Using Equity from Your Existing Property to Fund a New Rental Build

If you're a property owner in Nova Scotia, you might be wondering how to turn your home equity into a tool for building income-generating rentals. With Halifax's average home price hitting $550,000 in 2025 and vacancy rates below 1%, demand for rental units is high. Here's the math: if your home is worth $600,000 and you owe $300,000, you have $300,000 in equity. Lenders typically allow you to borrow up to 80% of that, or $240,000. That’s enough for a down payment on a $1.2 million four- to six-unit rental property. This article breaks down how to calculate your equity, access it through HELOCs or refinancing, and pair it with CMHC MLI Select financing to start your rental build.

How Home Equity Works and How Much You Can Borrow

What is Home Equity?

Home equity is the gap between your property's current market value and the remaining balance on your mortgage. For example, if your Halifax home is valued at $550,000 and you owe $200,000 on your mortgage, your equity is $350,000. This equity increases as you pay down your mortgage and as your property value rises.

Calculating Your Available Equity

In Canada, federal regulations allow you to borrow up to 80% of your home's appraised value. To figure out how much equity you can access, multiply your property's value by 80% and subtract your remaining mortgage balance. For instance, if your property is appraised at $620,000, the maximum borrowing limit would be $496,000 (80% of $620,000). If you owe $300,000 on your mortgage, you could potentially access $196,000 in equity.

Different financing products have their own borrowing limits. For example:

- Home Equity Lines of Credit (HELOCs): Typically capped at 65% of your home's appraised value. For a $600,000 property, this means a HELOC would allow borrowing up to $390,000. After subtracting a $300,000 mortgage, you'd have $90,000 available.

- Home Equity Loans or Cash-Out Refinancing: These can let you borrow up to the full 80% limit. Using the same $600,000 property, this would mean accessing $480,000, leaving $180,000 after subtracting the $300,000 mortgage.

Why this matters for property owners: Before pursuing equity financing, getting a professional appraisal is crucial. Your equity depends on the current market value, not the original purchase price. In a city like Halifax, where property values are climbing, many homeowners find they have more equity than expected. This can open up opportunities to fund projects like rental builds. Knowing these borrowing limits ensures you pick the right financing tool for your goals.

sbb-itb-16b8a48

How to Get a HELOC on Investment Property (Use Your Equity!)

