Understanding Cash Flow vs. Equity Growth in Rental Construction

What’s more important: monthly income or long-term wealth? If you’re building multi-unit rentals in Nova Scotia, that’s the question you’re likely grappling with. On one hand, cash flow gives you immediate returns - covering your mortgage, taxes, and maintenance. On the other, equity growth builds wealth over time through property appreciation and mortgage paydown.

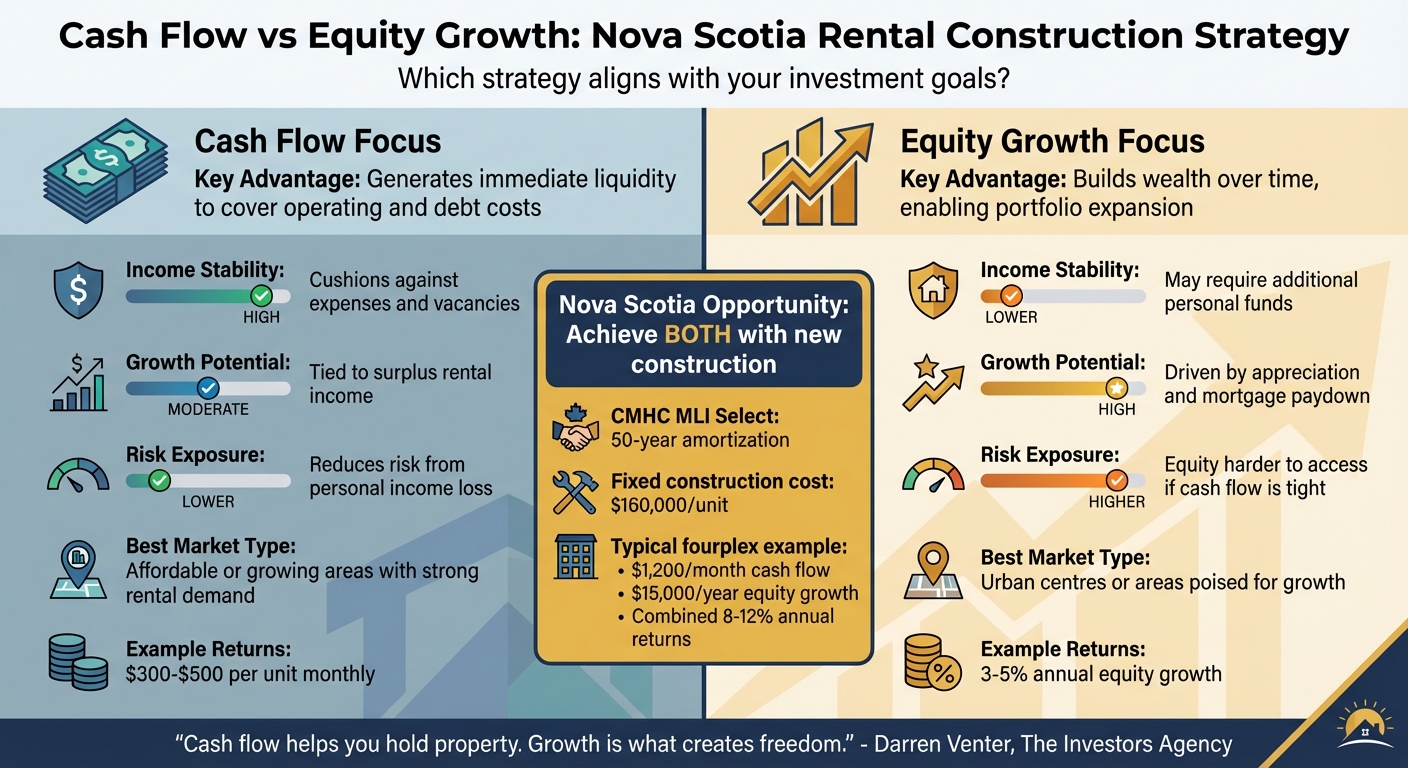

Here’s the reality: Nova Scotia’s rental market offers both opportunities. With property prices lower than Toronto or Vancouver, you can achieve 8–12% annual returns. A typical fourplex near Halifax might generate $1,200/month in cash flow while building $15,000/year in equity through 4% appreciation and principal reduction. This article breaks down how to balance these priorities and structure your project for the best outcome.

Cash Flow vs. Equity & How Much Money Do You NEED To Invest?

sbb-itb-16b8a48

1. Cash Flow in Rental Construction

Cash flow represents the net income left after covering operating expenses such as mortgage payments, property taxes, insurance, maintenance, and utilities. For multi-unit rental construction, this surplus determines whether the property starts generating income immediately or requires additional funding to stay afloat.

