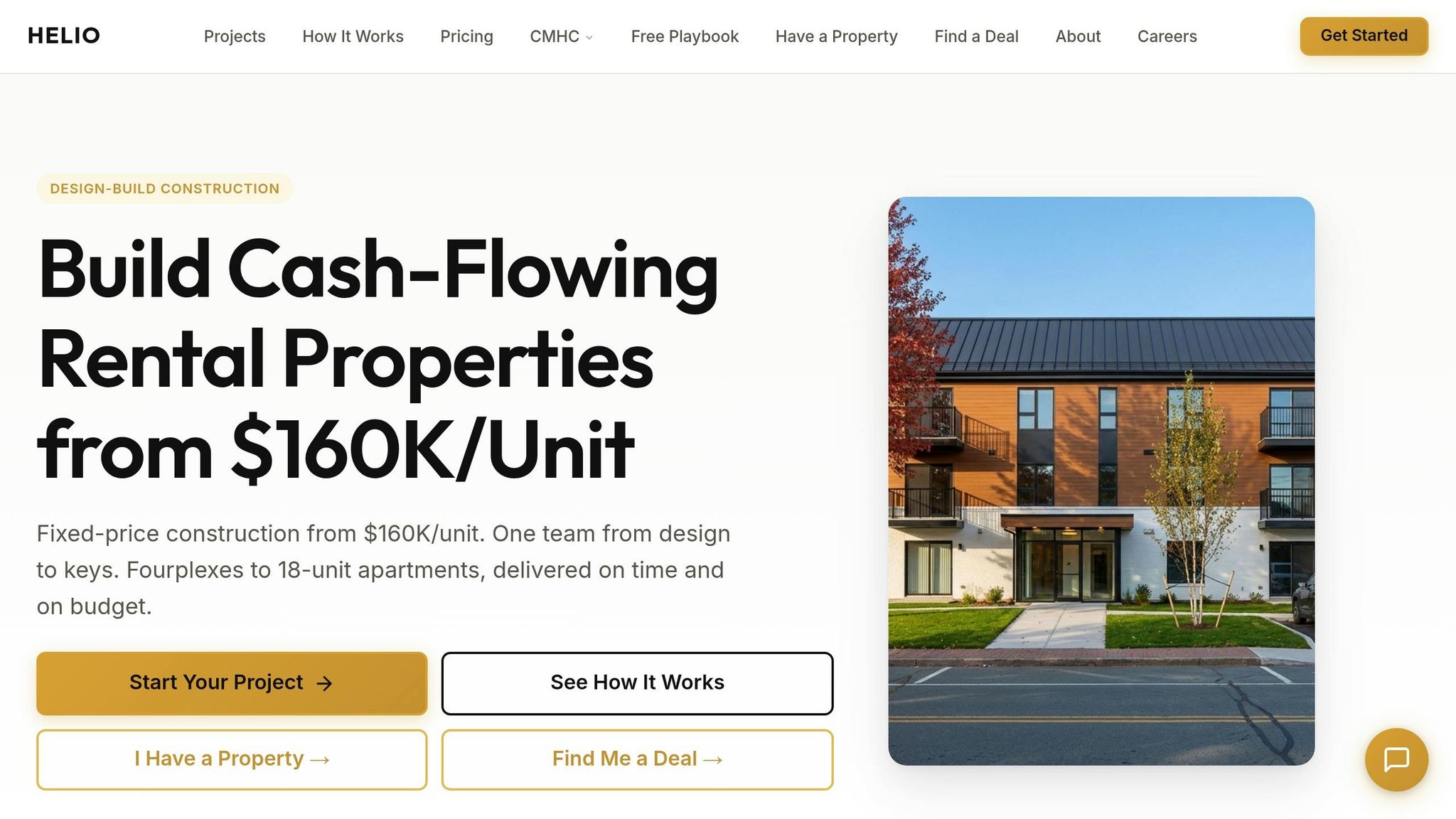

Step 4: Why Helio's Fixed-Price Model Makes Scaling Easier

When you're using equity from finished projects to fund new builds, keeping construction costs and timelines under control is non-negotiable. Scaling a portfolio relies on having predictable numbers - both in terms of cost and project delivery. Traditional construction models often lack this predictability, but Helio's integrated design-build approach is built to address these challenges head-on.