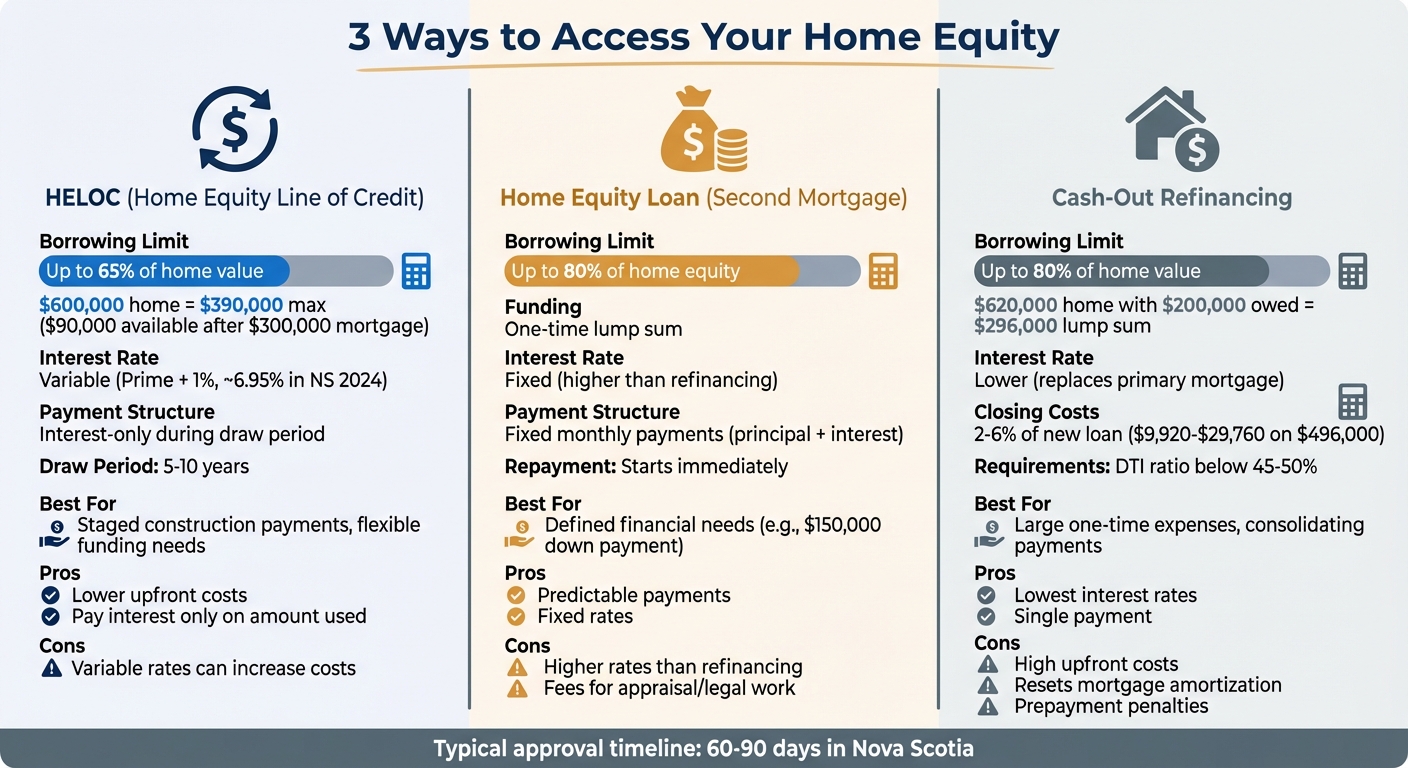

3 Ways to Access Your Home Equity

3 Ways to Access Home Equity for Rental Property Investment in Nova Scotia

When planning a rental construction project in Nova Scotia, tapping into your home equity can provide the funding you need. Each option comes with its own structure, costs, and repayment terms, so choosing the right one depends on your specific project and financial situation.

Home Equity Line of Credit (HELOC)

A HELOC functions like a revolving credit line, secured by your home. You’ll be approved for a maximum credit limit - up to 65% of your home’s lending value - and can borrow, repay, and borrow again during a draw period, typically lasting 5–10 years. As Academy Bank explains:

A HELOC is a revolving line of credit that allows you to borrow against your home's equity... you can borrow, repay, and borrow again up to your limit during the 'draw period' [6].

This makes HELOCs particularly useful for construction projects, where expenses often come in phases. For instance, you can withdraw funds as needed to match key project milestones.

However, keep in mind that HELOCs usually come with variable interest rates tied to the lender's prime rate (e.g., Prime + 1%). If rates go up, your borrowing costs will rise as well. In Canada, lenders cap HELOCs at 65% of your home’s value and require you to maintain at least 20% equity [7][8]. While upfront costs are lower than refinancing - some lenders even waive application fees - this option is best for projects with uncertain or staggered funding needs.

Home Equity Loan (Second Mortgage)

A home equity loan provides a one-time lump sum with a fixed repayment schedule, separate from your existing mortgage. Unlike a HELOC, you receive all funds upfront and start repaying both principal and interest immediately. Ramsey Solutions explains:

The home equity loan allows you to borrow one lump sum of your equity, while a HELOC lets you borrow multiple sums of your equity at a time - like using a credit card [5].

You can borrow up to 80% of your home’s equity, and the fixed interest rates ensure predictable monthly payments. However, these rates are typically higher than those offered through cash-out refinancing. Lenders will evaluate your credit score, income, and debt-to-income ratio, and you’ll incur fees for appraisals, legal work, title searches, and insurance.

This option works well if you have a defined financial need - such as a $150,000 down payment on a multi-unit property in Halifax - and prefer the stability of fixed repayments. If lower interest rates are a priority, you might want to explore cash-out refinancing instead.

Cash-Out Refinancing

With cash-out refinancing, you replace your current mortgage with a new, larger loan based on up to 80% of your home’s current value. The difference between the new loan and your remaining mortgage balance is given to you as a lump sum. For example, if your Halifax home is valued at $620,000 and you owe $200,000, refinancing up to 80% of the value would provide a lump sum of about $296,000.