Income Source

The primary driver of cash flow is rental income. In Nova Scotia, new two-bedroom units typically rent for $1,950 to $2,100 per month. Short-term rentals can bring in roughly 30% more revenue [1]. Targeting specific groups like healthcare workers or students and offering premium features - such as parking, in-unit laundry, or smart home technology - can further increase rental income. Adding secondary or backyard suites also boosts cash flow, especially with the provincial incentive that offers up to $40,000 in forgivable loans for such projects.

Timeline

Using an integrated design-build approach, multi-unit properties can be completed in about six months, allowing rental income to start sooner. Financing through CMHC's MLI Select program, which offers 95% loan-to-value and a 50-year amortization, can reduce monthly mortgage payments. Even with construction costs averaging $160,000 per unit, this setup often results in positive cash flow.

Risk Factors

Income gaps caused by vacancies or tenant turnover are a common risk. Setting aside 5% of gross rental income to cover these gaps is a prudent move [4]. Other risks include unexpected maintenance costs, rising property taxes, increasing insurance premiums, and fluctuating mortgage rates. To emphasize the importance of liquidity, Andrew Syrios points out:

Cash is liquid money and is absolutely essential when you finance real estate... whereas equity is completely useless [if you need money quickly].

To safeguard against these risks, it's wise to maintain cash reserves equivalent to 3–6 months of mortgage payments.

Tax Implications

Rental income is taxable, but landlords can offset this by deducting expenses like mortgage interest, property taxes, insurance, and maintenance costs using Form T776. Additionally, Nova Scotia's decision to remove the provincial portion of the HST on new rental housing reduces construction costs, improving the initial cash flow outlook. Up next, we’ll look at how property appreciation and debt reduction contribute to building equity.

2. Equity Growth in Rental Construction

Cash flow might give you immediate returns, but equity growth is where long-term wealth is built.

Equity growth refers to the increase in your ownership stake in a property over time. Unlike cash flow, which puts money in your pocket monthly, equity builds wealth through property appreciation and paying down your mortgage principal. In Nova Scotia, multi-unit rental properties have appreciated at an average annual rate of 6.8% between 2015 and 2023. Halifax saw even stronger growth, with values climbing about 12% year-over-year in 2023 [5]. To put this into perspective, a $1,200,000 triplex could see its market value rise by approximately $144,000 in just one year.

Income Source

Equity becomes accessible only when you sell or refinance the property. It grows in two ways: market appreciation, which depends on economic conditions, and principal paydown, which happens automatically with regular mortgage payments. For example, on a $500,000 property with 75% financing at a 4% interest rate, you’d reduce the principal by about $8,500 in the first year. If the property appreciates at 5% annually, its market value could increase by roughly $25,000 in that same timeframe.

Timeline

Equity growth is a steady, predictable process tied to your mortgage term. Early on, a significant portion of your equity will come from reducing the mortgage balance - roughly 30–50% for a $500,000 property with 75% financing and a 5% appreciation rate. Over time, appreciation takes the lead in driving equity gains.

Risk Factors

Equity isn’t immune to risks. Market downturns can temporarily reduce property values, as happened in Nova Scotia with a 2% dip in 2022 before the market rebounded. Rising interest rates can slow debt reduction and make refinancing more expensive. Construction cost overruns can also eat into your initial equity, making fixed-price contracts a smart move. To reduce risk, aim for conservative loan-to-value ratios (ideally 65% or lower) and opt for fixed-rate mortgages. Additionally, while policies like Nova Scotia's Residential Tenancies Act - capping rent increases at 3.8% in 2026 - help stabilize property values, they can limit strategies for accelerating appreciation.

Tax Implications

Principal paydown isn’t taxed, but appreciation is. When you sell, half of the property’s gain is taxed as income under capital gains rules, with provincial rates in Nova Scotia reaching up to 21%. If you’ve claimed capital cost allowance (CCA) for depreciation, that amount is recaptured and taxed as regular income, potentially reducing your net equity by 5–15%. For example, selling a $1,000,000 property with a $300,000 net gain - after $100,000 in capital improvements - could result in about $100,000 of taxable income after the 50% inclusion rule. Since rental properties don’t qualify for the principal residence exemption, it’s crucial to consult a Nova Scotia tax advisor to plan for these costs and calculate your true returns.

Equity growth is a cornerstone of long-term investment strategy, but it requires careful planning to manage risks and maximize returns.