Avoiding Cost Overruns and Delays

In traditional construction, coordinating multiple parties - each with their own margins - frequently leads to cost overruns and delays. This not only eats into your profits but also disrupts your refinancing schedule, slowing down portfolio growth. Cost-plus contracts, where you're billed for actual costs plus a fee (usually 10% to 25% of the project total) [8][9], make it even harder to forecast expenses. Even minor overruns can derail your timelines and refinancing plans [10].

Helio simplifies this by rolling architecture, structural engineering, construction, and project management into one fixed-price contract. At $160,000 per unit, you know exactly what your project will cost before breaking ground. For example, if you're building an eightplex, the total cost is locked at $1,280,000. No surprises, no unexpected hikes. This level of cost certainty eliminates the headaches of traditional models, allowing you to focus on scaling efficiently.

Fixed Pricing and 6-Month Timelines

Helio also guarantees a six-month construction timeline - from building permit to handing over the keys. This timeline is backed by strict penalties for delays, ensuring accountability. With over 40 units already delivered in Nova Scotia and 130 more in the pipeline, this model has proven its reliability. Pre-approved designs, well-coordinated trades, and aligned incentives ensure projects stay on track.

This kind of predictability is a game-changer for scaling. Picture this: you complete a fourplex in six months, stabilize it for another six months to refinance, and then move on to an eightplex - all within 18 months. Compare that to traditional construction, where a single project might still be under construction after 12–18 months, or even longer if delays pile up. Over a 24-month period, Helio's model could result in far more completed units, giving you a significant edge in building equity for future projects. By controlling both costs and timelines, Helio creates a streamlined process that accelerates your portfolio's growth.

Conclusion

Building a rental portfolio is all about strategy - each project should set the stage for the next. Starting with a fourplex financed through CMHC MLI Select is a smart move. With 95% loan-to-value financing, you can get started with as little as $30,000–$40,000 down. Once the property is complete and stabilized, the equity you’ve built becomes the foundation for your next project. Every new build adds more equity, creating a cycle that fuels ongoing growth.

The success of this approach hinges on controlling costs and timelines. Traditional construction methods often come with unpredictable expenses and delays, which can throw off your refinancing plans and slow portfolio growth. Helio’s integrated design-build model removes these uncertainties. With fixed pricing at $160,000 per unit and a six-month construction timeline, plus a $1,000/day late penalty written into the contract [11], you gain the predictability needed to plan your next steps with confidence. You’ll know exactly when you can refinance and move forward.

This approach has resonated with investors.

Mark Thompson from Truro shared: "As a first-time investor, having one team handle everything from design to occupancy was the difference between moving forward and staying stuck in hesitation" [11].

Whether you’re building your first fourplex or scaling up to an eightplex, Helio’s model is tailored for Nova Scotia property owners looking to grow their rental portfolios efficiently - one project at a time.

With the right financing structure and a construction partner that sticks to both budget and schedule, you can scale your portfolio steadily, building equity that compounds into long-term wealth.

FAQs

Can I use MLI Select if I’m building only 4 units?

Yes, the CMHC MLI Select financing program is available for a 4-unit build, like a 4-plex in Halifax. This program is designed to support small-scale rental property projects and can help ensure positive cash flow, making it an attractive option for property owners.

How soon after completion can I refinance to pull equity out?

Refinancing can usually be done soon after the property is finished and stabilized, provided its updated value has been appraised. Certain programs may allow refinancing up to 90% of the property's appraised value. However, the exact timing will hinge on the lender's criteria and whether the property is ready for a formal appraisal.

What could prevent my refinance from being approved?

Refinancing can hit a roadblock if your project doesn't align with lender requirements. Common issues include insufficient market demand, unrealistic budgets, or poorly developed property management plans. Additionally, failing to meet specific program standards, such as the energy efficiency and affordability benchmarks set by CMHC's MLI Select, can result in rejection.

Other factors that may jeopardize approval include construction delays, cost overruns, or inaccurate rental income projections. These elements signal higher risks to lenders, which can make them hesitant to move forward.