This option often comes with lower interest rates since it replaces your primary mortgage, but closing costs typically range from 2% to 6% of the new loan amount. On a $496,000 refinance, this means upfront costs of $9,920 to $29,760. You’ll likely need a new appraisal and may face prepayment penalties on your existing mortgage. Most lenders also require a debt-to-income ratio below 45% to 50%.

Cash-out refinancing is a good fit if current mortgage rates are better than what you’re paying now or if you want to consolidate your payments into one. It’s ideal for covering large, one-time expenses like major construction costs.

Each of these methods has its strengths, so consider your project’s timeline and cash flow needs before making a decision.

Combining Equity with CMHC MLI Select Financing

By tapping into your home equity and pairing it with CMHC MLI Select financing, you can significantly reduce the upfront cash needed for building a multi-unit rental property. This approach is particularly effective in Nova Scotia, where constructing a fourplex typically costs between $640,000 and $1,000,000.

What CMHC MLI Select Offers

CMHC MLI Select provides up to 95% loan-to-value (LTV) financing for multi-unit rental projects that meet specific criteria for energy efficiency and affordability. This means you only need to cover 5% of the total project cost as a down payment, compared to the 20-35% typically required with conventional financing. For example, on a $640,000 fourplex, the down payment would be just $32,000 instead of $128,000 to $224,000.

The program also includes lower insurance premiums and extended amortization periods - up to 50 years for projects scoring 50+ points under CMHC's sustainability criteria. Eligibility depends on factors such as energy performance, accessibility features, and affordability commitments. With Helio's standard designs pre-qualified for MLI Select, you can skip the uncertainty of meeting CMHC's requirements.

Using Equity to Meet CMHC Down Payment Requirements

Here’s how equity plays into this strategy: Imagine you own a home in Halifax valued at $500,000 with a $200,000 mortgage balance. By using a HELOC at 65% of your home’s value, you could access up to $125,000 in equity. If you’re planning to build a $960,000 sixplex that qualifies for CMHC MLI Select, the required down payment would be $48,000 (5% of the project cost). You could draw $48,000 from your HELOC to cover the down payment, while CMHC-backed financing would fund the remaining $912,000.

This method allows you to turn unused equity into a down payment, securing 95% financing for a new income-generating property. Under traditional financing, you’d need $192,000 to $336,000 in cash - amounts that often exceed what most property owners can access through equity alone.

How to Finance and Start Your Rental Build

Assess Your Equity and Choose Your Financing Method

The first step in financing your rental build is understanding your current equity. Get a professional appraisal for your property, which typically costs around CAD$500. From there, subtract your outstanding mortgage balance to calculate your usable equity. For example, if your property is worth CAD$500,000 and you owe CAD$200,000 on your mortgage, you have CAD$300,000 in equity. Of this, up to 65% - around CAD$125,000 - might be accessible through a home equity line of credit (HELOC).

When evaluating financing options, consider your project timeline and cash flow needs:

- HELOC: With an interest rate of about 6.95% in Nova Scotia as of 2024, this is a good choice for staged construction payments since you only pay interest on the amount you use.

- Home Equity Loan: Offers a lump sum with fixed payments, which is useful if you need the entire down payment upfront.

- Cash-Out Refinancing: This can lower your overall interest rate but resets your mortgage amortization, which could extend the time it takes to pay off your home.

Before approaching lenders, prepare all necessary documents: property appraisal, mortgage statements, tax returns for the last two years, pay stubs, and a summary of your debts. For rental builds, lenders will also require a construction timeline, a detailed project budget, and architectural plans. Having this package ready can speed up approvals, which typically take 60 to 90 days in Nova Scotia from the initial equity assessment to the start of construction.

By carefully selecting the right financing method and assembling your documents early, you can reduce your interest costs and align your funding with your construction schedule. If you're using CMHC MLI Select financing, you can further lower upfront cash requirements, freeing up equity for contingencies. Once financing is locked in, the focus shifts to executing the project efficiently.