Comparing Cash Flow and Equity Growth

Cash Flow vs Equity Growth in Nova Scotia Rental Construction

When weighing cash flow against equity growth, the choice comes down to your investment timeline and financial priorities. The crux of the decision is this: cash flow ensures liquidity now, while equity growth builds wealth over time. As Darren Venter from The Investors Agency explains:

Cash flow helps you hold property. Growth is what creates freedom [2].

In Nova Scotia's rental construction market, it's not about picking one over the other. Instead, it's about deciding where to focus based on your goals and current financial position.

| Factor | Cash Flow Focus | Equity Growth Focus |

|---|---|---|

| Key Advantage | Generates immediate liquidity to cover operating and debt costs | Builds wealth over time, enabling portfolio expansion |

| Income Stability | High; cushions against expenses and vacancies [2][3] | Lower; may require additional personal funds [2] |

| Growth Potential | Moderate; tied to surplus rental income [2] | High; driven by appreciation and mortgage paydown |

| Risk Exposure | Lower; reduces risk from personal income loss [3] | Higher; equity can be harder to access if cash flow is tight [3] |

| Market Type | Affordable or growing areas with strong rental demand | Urban centres or areas poised for growth [2][4] |

This breakdown highlights the trade-offs between the two approaches. By understanding these dynamics, you can better align Helio's design-build process with your financial strategy.

In Nova Scotia, new construction offers the potential for both cash flow and equity growth, especially when leveraging CMHC MLI Select financing with its 50-year amortization. This setup often allows for immediate positive cash flow while capturing long-term equity gains through appreciation and principal reduction. Building within a 90-minute radius of Halifax is a smart move - lower land costs combine with solid urban rental demand. With Helio's fixed-price construction at $160,000 per unit, you can forecast cash flow and equity outcomes before starting, minimizing risks and maximizing returns.

Conclusion

Balancing cash flow with equity growth is the cornerstone of maximizing returns in Nova Scotia rental construction. Cash flow provides the monthly income needed to manage the property and handle vacancies, while equity growth builds long-term wealth for financial independence. The most successful property owners don’t pick one over the other - they structure their projects to achieve both.

In today’s Nova Scotia market, new construction offers a unique opportunity to align these goals. With CMHC MLI Select financing offering 50-year amortizations and Helio’s fixed-price construction costs of $160,000 per unit, you can accurately forecast both cash flow and equity growth before breaking ground. For instance, a typical fourplex located within 90 minutes of Halifax might generate $1,200 in monthly cash flow while building $15,000 in annual equity through principal paydown and 4% appreciation. These combined returns outperform relying solely on a single strategy.

Your investment timeline will influence whether you lean more towards cash flow or equity, but your construction approach is what ensures you can achieve both. An integrated design-build process reduces the risk of cost overruns and delays, which safeguards your cash flow. At the same time, energy-efficient designs help lower operational costs, protecting your monthly income. A guaranteed 6-month construction timeline means quicker rent collection and faster equity accumulation compared to traditional contractor timelines.

Use Nova Scotia benchmarks - $300–$500 per unit in monthly cash flow and 3–5% annual equity growth - to calculate your return targets. From there, identify the right property type, location, and financing structure to match your goals. Whether your focus is immediate income or long-term wealth, the numbers will steer your decisions - and new construction gives you the control to achieve both.

FAQs

How do I know if I should prioritize cash flow or equity growth?

Your choice should align with your financial goals and how much risk you’re comfortable taking. If your priority is cash flow, you’ll want properties that generate enough rental income to cover expenses and mortgage payments, providing a steady monthly return. On the other hand, focusing on equity growth means aiming for long-term gains through property value appreciation and gradually paying down debt.

In Nova Scotia, many investors aim to start with positive cash flow to ensure stability, while still benefiting from equity growth as the property appreciates over time. The right approach depends on what fits your overall financial plan.

How much cash reserve should I keep for a new multi-unit rental?

When planning a new multi-unit rental project in Nova Scotia, it's wise to allocate a cash reserve equal to 10–15% of the total project cost. For a $1.5 million build, this works out to roughly $150,000–$225,000. This reserve acts as a financial buffer, covering unexpected expenses, possible delays, or early operational costs. It ensures you can maintain stability during construction and the initial phase of operations before rental income starts flowing consistently.

How can I pull equity out without selling the property?

To tap into your home equity without selling, you might look at refinancing or a home equity line of credit (HELOC). Refinancing involves replacing your existing mortgage with a larger one, allowing you to access the difference in cash. On the other hand, a HELOC works like a revolving credit line, secured by the equity in your property. Both options typically require a property appraisal and lender approval. It’s wise to consult a financial advisor to figure out which option suits your specific needs in Nova Scotia.