Work with an Integrated Design-Build Firm

After securing financing, the next critical step is ensuring the project stays on budget and on schedule. This is where an integrated design-build firm can make all the difference. In Atlantic Canada, traditional construction projects often run 30% over budget due to poor coordination between separate architects, engineers, and contractors. A design-build firm eliminates this chaos by combining all disciplines under one contract and offering fixed pricing, keeping cost overruns below 5%.

This fixed-price approach is especially important when financing through home equity. It allows you to accurately predict your total project costs and align your equity draws to match. For example, Helio's standard fourplex design costs CAD$640,000 (or CAD$160,000 per unit), which is 10% lower than CMHC's benchmark pricing. Helio also includes a contractual CAD$1,000/day penalty if the six-month construction timeline is exceeded.

With CMHC MLI Select pre-qualified designs, you can secure up to 95% financing, using your equity only for the 5% down payment - about CAD$32,000 for a fourplex. This approach preserves the rest of your equity for contingencies, ensuring you’re not stretched thin during the build. By choosing a design-build firm, you not only save time and money but also gain the predictability needed to make your rental project a success.

What This Means for Your Property Investment

When you combine a solid financing strategy with a design-build approach, you’re setting the stage for faster returns on your property investment. By using home equity, you can turn underutilized assets into a steady income stream. Take a Nova Scotia homeowner as an example: they accessed $250,000 in equity to finance a $1.25 million triplex through CMHC MLI Select. This triplex could generate approximately $5,500 in monthly rental income while also benefiting from 6–8% annual appreciation. That translates to an additional $120,000–$160,000 in equity growth every year [1][2]. This surge in rental income doesn’t just boost your cash flow - it lays the groundwork for building a larger portfolio.

By pairing your equity with CMHC MLI Select, you can take on larger projects - like a sixplex built using fixed-price models - while keeping debt manageable and cash flow strong. Instead of being restricted to smaller investments, this approach lets you pursue well-priced, pre-qualified designs, preserving equity for future projects.

What this means for property owners: You’re creating a system that builds wealth over time. The rental income generated can cover your debt payments while your properties appreciate in value. Meanwhile, the equity you’ve preserved becomes the foundation for your next project, potentially within a few years. With this strategy, some individual property owners have grown portfolios producing $1 million or more in annual income without needing additional capital [4].

To ensure success, keep an eye on key metrics like cash-on-cash return (target 10–15%), cap rate (6–9% in Nova Scotia), and a debt service coverage ratio above 1.25×. For example, if you invest $500,000 in equity to finance a $2.5 million build, you could achieve a 12% cash-on-cash return - about $60,000 in net income annually on your $500,000 investment - a 7.5% cap rate, and a debt service coverage ratio of around 1.4× [3]. These figures highlight the potential for long-term portfolio growth, making this strategy a pathway to sustained financial success.

FAQs

Will using a HELOC or refinancing affect my ability to qualify for a new rental construction loan?

Using a HELOC (Home Equity Line of Credit) or refinancing can influence your ability to secure a rental construction loan. Both options can raise your debt-to-income ratio or increase your overall liabilities, which could make it tougher to qualify, depending on your financial situation and the lender's criteria. Given that construction loans come with staged draws and unique requirements, it's smart to check with your lender early on to see how these financial moves might impact your eligibility.

What are the biggest risks of using home equity to fund a rental build if interest rates rise?

Rising interest rates can lead to higher borrowing costs, directly impacting monthly payments and squeezing profitability. On top of that, if the market takes a downturn, you might face challenges when trying to refinance or sell the property at a favourable price. It's crucial to evaluate these risks thoroughly to safeguard your investment.

What CMHC MLI Select requirements must I meet to qualify for 95% financing?

To qualify for 95% financing through CMHC's MLI Select program, you'll need to meet several important requirements:

- Construction Financing: Secure funding that aligns with CMHC's guidelines, including detailed construction plans and accurate cost estimates.

- Loan-to-Value Ratio: Be prepared to provide at least a 5% down payment.

- Project Eligibility: Your project must be a multi-unit rental property with 4 or more units, meeting CMHC's rental housing standards.

- Financial Documentation: Submit comprehensive budgets, project timelines, and evidence that you can service the loan.